A serious accident can change your life in seconds, but you don't have to face it alone.

One moment you're driving home on a Houston freeway, heading to work in Dallas, or picking up your kids in San Antonio. The next, you're dealing with a damaged car, pain you didn't expect, and an insurance process you never asked to learn. If the crash wasn't your fault, your first thought is usually simple: the other driver should pay. In Texas, that may be true, but the path from “not my fault” to actual compensation is rarely automatic.

Searching for what happens if accident was not your fault Texas often involves dealing with more than a legal question. They're worried about medical bills, missed work, transportation, and whether saying the wrong thing to an adjuster could hurt their case. Those concerns are real.

This article is meant to give you a practical roadmap. You'll learn what to do at the scene, how insurance claims work in Texas, how fault can still become a fight, what damages may be available, and when it makes sense to speak with a Texas personal injury lawyer. If your case involves a truck collision, fatal crash, or life-changing injuries, the same basic rules still matter, whether you need a Houston car accident attorney, a truck crash lawyer Houston families trust, or a wrongful death lawyer Texas families can turn to for answers.

An Accident Can Change Everything But You Are Not Alone

A crash that wasn't your fault often brings two kinds of pain at once. There's the physical and emotional impact of the wreck itself, and then there's the stress of dealing with everything that follows.

A lot of people sit in that first consultation and tell me the same thing: “I didn't cause this, so why is this so complicated?” That reaction makes sense. You expect the facts to speak for themselves. Sometimes they do. Sometimes they don't.

Take a common example. After a rear-end collision on a busy Texas highway, you may think liability is obvious. But within days, the other driver's insurer might ask for a statement, question your injuries, or suggest you stopped suddenly. At the same time, your car may be in the shop, your neck may be stiffening up, and your employer may be asking when you'll be back.

You can be the innocent driver and still end up in a dispute about fault, treatment, or the value of your losses.

That doesn't mean you're powerless. It means the process has rules, and once you understand those rules, you can make better decisions.

What helps most at this stage is slowing the situation down. Focus on the next right step. Protect your health. Preserve evidence. Be careful with insurance conversations. Keep records. Ask questions early.

You don't need to know everything today. You just need a clear starting point and a plan.

Your First Steps After a Not-at-Fault Accident

A common scene goes like this. You are standing on the shoulder, your heart is racing, traffic is still moving, and your phone is in your hand. In that moment, it helps to treat the next hour like building a file, one piece at a time. The stronger that file is, the easier it is to protect both your health and your claim.

Put safety first

Start with safety, not proof. If the vehicles can be moved without creating more danger, get to a safer spot. Turn on hazard lights. Check yourself and anyone else involved for injuries. If there is any chance someone is hurt, call 911.

When officers arrive, stick to clear facts. Say where you were, what lane you were in, what you observed, and where the vehicles made contact. If you are unsure about something, say you are unsure. Accuracy helps more than trying to fill in the blanks.

One more point. Politeness is fine. Guessing about fault is not. A simple apology said out of stress can later be used in a way you never intended.

Document the scene before it changes

Accident scenes change fast. Cars are moved. Debris gets cleared. Witnesses leave for work or school. Your phone is often the fastest way to preserve what the road looked like before that evidence disappears.

Try to collect:

- Photos of every vehicle: Get wide shots and close-ups, including damage on all sides if you can.

- Road details: Capture traffic lights, lane markings, skid marks, street signs, construction zones, and weather conditions.

- Driver and vehicle information: Photograph the license plate, insurance card, and driver's license if the other driver allows it.

- Witness contact information: A name and phone number can matter later if the stories conflict.

A good way to think about this is simple. Your memory tells the story. Photos and contacts help prove it.

Get medical care early

Many people feel “okay” right after a wreck and wake up the next morning with neck pain, back pain, headaches, or numbness. Adrenaline can hide symptoms for hours. Early treatment protects your health first, and it also creates a clear medical record tied to the crash.

If urgent care or an emergency room is not needed, make an appointment as soon as you can with a doctor who can evaluate your injuries and recommend follow-up care. Some people also look for expert help for car accident victims while learning about treatment options after a wreck.

Keep every bill, discharge paper, prescription receipt, work note, and mileage record related to treatment. Those documents are the paper trail that shows what the crash cost you.

