A serious accident can leave you rattled, hurting, and unsure what to do next. Then you learn the other driver has no insurance, and the stress gets worse fast. You may be wondering how your medical bills will get paid, who will fix your car, and whether you're stuck covering losses caused by someone else.

If you searched for what happens if the other driver has no insurance in Texas, the short answer is this. You still may have ways to recover compensation. The path forward depends on fault, your own coverage, the available evidence, and whether the uninsured driver has anything worth pursuing.

A Serious Accident Can Change Your Life in Seconds

A Houston freeway crash often starts like any other day. Traffic slows. Someone looks down for a second. Then your vehicle jolts forward, airbags deploy, and everything after that feels blurred. You check yourself, check your passengers, and then hear the worst follow-up news. The driver who caused it doesn't have insurance.

That situation is upsetting, but it isn't rare. One Texas injury firm, citing Texas Department of Transportation data, reports that as many as 1 in 5 Texas drivers are uninsured, or roughly 20% of drivers on the road. The same source notes that Texas minimum bodily-injury coverage is $30,000 per person and $60,000 per crash, which can run out quickly in a serious injury case involving hospitalization, surgery, or long-term care, according to this discussion of uninsured-driver crashes in Texas.

The first problem is financial uncertainty

It's generally expected that the at-fault driver's insurance will handle the damage. When there's no policy, the normal claim route disappears. That doesn't mean your case disappears.

Texas follows a fault-based system. In practical terms, that means the driver who caused the wreck is still responsible for the harm they caused. The challenge is no longer just proving fault. It's finding a realistic source of recovery.

Practical rule: Don't assume “no insurance” means “no case.” It means you need a different strategy.

A common real-world example

After a rear-end crash on I-45, a driver may have neck pain, a damaged vehicle, and missed time from work within days. If the other driver has no coverage, the injured person usually needs to act on two tracks at once. First, protect the insurance claim available under their own policy. Second, preserve evidence in case a direct claim or lawsuit makes sense later.

That's why the early hours matter. The crash report, photos, witness names, and medical records can shape the entire claim. If those pieces are missing, even a valid uninsured motorist claim can become harder than it should be.

Here's the reassuring part. Texas law gives injured people options. They aren't always simple, and they aren't always fast, but there are workable paths forward.

