A serious accident can change your life in seconds — but you don’t have to face it alone. One minute you’re driving, the next you’re left with injuries, a wrecked car, and the overwhelming question: what is third-party insurance coverage?

Put simply, it’s not your insurance policy. It’s the insurance belonging to the driver who caused the crash. Their policy is legally required to cover the damages they caused to you, the innocent victim. Understanding how this works is the first step toward getting the justice and financial support you and your family deserve.

Understanding Your Rights After a Texas Accident

A sudden crash on a Houston freeway or a quiet neighborhood street can leave you feeling lost and disoriented. You're trying to heal from your injuries, but the medical bills are already piling up, and insurance adjusters are calling. This is exactly why getting a handle on third-party insurance is your first step toward taking back control.

Think of it this way: In any accident, there are at least two sides involved. You are the "first party," and the other driver is the "second party." The insurance company for the person who caused the wreck is the "third party." As the victim, you file a claim against their policy to get the compensation you need to rebuild your life.

Why This Matters for Your Recovery

Texas is a "fault" state when it comes to car accidents. This legal term simply means that the person whose negligence caused the collision is also responsible for paying for the damage. Third-party insurance is the financial system that makes this right.

Your claim isn’t just about getting your car fixed. It’s about securing the resources you need to put your life back together.

This compensation is meant to cover a wide range of losses, including:

- Medical Expenses: Everything from the ambulance ride and emergency room visit to ongoing physical therapy or future surgeries.

- Lost Wages: Reimbursement for the paychecks you missed because you were too injured to work, and compensation for any impact on your future ability to earn a living.

- Pain and Suffering: Compensation that acknowledges the physical pain and emotional trauma the accident has forced upon you and your family.

- Property Damage: The cost to repair or replace your vehicle.

As you navigate the legal and financial aftermath of a crash, it's also helpful to know about other resources available. For instance, the emotional toll can be significant, and some find a guide to ICBC counselling after an accident useful, as the journey to recovery involves more than just physical healing.

Here at The Law Office of Bryan Fagan, PLLC, our goal is to bring clarity and strength to you during this incredibly difficult time. We believe that understanding your rights empowers you to make the best decisions for your future. A Houston car accident attorney from our firm can take on the legal complexities, freeing you to focus completely on what matters most: your recovery.

