A serious accident can change your life in seconds, but you don’t have to face it alone.

If you’re reading this, you may be dealing with pain, missed work, medical appointments, calls from insurance adjusters, and a lot of uncertainty. You may also be wondering whether you even have a case, whether you waited too long, or whether hiring a Texas personal injury lawyer will just add more stress.

It doesn’t have to. The right plan can protect both your health and your claim.

A strong personal injury law firm texas guide should do more than tell you to “call a lawyer.” It should help you understand why each step matters, what mistakes can hurt your case, and how Texas law affects the money you may recover. That’s what this roadmap is meant to do.

Your Guide to Recovery After a Serious Texas Accident

After a wreck on a Houston freeway, a truck crash outside Dallas, a workplace vehicle collision in San Antonio, or a fatal crash near Austin, individuals don’t need legal jargon. They need clear answers.

The first priority is always your safety and medical care. The second is protecting the evidence that proves what happened and how badly you were hurt. The third is making smart decisions before an insurance company shapes the story for you.

That sequence matters.

A good claim isn’t built by one dramatic moment in court. It’s usually built by ordinary steps taken early and taken well. Getting checked by a doctor, preserving photos, keeping follow-up appointments, and refusing to guess when an adjuster asks loaded questions can make a major difference in the result.

Practical rule: Your case starts long before a lawsuit is ever filed. It starts with what you do in the hours and days after the accident.

Whether you need a Houston car accident attorney, a truck crash lawyer Houston, or guidance after a fatal collision that may involve a wrongful death lawyer Texas families can trust, the same core idea applies. Your recovery improves when you act with purpose.

Immediate Actions to Take After a Texas Accident

The first few hours after a crash feel chaotic. That’s exactly why a simple sequence helps.

Start with safety and a police report

If you can, move to a safe location and call 911. Even when injuries seem minor, police involvement matters because an officer’s report often becomes the first neutral record of where the crash happened, who was involved, and what conditions existed at the scene.

After a Houston freeway crash or a multi-car collision on I-610, people often feel pressure to sort things out quickly on the shoulder. Don’t rush into conversations about fault. Exchange information, cooperate with law enforcement, and stick to basic facts.

Ask for medical help if anyone may be injured. If you’re dizzy, disoriented, in pain, or unsure, say so.

Get medical care before symptoms get worse

A lot of injury victims say the same thing: “I felt okay at first.” That can happen after a serious collision. Adrenaline can mask pain, and some injuries become more noticeable later.

Medical care does two things at once. It protects your health, and it creates a record connecting the injury to the accident. If you wait too long, the insurance company may argue that something else caused your pain.

A practical approach is:

- Accept evaluation at the scene if needed. Don’t downplay symptoms just because you want to get home.

- Follow up promptly after release. Go to urgent care, your doctor, or the ER if symptoms appear or intensify.

- Follow the treatment plan. Gaps in treatment give insurers room to argue that you weren’t badly hurt.

Tell every provider where you hurt, what movements trigger pain, and when symptoms started. Incomplete medical histories create avoidable problems later.

Preserve the scene while it still exists

Evidence fades fast. Cars get moved. Debris gets cleared. Witnesses leave. Memories soften.

If you can safely do it, gather:

- Photos of vehicle damage: Get multiple angles, skid marks, traffic signals, lane positions, broken glass, and road conditions.

- Contact details for witnesses: A short name and phone number can become valuable later.

- Driver and insurance information: Confirm spelling, plate numbers, and policy details.

- Your own immediate observations: Note pain, weather, lighting, and anything the other driver said.

If there’s dashcam footage, save it right away. Don’t assume it will stay stored indefinitely.

Watch what you say at the scene

People often say “I’m sorry” out of politeness. After a crash, that can be misunderstood.

You can be respectful without making statements that sound like blame. Say, “Are you okay?” or “Let’s wait for the police.” Don’t speculate about speed, distance, or whether you “could have avoided it.” Those guesses often come back later.

The first day at home matters too

When you get home, start a simple accident file. Put all discharge papers, prescriptions, receipts, towing records, and repair information in one place.

Also keep a short daily note about your symptoms. If your back pain worsens at night, if headaches start after screen time, or if you need help bathing, dressing, or sleeping, write it down. Small details often explain the impact of an injury better than a billing statement does.

For a broader step-by-step checklist, review this guide on what to do after a car accident.

What not to do in the first 72 hours

Some mistakes hurt claims more than people realize:

- Don’t post about the accident online. A smiling photo from dinner can be twisted into “proof” that you’re not injured.

- Don’t skip follow-up care. Missing appointments makes your case harder to document.

- Don’t repair or discard damaged property too quickly. Visible damage may help show impact severity.

- Don’t give the other driver’s insurer a recorded statement. You’re usually better off waiting until you understand your injuries and rights.