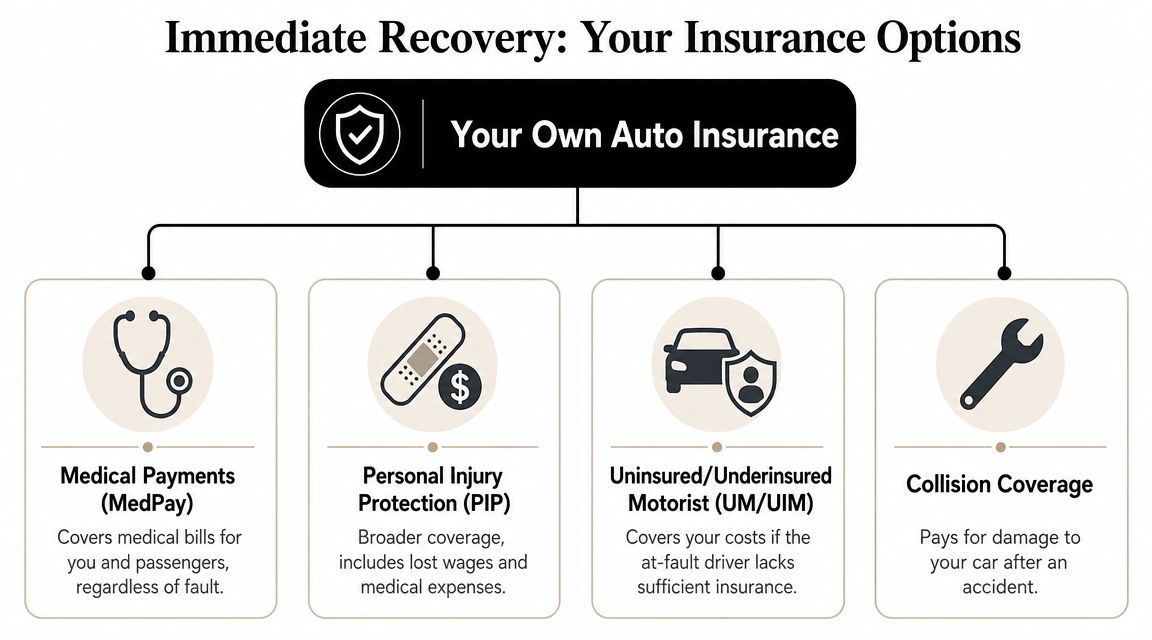

Your Immediate Recovery Options Through Your Own Insurance

When the other driver has no coverage, your own auto policy often becomes the fastest place to look for help. Many people don't realize how many different parts of their policy may apply after a crash.

Texas uses a fault-based insurance system, so you can still pursue the at-fault driver for damages such as medical bills, lost wages, property damage, and pain and suffering. Texas also requires drivers to carry minimum liability insurance of $30,000 per injured person, $60,000 per crash, and $25,000 for property damage, and Texas insurers must offer uninsured motorist coverage unless it was rejected in writing, as explained in this overview of Texas uninsured-driver claims.

UM and UIM coverage usually matter most

Uninsured motorist coverage, often called UM, is designed for the exact situation you're in when the at-fault driver has no insurance. Underinsured motorist coverage, or UIM, applies when the other driver has insurance, but not enough to cover the damage.

If your policy includes this protection, it can function as a substitute for the missing liability coverage. That doesn't mean the claim is automatic. You still have to show the other driver caused the collision and prove your damages.

If you want a more focused breakdown of how these claims work, review this page on Texas uninsured and underinsured coverage.

Other parts of your policy may help right away

Different coverages solve different problems. That matters because the bills after a crash rarely arrive all at once.

- Personal Injury Protection can help with medical expenses and may also help with lost income after the wreck.

- Medical Payments coverage may help pay medical bills, even while the fault investigation is still developing.

- Collision coverage may help pay to repair your vehicle, regardless of who caused the crash.

Often, people get stuck. They think using their own policy means they did something wrong. That's not the right way to look at it. These coverages exist because Texas drivers know not everyone on the road is properly insured.

What works and what doesn't

A strong first move is to request a copy of your declarations page and identify every coverage that might apply. That single document often answers urgent questions about repairs, treatment, and wage loss.

What doesn't work is waiting for the uninsured driver to “figure something out.” In most cases, that delay only increases pressure on you while evidence gets colder and deadlines get closer.

Your insurance company may be your recovery source, but in a UM claim it still evaluates fault, damages, and documentation closely. Treat the claim seriously from day one.

Understanding Fault and Negligence in an Uninsured Driver Claim

Texas law doesn't excuse a driver from responsibility just because they failed to buy insurance. The legal issue is still the same. Who caused the crash, and what did that crash cost you?

Texas is a fault-based, modified comparative negligence state. An uninsured at-fault driver remains legally responsible, but your recovery can be reduced by your share of fault and barred if you are 51% or more responsible. If you're found 20% at fault, the recoverable amount is reduced by 20%, as explained in this summary of Texas fault rules in uninsured-driver cases.

Why fault still matters in a claim against your own insurer

Many accident victims are surprised by this. Even when you file under your own UM coverage, you still have to prove the uninsured driver caused the wreck. Your insurer doesn't automatically pay because the other driver lacked insurance.

That means your case depends on evidence:

- Crash report

- Vehicle photos

- Witness statements

- Medical records

- Scene details such as lane position, signals, and damage patterns

For a plain-English look at this issue, this guide on how negligence is proven in Texas injury cases is a useful starting point.