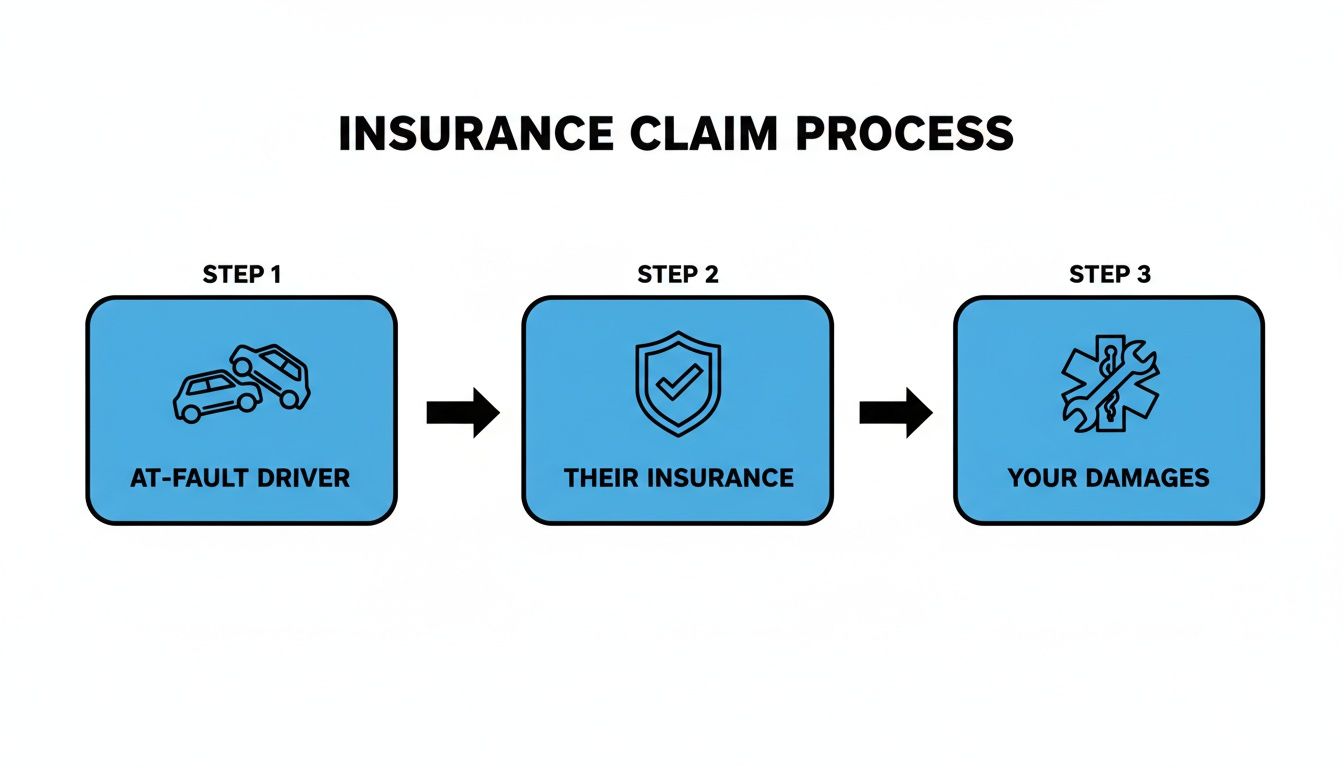

How a Third-Party Insurance Claim Works in Texas

Dealing with the aftermath of a car wreck is overwhelming, especially when you have to go through the other driver's insurance company. But knowing how the process works is the first step toward getting your life back on track and making sure you're treated fairly.

The whole thing kicks off the second the accident happens. Every step you take from that moment on can either protect your right to compensation or weaken your claim. Let's say you're hit on I-45 in Houston. Your first priority is always safety. But after that, the actions you take at the scene are absolutely critical for what comes next.

You'll want to call 911, get medical help for anyone who needs it, and—if you’re able—start gathering evidence. That means snapping photos of the cars and the surrounding area, and getting the other driver's name, phone number, and insurance information.

The First Steps to Protecting Your Claim

Once the initial shock wears off, your focus has to shift to holding the at-fault driver responsible. This process follows a pretty standard path, starting with letting the right insurance company know what happened.

Here are the essential first moves you need to make:

- Report the Wreck: Your claim needs to be filed with the at-fault driver's insurance company—the third party. You don't have to report it to your own insurer unless you plan on using your own coverage, like Personal Injury Protection (PIP).

- Stick to the Facts: When you call their insurance, give them only the basic, factual details. Tell them when and where the crash occurred, but don't guess about who was at fault or how badly you're hurt.

- Document Everything: Start a file right away. This is where you'll keep every single medical bill, pharmacy receipt, and a detailed journal of your symptoms and how your injuries are impacting your daily life. This careful record-keeping will become the backbone of your claim.

This visual gives you a simple overview of how a third-party claim flows, from the crash itself to getting compensation for your damages.

Ultimately, the key takeaway is that the at-fault driver's insurance is the one responsible for covering the harm their policyholder caused you.

Interacting With the Insurance Adjuster

Not long after you file the claim, an insurance adjuster will call you. It is vital that you understand what their job really is. The adjuster is not your friend; they work for the insurance company, and their primary goal is to protect their employer's bottom line by paying you as little as possible.

Adjusters are trained negotiators. They might sound friendly and concerned, but their objective is to find any reason to downplay your injuries, question your damages, and reduce the value of your claim. A common tactic is asking for a recorded statement, hoping you’ll say something they can twist and use against you later.

Here's a critical piece of advice: you have no legal obligation to give a recorded statement to the other driver's insurance company. It's one of the easiest ways injured people accidentally sabotage their own cases. Just politely say no and tell them all future communication needs to go through your attorney.

When your claim involves vehicle damage, knowing how to compare auto repair costs is crucial for getting what you're owed. The adjuster might try to steer you to one of their "preferred" shops or argue with legitimate estimates to keep their payout low. Having your own evidence helps you stand your ground against their lowball offers.

The entire claims process is designed to wear you down, making you feel so frustrated that you’ll accept a quick, cheap settlement just to be done with it. An experienced Houston truck crash lawyer recognizes these tactics from a mile away. We can take over all communication with the insurer, build a powerful case with solid evidence, and fight for the full compensation you truly deserve for your medical bills, lost wages, and the immense personal toll the accident has taken on your life.

Understanding Negligence and Liability in Texas

To get the at-fault driver's insurance company to pay up, it’s not enough to just say they caused the crash. You have to prove it, legally. This is where the concepts of negligence and liability come into play—they are the legal bedrock of every single third-party insurance claim in Texas.

Simply put, negligence is when someone fails to act with reasonable care, and that failure hurts you. Imagine a driver on a busy San Antonio street glancing down at a text. They roll through a red light and slam into another car in a violent T-bone collision. Their decision to text instead of focusing on the road was a failure to use the care any reasonable person would—and that makes them negligent.