Texas also gives you a limited window to file a personal injury lawsuit after a crash. In many cases, that deadline is two years from the date of the accident. Even with that time limit, waiting is rarely helpful because early medical records often give the clearest picture of when symptoms began and how serious they became.

Be careful when insurance starts calling

You should report the crash to your own insurer promptly. That is different from giving the other driver's insurer a detailed recorded statement right away.

An adjuster may sound casual and helpful. Their questions are still designed to evaluate the claim and limit what the company pays. Before you go into details, read about whether you should speak with insurance after a Texas accident.

Here's a helpful overview of what to protect right away:

Practical rule: If you are hurt, unsure how the crash happened, or feeling pressured, pause before giving a recorded statement. Get clear on your rights first.

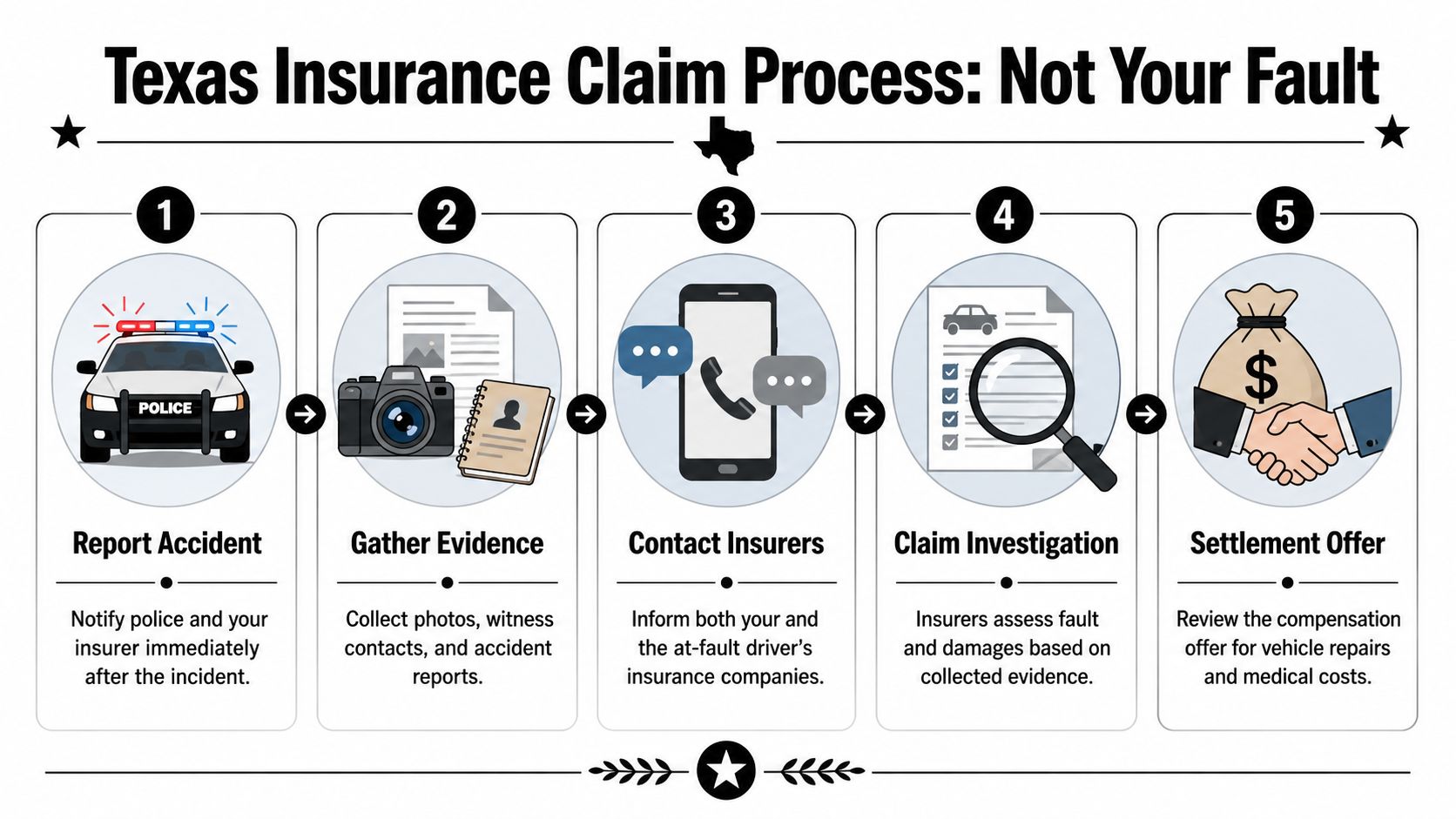

Filing an Insurance Claim in a Texas At-Fault System

The claim process often feels backwards at first. You were the one hit, but now you are the one gathering records, answering calls, and waiting for an adjuster to decide what the case is worth.