A simple Dallas intersection example

Say two drivers collide in an intersection in Dallas. One says the light was green. The other says the same thing. There's no insurance on the at-fault side, and now your UM carrier wants proof before paying.

If the evidence shows the uninsured driver ran the light, your claim is strong. If the evidence also shows you were speeding, the insurer may argue you share part of the blame. Under Texas comparative responsibility rules, that percentage can directly reduce what you recover.

A case like that often turns on details that seemed small at the scene:

| Evidence | Why it matters |

|---|---|

| Traffic camera footage | Helps show signal timing and vehicle movement |

| Independent witness statement | Supports or contradicts each driver's version |

| Point of impact | Can confirm lane position and direction |

| Medical timeline | Connects the injuries to the wreck |

Fault arguments start early

Insurance companies start evaluating fault almost immediately. That's why early statements matter. Casual comments like “I didn't see them until the last second” can be used to argue you were partly responsible.

The strongest uninsured-driver claims are usually built on simple, early proof. Photos, names, treatment records, and a consistent timeline.

This is also why legal terminology matters less than clear facts. Negligence is just the legal word for careless conduct that causes harm. In a car crash case, proving negligence usually means showing the other driver made an unsafe choice and that choice caused your injuries.

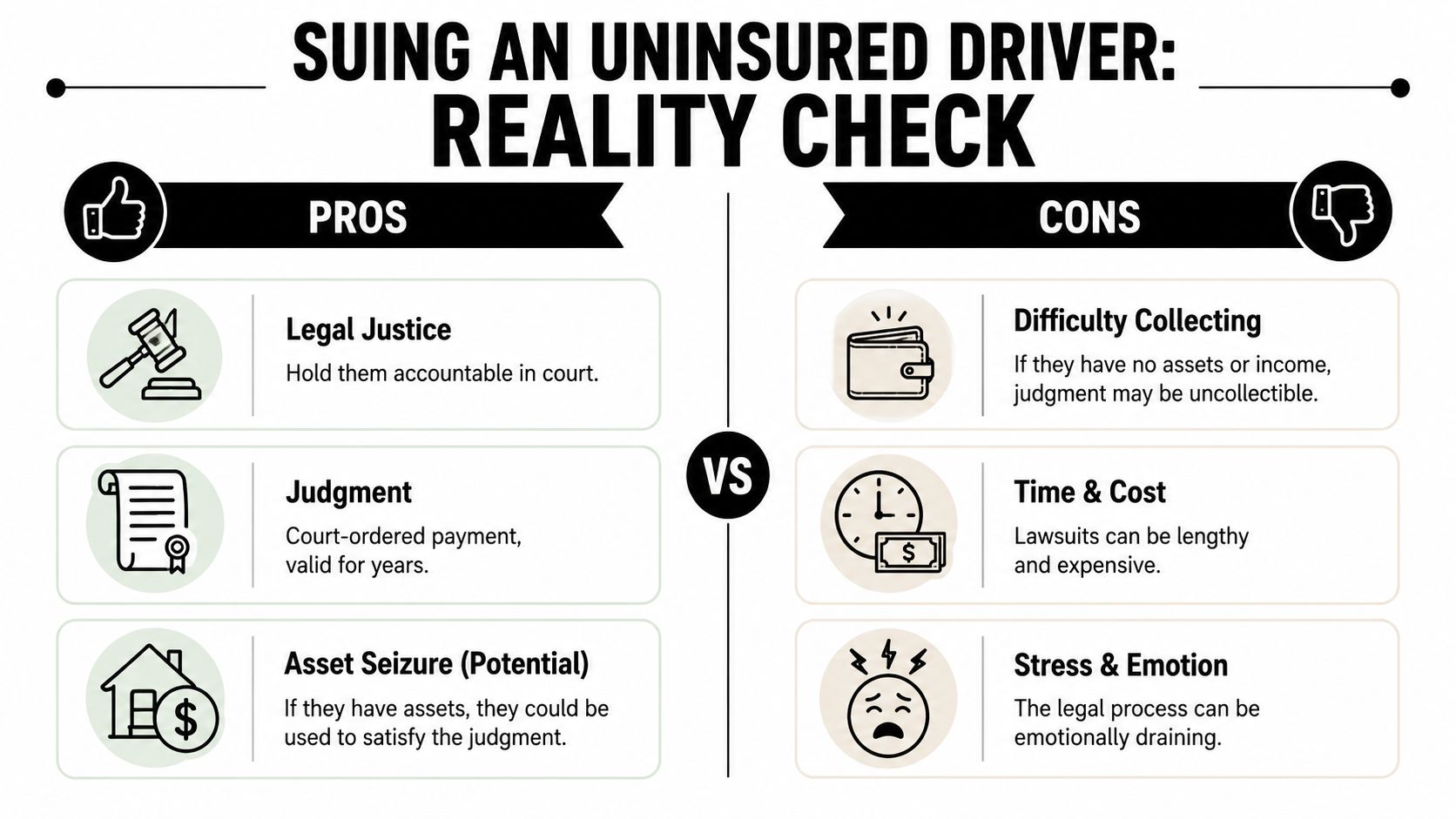

Suing the At-Fault Driver The Reality of Collecting Damages

Yes, you can sue an uninsured driver in Texas. In some cases, that's the right move. But whether you can sue and whether suing will lead to money collected are two different questions.

The Texas Department of Insurance explains that when the at-fault driver has no insurance, the two main recovery paths are a claim under your own UM/UIM coverage or a direct lawsuit against the driver personally. It also explains the practical problem of collectability. A judgment may exist on paper, but recovery depends on the driver's assets, income, and whether any third-party liability exists, as outlined in this Texas Department of Insurance guidance.

When a lawsuit makes practical sense

A direct lawsuit may be worth serious attention if there's reason to believe the driver has something to collect from. That might include non-exempt assets, reliable income, or another party that may share legal responsibility.