Texas Comparative Responsibility Rules

So, what happens if the insurance company points a finger back at you, claiming you were also partly to blame? Texas has a specific rule for this exact scenario, known as comparative responsibility (or proportionate responsibility).

This rule is a game-changer for accident victims. It means you can still recover damages from the other driver even if you're found to be partially at fault for the collision. The catch? Your share of the blame cannot be 51% or more.

For instance, if a jury decides you were 20% at fault for a Houston freeway crash, your final compensation award would simply be reduced by that 20%. As long as you weren't the main cause of the wreck, you still have every right to hold the other driver accountable for their share.

Proving Fault Is The First Step To Justice

Establishing the other driver’s negligence is the key that unlocks the compensation you and your family deserve. This process isn't about pointing fingers; it's about a thorough investigation to gather cold, hard evidence that tells the true story of what happened.

Critical evidence often includes:

- The official police report filed at the scene.

- Photos and videos documenting vehicle damage, your injuries, and the crash site.

- Statements from any eyewitnesses who saw it happen.

- Expert testimony, which can be absolutely vital. You can find out more about how an accident reconstruction expert witness can prove what really happened.

A Texas personal injury lawyer who has seen the devastation caused by wrecks on I-10 and the Dallas North Tollway knows that third-party insurance is the lifeline victims depend on. It’s the at-fault driver’s policy that’s supposed to cover your damages.

What Damages Can You Claim?

Once you’ve established negligence, the next step is to calculate the full, true extent of your losses. A claim isn't just about the stack of medical bills on your kitchen table; it’s about every single way this accident has upended your life.

You are entitled to seek compensation for every loss you have suffered—physical, financial, and emotional. Understanding these categories helps ensure that no part of your suffering is overlooked when demanding a fair settlement.

Damages are generally broken down into two main types:

- Economic Damages: These are the tangible, out-of-pocket financial losses you can add up with a calculator. This includes all past and future medical bills, lost income from being unable to work, and any impact on your future earning capacity if the injuries will affect your career long-term.

- Non-Economic Damages: These are the profound but intangible losses that don't come with a price tag. This is compensation for your physical pain and suffering, emotional distress, mental anguish, scarring or disfigurement, and the loss of your ability to enjoy life.

A skilled Houston car accident attorney knows exactly how to build a case that not only proves negligence but also fully documents every penny of your economic and non-economic damages. We fight to make sure the at-fault driver’s insurance company understands the true value of your claim, so you can get the resources you need to heal and finally move forward.

First Party vs. Third Party Coverage: What You Need to Know

After a serious accident, the world of insurance can feel like a maze filled with confusing jargon. One of the most powerful things you can do to protect your family's financial future is to understand the different policies involved. The two most important types you'll run into are first-party and third-party coverage.

Let's break it down simply: third-party coverage belongs to the driver who hit you, while first-party coverage is the policy you pay for to protect yourself. When another driver’s carelessness causes your injuries, you file a third-party claim against their insurance. But don't overlook your own policy—it can provide an immediate and critical safety net.

Your Own Policy as a Financial Shield

Even when the other driver is clearly at fault, their insurance company might delay, dispute, or flat-out deny your claim. This is where your own first-party coverages become so important. They are designed to pay benefits directly to you, often regardless of who caused the crash.

Your first-party coverage can include several vital components:

- Personal Injury Protection (PIP): In Texas, every auto policy has to include PIP unless you reject it in writing. It helps cover medical bills and a chunk of your lost wages up to your policy limit, no matter who was at fault. This can be a real lifeline while you're waiting for a third-party settlement to come through.

- Medical Payments (MedPay): This is an optional coverage that, like PIP, helps pay for medical expenses for you and your passengers. It usually has lower limits than PIP and doesn't cover lost wages.

- Uninsured/Underinsured Motorist (UIM): This is arguably one of the most crucial coverages you can carry. It protects you if you're hit by a driver with no insurance or one whose policy is too small to cover the full extent of your catastrophic injuries.

Knowing the details of your own policy is critical. You might have access to immediate financial help you didn't even know was there.

The Key Differences At a Glance

The distinction between these coverages can be a bit confusing, but it really boils down to one simple question: who is paying for your damages? Is it the at-fault driver's insurance company, or is it your own?

Understanding the roles of each policy type empowers you to seek compensation from every available source. It's not about choosing one over the other; it's about strategically using both to ensure you have the resources you need to recover.

To make this crystal clear, let’s put them side-by-side. This table breaks down the fundamental differences between your own policy and the at-fault driver's policy after a Texas car accident.