Texas follows an at-fault system, so the driver who caused the crash is usually responsible for the losses that follow. In plain English, that usually means you make a claim against the other driver's liability coverage and prove two things: they caused the wreck, and the wreck caused your losses.

What the claim usually looks like

A Texas insurance claim usually moves in stages. It helps to treat it like building a file, one layer at a time. First comes the basic report. Then the insurance company checks liability. Then it looks at your medical records, vehicle damage, lost income, and any other proof showing what the crash cost you.

Here is the usual sequence:

| Step | What happens |

|---|---|

| Claim opened | You report the crash and give the insurer the basic facts. |

| Fault review | The adjuster reviews the police report, photos, witness statements, and vehicle damage. |

| Damage review | Medical bills, treatment notes, repair estimates, wage records, and receipts are collected. |

| Coverage check | The insurer confirms what policy applies and how much coverage is available. |

| Settlement evaluation | The insurer decides whether to accept fault, deny fault, or make an offer. |

This is also why good documentation matters so much. If the insurer disputes how the wreck happened, records such as photos, dash cam footage, witness information, and even GPS tracking route history can help confirm where the vehicle was and how events unfolded.

Why the adjuster focuses so much on fault

Adjusters do not just ask, “Were you hurt?” They also ask, “Can we shift part of the blame?”

That question matters because Texas uses a comparative fault rule. If the insurance company argues that you were partly responsible, it may try to reduce what it pays. You can read a plain-English explanation of how comparative fault works in Texas injury claims.

A simple way to view it is this: liability is the front door to the claim, and damages are what you carry through it. If the insurer can narrow the doorway by disputing fault, it may try to limit the whole claim.

What to say, and what to avoid

You do not need a long speech. Clear, careful facts are better.

Useful communication usually sounds like this:

- State the basics clearly: where the crash happened, when it happened, and which vehicles were involved

- Answer only what you know: if you are unsure about speed, distance, or timing, say that

- Describe symptoms accurately: pain that seems minor on day one can become more serious later

- Avoid blame statements: comments like “I may have missed them” can be used against you before all the evidence is reviewed

Strong claims are built with records and consistency. They are rarely improved by guessing, speculating, or trying to sound polite by taking blame.

If your vehicle may be totaled

The property damage part of the case often moves faster than the injury part. That can catch people off guard.

If the insurer says your car is a total loss, the discussion usually centers on actual cash value. That is the vehicle's market value right before the crash, not what you originally paid for it or how badly you need a replacement now. Texas insurers must follow specific total-loss rules, as described in this Texas total loss discussion.

If the value looks too low, push for the documents behind the number. Ask for the valuation report, the comparable vehicles used, and any adjustments for mileage, condition, or options. Then compare that information to your own photos, maintenance records, upgrade receipts, and local sales listings. That step-by-step review often shows whether the offer is fair or needs to be challenged.

How Texas Law Determines Fault and Why It Matters

People often think fault is obvious. Sometimes it is. But many cases come down to competing versions of the same event.