Examples include situations where:

- The driver was working at the time and an employer may be involved

- A company owned the vehicle

- A third party contributed to the crash

- The uninsured driver has identifiable assets

In those cases, a lawsuit can do more than make a point. It can create an advantage and a path to actual recovery.

When it may be more effort than value

A lot of uninsured drivers don't carry insurance because they are already struggling financially. If that driver has no reachable assets and no meaningful income, a lawsuit can become a long process that produces little or nothing.

That doesn't make your injuries less real. It just means strategy matters. Many victims are better served by focusing first on available policy benefits, preserving evidence, and evaluating whether a third party may have exposure.

Here's the practical trade-off:

| Option | Main benefit | Main risk |

|---|---|---|

| UM/UIM claim | Often the most realistic recovery source | Your own insurer may dispute fault or damages |

| Direct lawsuit | Can hold the driver personally accountable | Judgment may be hard or impossible to collect |

A paper judgment isn't the same as compensation in your bank account.

The right answer depends on facts, not emotion. After a truck collision in Houston, for example, the uninsured individual driver may not be the only person or entity worth investigating. In a straightforward neighborhood fender bender, the answer may be very different.

A Step-by-Step Guide to Protecting Your Rights

In the first days after a crash, the right steps can protect both your health and your claim. The wrong steps can create gaps that an insurer later uses against you.

Start with safety and documentation. Then move quickly into medical care, insurance notice, and recordkeeping.

What to do at the scene

If you're physically able, take these steps in order:

- Get to safety. Move out of active traffic if possible.

- Call 911. A police report helps document what happened.

- Exchange information. Get the other driver's name, license plate, and contact details, even if they admit they have no insurance.

- Take photos. Capture vehicle damage, roadway position, skid marks, debris, weather conditions, and visible injuries.

- Talk to witnesses. Get names and phone numbers before people leave.

Don't argue about fault at the roadside. Don't apologize in a way that sounds like an admission. And don't rely on memory later when your phone can preserve the scene immediately.