First Party vs Third Party Insurance Coverage At a Glance

| Feature | First-Party Coverage (Your Policy) | Third-Party Coverage (At-Fault Driver's Policy) |

|---|---|---|

| Who Pays? | Your own insurance company pays you directly. | The at-fault driver's insurance company pays you. |

| When Does It Apply? | Immediately after an accident, regardless of fault (for PIP/MedPay/UIM). | Only after the other driver is proven to be at fault for the accident. |

| What's Covered? | Medical bills, lost wages (PIP), and damages caused by an uninsured/underinsured driver (UIM). | All damages, including medical bills, lost wages, property damage, and pain and suffering. |

| Main Purpose | To provide an immediate safety net and protect you from uninsured drivers or insufficient liability limits. | To compensate you for all losses caused by the policyholder's negligence. |

This table shows how each type of coverage serves a different but equally important purpose in your recovery.

For a deeper dive into what the at-fault driver's policy is responsible for, you can learn more about what bodily injury liability coverage entails and how it functions in a Texas claim.

Imagine this scenario: you're in a wreck caused by a driver who only has the minimum liability coverage required by Texas law—just $30,000 for a single injured person. If your medical bills alone are $100,000, their third-party policy won't even scratch the surface of your losses. In this situation, your own Underinsured Motorist (UIM) coverage would be your best path to recovering the remaining $70,000 and more.

A skilled wrongful death lawyer Texas knows how to investigate every policy involved to piece together the full compensation you deserve. We will analyze both the third-party liability policy and your own first-party coverages to build a strategy that leaves no stone unturned.

Common Tactics Insurance Companies Use to Deny Claims

After an accident, you’re in a vulnerable position. You're trying to manage physical pain, emotional trauma, and the financial stress that starts piling up almost immediately. It’s natural to expect the at-fault driver's insurance company to do the right thing, but you have to remember their real goal: protecting their profits by paying you as little as they possibly can.

Insurance adjusters are trained negotiators. Their job is to find any reason—big or small—to devalue your claim, slow it down, or deny it outright. Knowing their playbook is your first and best line of defense.

The Quick Lowball Offer

Don't be surprised if an adjuster calls you just days after the crash. They’ll sound friendly, sympathetic, and offer a check for a few thousand dollars right away. With medical bills coming in, this can feel like a lifeline.

But this isn't an act of kindness; it's a strategic move. The insurance company is hoping you’ll take the money and sign away your rights before you even know how badly you’re hurt. Some of the most serious injuries, like back and neck trauma, can take weeks to fully surface. Once you cash that check, the case is closed. You can't ask for another dime, even if you find out later you need surgery.

The Recorded Statement Trap

An adjuster will almost always ask for a recorded statement about the accident, presenting it as a routine part of the process. It’s not. It’s a trap, plain and simple, designed to get you to say something they can use against you later.

They are masters at asking leading questions or getting you to minimize your injuries. An innocent comment like "I'm doing okay" can be twisted to argue that your injuries aren't that severe. You are never required to give a recorded statement to the other driver’s insurance company. The best way to handle this is to politely decline and tell them your attorney will be in touch.

Delay, Deny, Defend

Insurance companies know that the longer they can drag things out, the more desperate you’ll become. Time is their greatest weapon. As financial pressure mounts, you’re more likely to accept a fraction of what your claim is actually worth.

This strategy is often called "delay, deny, defend," and it works like this:

- Delaying: They’ll ignore your calls, claim they lost your paperwork, or ask for the same documents over and over again. Anything to bring the process to a crawl.

- Denying: They’ll hunt for any loophole or minor inconsistency to deny your claim. A common tactic is blaming your injuries on a pre-existing condition.

- Defending: If you refuse to give up, they’ll dig in their heels and prepare for a legal fight, hoping the cost and stress will force you to back down.

This is a war of attrition, and it’s a fight you shouldn’t have to wage while you’re focused on healing.

Disputing Your Medical Treatment

Another common tactic is to second-guess your doctor. An adjuster, who has zero medical training, might argue that the treatment you're receiving is unnecessary, excessive, or unrelated to the crash. They will challenge your doctor’s expert medical opinion just to avoid paying the bills for your care.

Never let an insurance adjuster dictate your medical treatment. Your health comes first. Always follow your doctor's advice and keep detailed records of every appointment, prescription, and therapy session.

For a more in-depth look at the strategies insurers use, you can learn more about why insurance companies deny claims and how to effectively fight back.