A serious accident disrupts everything. But if you handle the first 72 hours carefully, you protect the foundation of your case.

Protecting Your Claim from Insurance Company Tactics

Insurance companies move fast for a reason. They want to control the story before the evidence is complete and before you understand the value of your claim.

That doesn’t mean every adjuster is hostile. It does mean their job is to resolve claims efficiently and protect the company’s money, not your future care.

Why some evidence matters more than other evidence

Not all proof carries the same weight. In practice, certain records do more work than others.

The strongest claims usually combine three types of proof:

- Liability evidence: Police reports, video, dashcam footage, scene photos, and witness statements.

- Medical proof: Records showing diagnosis, treatment, imaging, restrictions, and ongoing complaints.

- Long-term impact evidence: Information showing disability, work limits, future care needs, or wage loss.

That evidence hierarchy matters because insurers pay more attention to documented facts than to unsupported descriptions. According to WK Firm’s discussion of injury claim evidence, cases with thorough evidence, including clear liability documentation, corroborating witness testimony, and complete medical records, command settlement offers 40-60% higher than cases with incomplete documentation.

That doesn’t mean every case with good evidence settles well. It means documentation impacts negotiating strength.

The quick settlement trap

One common tactic is the early settlement offer. It may come before you know whether you’ll need more treatment, physical therapy, specialist care, or time away from work.

That money can look helpful when bills are piling up. But once you sign a release, you usually can’t go back and ask for more because your symptoms lasted longer than expected.

After a rear-end crash, for example, neck and back pain may seem manageable in the first week and become disruptive later. If you settle too early, you carry that risk yourself.

A fast offer isn’t always a fair offer. It’s often an attempt to close the file before the medical picture is complete.

Recorded statements and loaded questions

Adjusters often sound casual. The questions are not.

They may ask, “You’re feeling better now, right?” or “You didn’t see my insured until the last second?” Those questions are designed to lock you into wording that weakens your case.

A safer approach is simple:

- Confirm basic facts only. Your name, contact information, and the date and location of the crash.

- Decline detailed recorded statements. Say you’re still receiving medical evaluation and aren’t prepared to discuss injuries yet.

- Don’t estimate. If you don’t know speed, distance, or timing, say you don’t know.

If you need help with that conversation, this resource on what to say to insurance after an accident gives practical guidance.

What actually strengthens your position

People often think a claim becomes stronger because they’re angry or because the other driver was rude. Neither one changes value. Proof does.

A stronger file usually includes:

| Evidence Category | Why It Matters | Example |

|---|---|---|

| Liability records | Helps show who caused the crash | Police report, intersection video |

| Medical records | Connects injuries to the accident | ER chart, imaging, specialist notes |

| Witness support | Confirms your account | Independent bystander statement |

| Daily impact notes | Shows how life changed | Missed sleep, driving limits, pain at work |

If you’re dealing with a commercial carrier, rideshare insurer, or a serious injury case, preserving this material early can be the difference between a disputed claim and a credible demand.

Understanding Your Rights Under Texas Personal Injury Law

A serious crash can leave you dealing with pain, bills, missed work, and a lot of pressure to make decisions fast. Texas law sets the rules for who can recover money, how shared fault affects the case, and how long you have to act. Once you understand those rules, you can make smarter choices and avoid mistakes that give the insurance company an advantage.

Fault and negligence in plain English

Most Texas injury claims are built on negligence. The question is whether another person or business failed to use reasonable care and caused your injury.

That may involve a driver who ran a red light, a trucking company that ignored maintenance problems, or a property owner who left a known hazard unaddressed. Lawyers describe this in formal terms such as duty, breach, causation, and damages. For an injured person, the practical issue is simpler. What happened, who had the responsibility to prevent it, and what proof connects that conduct to your losses?

That "why" matters. If you know why a fact helps prove fault, you are less likely to overlook evidence that seems small at first but becomes important later.

Comparative responsibility can reduce recovery

Texas follows modified comparative fault. The rule many injury victims need to know is the 51% bar. You can recover damages if you are 50% or less responsible, but your recovery is reduced by your percentage of fault. If you are 51% responsible or more, Texas law bars recovery.

A simple example shows how this works. If a case is worth $100,000 and the injured person is found 20% at fault, the recovery drops to $80,000.

That is why fault disputes matter so much. Insurance adjusters often look for facts they can use to assign part of the blame to you. In a car wreck case, that may mean arguing you were distracted, following too closely, driving too fast for conditions, or failed to react soon enough. In a premises case, they may claim the danger was open and obvious. The legal rule is straightforward, but the fight is usually over evidence and framing.

How long do you have to file a claim in Texas

Texas personal injury cases usually have a two-year statute of limitations. In many cases, that means a lawsuit must be filed within two years of the injury.