What to do in the next day or two

Medical treatment should move near the top of your list, even if your pain seems minor at first. Soft-tissue injuries, concussions, and back injuries often feel worse after the adrenaline wears off.

Keep your records organized from the start:

- Medical visits and discharge papers

- Prescriptions and mileage to appointments

- Repair estimates and towing receipts

- Missed work records

- Emails and claim numbers from insurers

This is also the point where many people notify their own insurance company. Give basic facts. Be accurate. Don't guess if you don't know an answer.

A short visual overview can help if you're still sorting through the first steps:

Be careful with insurance conversations

Your insurer may ask for a statement. In some cases, providing basic information is routine. In others, especially where fault is disputed or injuries are serious, it makes sense to slow down and get legal advice before giving a detailed recorded statement.

That's particularly true if the crash involved a commercial vehicle, multiple cars, or a fatality. A car accident lawyer, a truck crash lawyer Houston, or a wrongful death lawyer Texas team can help preserve evidence and manage communication. If the collision caused severe long-term harm, support from a catastrophic injury case lawyer may also be necessary.

How long do you have to file a claim in Texas

Texas personal injury claims are subject to filing deadlines, often called the statute of limitations. In plain terms, that means you don't have unlimited time to sue. Waiting too long can damage or even eliminate your legal options.

You should also know that insurance policies can impose notice requirements that matter much sooner than a lawsuit deadline. That's one reason fast action matters in uninsured-driver cases.

A practical checklist that helps

Some steps consistently help. Others consistently cause problems.

- Helpful move. See a doctor promptly and follow the treatment plan.

- Helpful move. Keep every bill, estimate, and claim letter.

- Costly mistake. Posting about the crash or your injuries on social media.

- Costly mistake. Delaying treatment because you hope the pain will fade.

- Helpful move. Speak with a Texas personal injury lawyer or Houston car accident attorney before the case gets boxed in by bad assumptions.

One option for guidance in these cases is the Law Office of Bryan Fagan, PLLC, which handles Texas motor vehicle injury claims including uninsured-driver disputes.

You Are Not Alone Get Help from an Experienced Attorney

An uninsured-driver case puts pressure on you from several directions at once. You may be trying to heal, get your car fixed, answer calls from adjusters, and figure out whether the driver who hit you can be sued at all. That's a lot for one person or one family to manage.

An experienced lawyer helps by making the case concrete. That means gathering records, securing the crash report, identifying available insurance, evaluating whether a direct lawsuit has value, and presenting the evidence in a way that supports full damages. It also means telling you when a path isn't worth the time and stress.

What legal help changes

A good lawyer won't just repeat that you have options. The lawyer should help you choose between them.

That may include:

- Reviewing your policy to find UM, collision, PIP, or medical payment coverage

- Building proof of fault for a disputed crash

- Assessing collectability before filing suit against an uninsured driver

- Looking for other responsible parties in a company-vehicle, rideshare, or truck case

- Handling insurer communication so you don't get boxed into a weak statement

For families trying to understand how injury claims are built and managed from intake through resolution, this essential guide for personal injury firms offers a useful operational perspective on what a well-run case process should look like.

When to call a lawyer

If you have serious injuries, missed work, a disputed fault story, or a carrier that's delaying your claim, don't wait for the case to “sort itself out.” It usually won't.

This page on when you should hire a personal injury lawyer in Texas can help you decide whether it's time to bring in counsel.

Recovery is possible, even when the driver who caused the crash had no insurance. The key is to act early, protect the evidence, and make decisions based on collectability and coverage, not frustration alone.

If you were hurt by an uninsured driver, Law Office of Bryan Fagan, PLLC can help you understand your options in a free consultation. You can talk through fault, insurance coverage, medical bills, lost income, and whether a direct claim or lawsuit makes sense. There's no need to handle this alone, and there are no fees unless the firm recovers compensation for you.