At The Law Office of Bryan Fagan, PLLC, we’ve seen every one of these tactics and know exactly how to shut them down. A Houston personal injury lawyer from our team can take over all communication with the insurer, shielding you from their pressure and manipulation. We build a powerful, evidence-based case that they can’t ignore, forcing them to come to the table and negotiate in good faith.

Why You Need a Texas Personal Injury Lawyer for Your Claim

Trying to take on a massive insurance corporation by yourself after a serious accident is an unfair fight. It’s you against their teams of adjusters and lawyers who handle thousands of claims a year. Their one and only goal is to protect their company’s profits—not to make sure you get a fair payout.

An experienced Houston car accident attorney is the advocate you need to level the playing field. When you work with us, you’re not just another claim number. You’re a person with a story, and we make it our mission to ensure the insurance company hears it.

We Conduct a Thorough Independent Investigation

The insurance company will do its own investigation, sure, but it will be laser-focused on finding ways to downplay your claim or even shift the blame onto you. We don't play that game. We conduct our own comprehensive investigation with one goal in mind: proving the other driver's negligence and building the strongest case possible for you.

Our team hits the ground running to:

- Secure the official police report and all related evidence.

- Interview eyewitnesses while their memories are still fresh.

- Gather and preserve critical evidence like traffic camera footage or data from a truck's "black box."

- Work with accident reconstruction experts to prove exactly how the crash happened.

This proactive approach is often what separates a denied claim from a successful recovery.

We Calculate the Full and True Value of Your Claim

An insurer's first offer is almost always a lowball number. It rarely comes close to covering what you’ve truly lost. They're banking on you being desperate enough to accept it before you even understand the long-term consequences of your injuries.

An experienced personal injury lawyer knows how to calculate the real value of your claim, which includes not just current bills but also the future costs tied to your recovery.

We will meticulously document every single loss, including:

- All current and future medical expenses, from surgeries to physical therapy.

- Lost income and what you can no longer earn in the future.

- The immense physical pain and emotional suffering you've been forced to endure.

- The impact on your quality of life and relationships.

We leave no stone unturned. Our demand for compensation will reflect every single facet of your suffering.

We Aggressively Negotiate and Litigate on Your Behalf

Armed with a powerful, evidence-based case, we take the fight to the insurance company. We handle all the phone calls, the paperwork, and the back-and-forth negotiations, shielding you from the stress and pressure tactics that adjusters love to use. Our reputation as trial-ready litigators often convinces insurers to offer a fair settlement without ever stepping foot in a courtroom.

But if they refuse to do what’s right, we won’t hesitate to file a lawsuit and take your case before a Texas judge and jury. We work on a contingency fee basis, which means you pay absolutely no attorney’s fees unless we win your case. This removes the financial risk, allowing you to focus on healing while we focus on justice. Recovery is possible, and our team is here to help you get there.

How Long Do You Have to File a Claim in Texas?

In Texas, you generally have two years from the date of the accident to file a personal injury claim. This is known as the statute of limitations, and it’s a hard deadline.

If you miss this two-year window, the courthouse doors will likely be closed to you forever, meaning you lose your right to seek compensation. It’s absolutely critical to connect with a Texas personal injury lawyer long before this deadline approaches. This gives your attorney the time needed to properly investigate, preserve evidence, and build a strong case on your behalf.

What if My Damages Exceed the At-Fault Driver's Policy Limits?

This is a tough and unfortunately common situation, especially when someone has suffered a catastrophic injury. The at-fault driver's insurance will only pay up to their policy limit, not a penny more.

But that doesn't always mean you're out of options. If you have Uninsured/Underinsured Motorist (UIM) coverage on your own policy, you may be able to turn to it to cover the remaining costs. A skilled attorney will dig deep to uncover every possible source of recovery, making sure you can access the maximum compensation from every available policy.

Should I Accept the First Settlement Offer?

Almost never. The insurance adjuster’s first offer is rarely their best one. They are trained to offer a low amount right out of the gate, hoping you’ll take the quick cash before you truly understand the full extent of your injuries, lost wages, and future medical needs.

Never sign anything or accept a check from an insurance company without speaking to a qualified Houston car accident attorney first. Your lawyer can properly evaluate your case, calculate its true value, and make sure you aren't leaving money on the table that you will desperately need for your future.

A serious accident can change your life in seconds — but you don’t have to face it alone. The experienced attorneys at The Law Office of Bryan Fagan, PLLC are here to stand up for you and fight for the fair compensation you deserve. We understand what you're going through, and we are ready to help. Schedule a free, no-obligation consultation today to understand your rights and get the compassionate guidance you need. Recovery is possible, and legal help is available. Contact us now to start your journey toward justice.