Waiting is risky for reasons that have nothing to do with the calendar alone. Evidence fades fast. Video gets deleted. Vehicles are repaired. Work records get harder to collect. Witnesses forget details or stop responding. Early action is not just about meeting a deadline. It is about preserving the proof that gives your claim value and puts you in a stronger position if the other side denies responsibility.

Some cases also involve exceptions, shorter notice requirements, or facts that change when the clock starts. Claims involving minors, government entities, or delayed discovery issues can require a closer legal review.

Special concern in fatal injury claims

Fatal accident claims raise separate legal and practical questions. Families may have the right to pursue a wrongful death claim, and the estate may also have a survival claim depending on the facts. Those are different claims with different purposes, which is one reason early legal advice matters.

In some cases, the cause of death is disputed or there are unanswered medical questions. Families sometimes consider private autopsies to preserve evidence and clarify what happened. This resource on wrongful death cases explains why that issue can matter.

This video also gives helpful background on Texas injury law and claim issues:

What these rules mean for you

Your rights under Texas law are not just abstract rules in a statute book. They shape strategy from the beginning. Who can be held responsible, whether shared fault will be argued, what evidence needs to be preserved, and how fast formal action must be taken all affect the outcome.

Ask direct questions early. Who may be liable? What evidence could disappear? Is there a limitations issue? Is the defense likely to argue you were partly at fault? Clear answers to those questions help protect your claim and put you in a better position to recover the damages the law allows.

What Is Your Texas Injury Claim Really Worth?

This is usually the question people ask first, even if they feel uncomfortable saying it out loud. The honest answer is that claim value depends on the facts, the injuries, the proof, and the insurance available.

It also depends on the type of damages involved.

The three main categories of damages

Some losses are easy to identify on paper. Others are very real but harder to measure.

Here’s a clear breakdown:

| Damage Type | What It Covers | Examples |

|---|---|---|

| Economic damages | Financial losses tied to the injury | Medical bills, lost wages, property damage, future care |

| Non-economic damages | Human losses that don’t come with a simple invoice | Pain, suffering, emotional distress, reduced quality of life |

| Punitive damages | Damages meant to punish extreme misconduct in limited cases | Egregious drunk driving or other gross negligence situations |

Economic damages are the starting point

Economic damages are usually the easiest part of a claim to document. Bills, wage records, pharmacy receipts, mileage to medical visits, and repair estimates all help show direct financial loss.

But even these numbers can be understated if the injury is serious. A broken bone may heal. A brain injury, spinal injury, or severe orthopedic injury may affect future earning ability, household independence, and long-term treatment.

That’s one reason catastrophic injury cases often look very different from routine soft-tissue claims.

Non-economic damages often drive the real dispute

Pain and suffering isn’t “extra” money. It’s compensation for what the injury changed.

Maybe you can no longer sleep through the night. Maybe you can’t pick up your child, return to the same job, or tolerate a long drive without pain. Maybe your spouse has watched your personality change after a brain injury or trauma.

Those losses matter, but insurers often challenge them because they aren’t shown by a single bill. Good medical records, consistent treatment, and testimony from people who know you can make those damages more concrete.

The value of a case isn’t just what you paid. It’s also what the injury took from your daily life.

Punitive damages are different

Punitive damages are not available in every case. They generally come into play when the conduct goes beyond ordinary carelessness and looks more like gross negligence.

That issue can arise in some drunk driving cases, extreme safety violations, or other reckless conduct. These claims require a careful factual analysis and often stronger proof than a standard negligence case.

Why verdict headlines can be misleading

People often search online and see huge verdicts. Those cases are real, but they don’t tell the whole story.

According to Lawsuit Information Center’s review of Texas personal injury verdicts, the average Texas personal injury verdict is $826,892, while the median is $12,281. That gap matters. It shows how a small number of catastrophic injury and wrongful death verdicts can pull the average upward, while many cases resolve for much less.

The same source notes that Texas juries can return very large awards in severe cases, including a nearly $72 million wrongful death verdict in May 2024 involving a Frito-Lay warehouse accident, while statutory limits can also sharply reduce recovery in some categories, including medical malpractice cases.

That’s why any honest case evaluation has to look beyond headlines. A fair estimate should consider liability strength, injury severity, treatment history, insurance coverage, and whether long-term losses can be proven.

Wrongful death damages bring added burdens

When a family loses someone in a fatal crash, the financial impact can include lost support, lost services, and final expenses, on top of emotional devastation.

Families often also need immediate practical information while they grieve. If you’re trying to understand burial and service expenses, this guide to Texas funeral costs may be useful as a starting point.

A wrongful death lawyer Texas families consult should be able to explain both the legal claim and the immediate realities that follow a fatal loss.