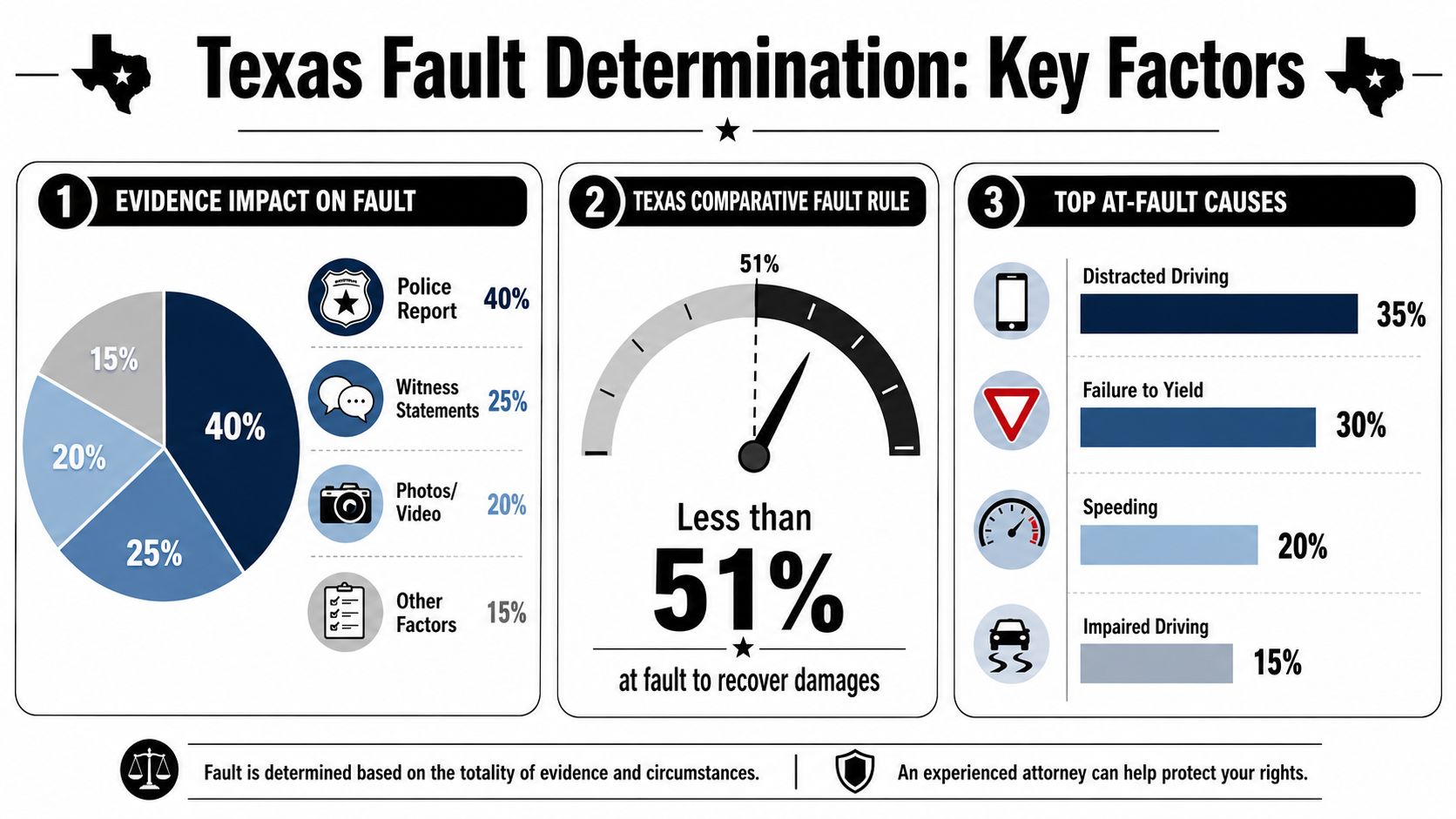

Texas is an at-fault state, and it also follows modified comparative fault. Under that rule, a person can recover damages only if they are 50% or less responsible. If they are 51% or more at fault, they recover $0, as explained in this Texas comparative fault overview.

A simple example of how the rule works

Many individuals often find this confusing.

If your total damages are $100,000 and you are found 20% at fault, your recovery would typically be reduced to $80,000. If you are found 50% at fault, you could recover only half of your proven losses. But if the evidence pushes you to 51% or more, your recovery is barred.

That's why fault is not just a label. It directly changes the outcome of the case.

What evidence usually affects fault

Insurance companies and lawyers look at the same core sources again and again:

- Police reports: These may shape the first version of the story.

- Photographs and video: Damage patterns and road layout often matter more than people expect.

- Witness statements: Independent witnesses can clarify what each driver was doing.

- Medical records: These help connect the collision to the injuries being claimed.

In some cases, technology helps fill gaps. Dashcams, app data, and even GPS tracking route history can provide context about where a vehicle traveled before a collision.

If you want a fuller explanation of how these percentages work, this guide to Texas comparative fault law is a useful starting point.

Why small facts become major issues

A disputed lane change. A claim that you were following too closely. An argument over whether you braked in time. These may sound minor, but they can shift fault percentages in ways that change the value of the claim.

Here's a real-world style example. After a Houston freeway crash, one driver may say the other cut across two lanes. The other may insist you were speeding. Without photos, witness accounts, or video, the insurer may try to split blame.

Fault isn't decided by who sounds most confident. It's decided by what can be proved.

That's why early evidence collection matters so much in a Texas car accident case.

What Compensation Can You Recover After an Accident

After a crash, clients often ask me one practical question: “What is this claim supposed to cover?”

A good way to answer it is to picture your losses in two buckets. One bucket holds the costs you can measure with records, bills, pay stubs, and repair estimates. The other holds the human impact of the wreck, meaning how your injuries changed your daily life, your comfort, and your ability to do normal things.

In a Texas injury claim, both categories can matter. The job is to show, clearly and methodically, what the collision cost you financially and what it took from you personally.

Economic damages

Economic damages are the easier part to spot because they usually leave a paper trail.

If the wreck sent you to the emergency room, forced you to miss work, or left you paying for a rental car while your vehicle was in the shop, those losses may be part of your claim. The same is true for future care if your doctors expect ongoing treatment.

Common examples include:

- Medical expenses: ER care, ambulance bills, follow-up visits, imaging, physical therapy, prescriptions, and other treatment tied to the crash

- Lost wages: Paychecks, salary, commissions, or self-employment income you lost while you were recovering

- Loss of earning capacity: Income you may lose in the future if your injuries limit the kind of work you can do

- Property damage: Repair or replacement of your vehicle and other damaged personal items

- Out-of-pocket costs: Travel to appointments, medication co-pays, rental car charges, and similar crash-related expenses

This part of the case works a lot like assembling a receipt file after a major home repair. Every document helps show what had to be spent, what income stopped coming in, and what expenses are still ahead.

Non-economic damages

Non-economic damages are harder to calculate, but they are no less real.

A back injury may mean you cannot sleep through the night. A shoulder injury may make it painful to pick up your child. A concussion may leave you struggling to focus at work or feeling unlike yourself for weeks or months. Those losses do not arrive as a bill in the mail, but they still affect the value of the case.

These damages can include:

- Physical pain

- Mental anguish

- Physical impairment

- Loss of enjoyment of daily life

- Disfigurement or scarring in some cases

This is often the part people understate. They tell the insurer about the hospital visit but leave out the fact that they now need help getting dressed, cannot drive comfortably, or had to stop hobbies and routines that mattered to them. Those details count.

A strong claim shows more than what you paid. It shows how your life changed.

A practical way to measure your losses

If you are trying to understand the value of your case, start with three simple questions:

| Area | Questions to ask |

|---|---|

| Medical impact | What treatment have you had, what treatment is still recommended, and what symptoms continue day to day? |

| Income impact | How much work have you missed, and has the injury changed your ability to earn a living? |

| Life impact | What tasks, routines, family roles, or activities have become painful, difficult, or impossible? |

That framework gives you a roadmap. Save your bills. Keep records of missed work. Write down the daily problems the injury causes while they are still fresh in your mind.

In some cases, the path is more complicated because there may be questions about future treatment, long-term disability, or limited insurance coverage. If coverage becomes a concern, it helps to understand how uninsured and underinsured motorist coverage in Texas can affect what is available.

What If the At-Fault Driver Was Uninsured or Fled the Scene

One of the hardest moments in a consultation is when a client says, “We know it wasn't my fault, but the other driver had no insurance,” or “They just drove off.”

That situation is frightening, but it doesn't always mean the case ends there.

Your own policy may become the next option

Texas consumer guidance says that if the other driver was uninsured or left the scene, you should turn to your own coverage. In these cases, people often need to rely on uninsured or underinsured motorist coverage, MedPay, or collision coverage to avoid paying everything out of pocket, as noted in this Texas insurance guidance for claims against the other driver.

That's important because “not your fault” doesn't always mean the other driver can pay.

If you're sorting through these issues, it helps to understand Texas uninsured and underinsured coverage.

What to do in this kind of case

Handle these cases carefully from the start:

- Report the crash promptly: Your insurer will usually require notice.

- Preserve every record: Keep photos, repair estimates, medical records, and witness information.

- Ask for denials in writing: If an insurer refuses part of the claim, written reasons matter.

- Watch for fault disputes: Even in a hit-and-run or uninsured-driver case, the insurer may still examine your actions closely.

Why these claims can feel so frustrating

People expect their own insurer to be easier to deal with. Sometimes it is. Sometimes it still becomes a fight over coverage, medical proof, or fault.

That's especially true when the injuries are serious or the facts are incomplete. A hit-and-run at night, for example, may leave you with no other driver to identify, no easy witness, and a damaged vehicle that needs immediate attention. In that situation, the strength of your records becomes even more important.

Do You Need a Texas Personal Injury Lawyer

A week after the crash, many people are still hearing the same thought in their head: I know the wreck was not my fault, so why does this already feel so hard?

That is usually the point where legal advice starts to help. A lawyer is not only for filing a lawsuit. In many cases, a lawyer helps you protect the claim before it gets weaker. That can mean stopping careless statements, gathering the right records, dealing with adjusters, and sizing up whether a settlement offer covers what the crash has cost you.

Some cases stay fairly straightforward. Others get complicated fast.

You should seriously consider talking with a Texas personal injury lawyer if the facts, injuries, or insurance issues are starting to outgrow what you can reasonably handle on your own.

Signs it's time to get legal advice

Certain warning signs tend to show up early:

- Fault is being challenged: The other driver or insurer says you caused all or part of the crash.

- Your injuries are lasting longer than expected: You need follow-up care, specialist treatment, physical therapy, or time away from work.

- The insurer wants a quick statement or quick settlement: Early offers often come before the medical picture is clear.

- Several parties may be involved: Multi-vehicle wrecks, company vehicles, and commercial trucks often bring added layers of insurance and investigation.

- A family is dealing with the worst outcome: Fatal crash cases raise questions that are far more serious than a routine property-damage claim.

A simple way to look at it is this. If your case involves more than car repairs and a short doctor visit, getting legal advice early often helps you avoid expensive mistakes later.

Deadlines matter, but timing matters even more

Texas law gives injured people a limited window to file many personal injury lawsuits. In car crash cases, that deadline is often two years from the date of the accident, though exceptions can apply in some situations.

Waiting creates problems long before the deadline arrives. Surveillance footage can be erased. Witnesses forget details. Vehicles get repaired or sold. Medical gaps show up in the records, and insurers may use those gaps to argue that you were not seriously hurt.

That is why I often tell clients to treat a case like preserving footprints after a storm. The longer you wait, the less clear the path becomes.

What a lawyer actually does in a not-at-fault case

People sometimes worry that hiring a lawyer means turning everything into a fight. Usually, it means bringing order to a process that already feels scattered.

A lawyer can help you:

- identify what evidence still needs to be collected

- deal with insurance adjusters so your words are not taken out of context

- calculate losses beyond the first repair bill or emergency room visit

- watch for blame-shifting under Texas fault rules

- prepare the case for settlement, and for court if the insurer refuses to be reasonable

That last point matters. Insurance companies evaluate risk. A well-prepared claim tells them you are organized, documented, and ready to prove what happened.

Good legal help is often less about aggression and more about protection, clarity, and timing.

If you are asking yourself whether you need a lawyer, the question is often a sign that a consultation would help. You do not need to have every document sorted out first. You need a clear roadmap, an honest case assessment, and a plan for the next step.

You Don't Have to Face This Alone Your Recovery Is Our Priority

If you've been hurt in a crash that wasn't your fault, the biggest thing to remember is this. You do have options.

Texas law can allow recovery after a car wreck, truck collision, or other serious crash, but the process depends on what you do next. Your actions at the scene matter. Your medical records matter. Your communication with insurers matters. And if fault becomes a dispute, the quality of your evidence may shape the result.

That can feel like a lot when you're already trying to heal. But you don't have to solve it all on your own. With the right guidance, people can move from confusion to clarity. They can protect their claims, challenge unfair blame, and pursue compensation that reflects the full impact of the accident.

Recovery is possible. Legal help is available. And the fact that the crash disrupted your life doesn't mean it gets to define your future.

If you need answers about a crash in Texas, Law Office of Bryan Fagan, PLLC offers free consultations for accident victims and families. You can talk through what happened, learn what steps make sense next, and get clear guidance on protecting your rights after a car, truck, catastrophic injury, or wrongful death case.