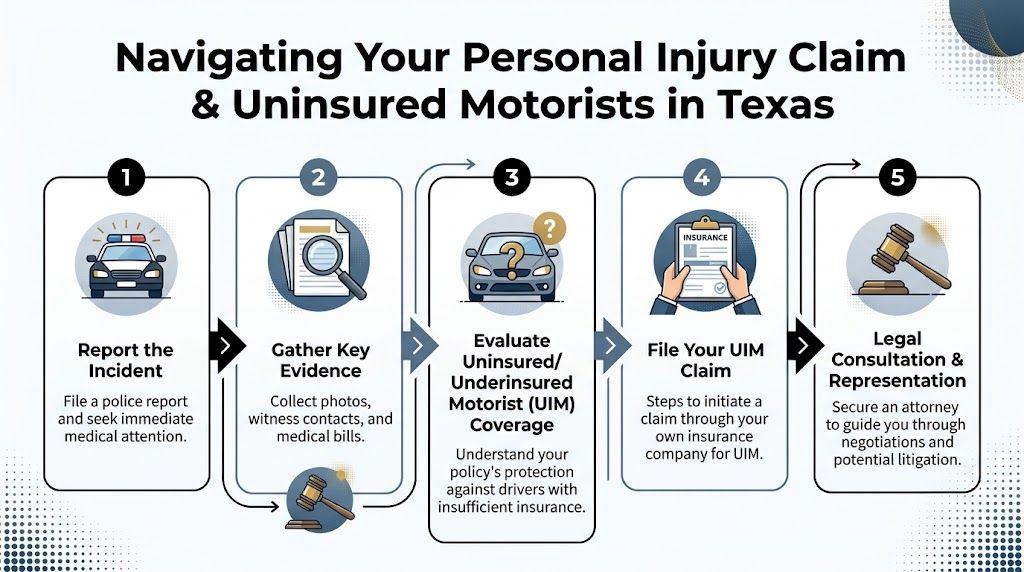

Navigating the Legal Process and Uninsured Motorists

A serious crash can leave you dealing with two fights at once. One is your physical recovery. The other is a claim process that gets harder when the driver who caused the wreck has no insurance or too little coverage.

What the legal process usually looks like

In a Texas injury case, the order of events matters. Early mistakes can give the insurance company room to question fault, treatment, or the value of the claim later.

A typical case starts with investigation. That means gathering the crash report, photos, witness information, vehicle damage evidence, medical records, and proof of lost income. At the same time, medical treatment continues so the full extent of the injury becomes clearer.

Once the facts and damages are documented well enough, a demand package may go to the insurer. Negotiations usually follow. If the carrier disputes liability or refuses to pay a fair amount, the case may need to be filed in court.

Many claims still resolve before trial, but preparation still drives results. An insurer pays closer attention when the file shows clear evidence, consistent treatment, and a willingness to prove the case in court if needed.

Uninsured and underinsured claims require a different strategy

A lot of injured Texans are surprised by this part. If the at-fault driver has no coverage, or carries only a small policy, your own insurance company may become the company on the other side of the dispute.

That does not mean the claim becomes informal or friendly. Your carrier may still challenge fault, argue that treatment was excessive, dispute whether the wreck caused your symptoms, or undervalue pain and lost income. In practical terms, you still have to build the case the same way you would against the other driver.

If you are not sure what your policy includes, this guide to Texas uninsured and underinsured motorist coverage is a good place to start.

A practical roadmap for UM and UIM claims

The strongest UM or UIM claims usually follow a disciplined sequence:

- Confirm coverage early: Get the declarations page and check whether UM/UIM coverage exists, whether it was rejected in writing, and what limits apply.

- Give notice promptly: Delays can create avoidable disputes with your own carrier.

- Build the liability file: Even if the other driver was clearly at fault, do not assume the insurer will accept that without proof.

- Track treatment carefully: Gaps in care, missed appointments, and vague complaints are common attack points.

- Review requests before responding: Recorded statements, broad medical authorizations, and release forms can affect the value of the claim.

The reason for each step is simple. UM and UIM cases often turn on documentation, timing, and policy language, not just on whether the crash happened.

Consider a common Texas example. A driver is rear-ended on the way home from work. The other motorist has a low-limit policy, but the injured driver needs imaging, follow-up care, physical therapy, and time away from work. The liability coverage may be exhausted quickly. Underinsured motorist coverage can then become a major source of recovery, but only if the claim is presented in the right order and supported with solid records.

What helps in negotiation

Good negotiation is rarely about saying the same thing louder. It is about removing excuses the insurer could use to pay less.

| Approach | Why It Helps |

|---|---|

| Organized records | Shows the timeline clearly and makes damages harder to minimize |

| Consistent treatment | Connects the crash to the injury and supports seriousness |

| Clear proof of fault | Limits attempts to shift blame onto you |

| Trial-focused preparation | Puts real pressure on the insurer to evaluate the case fairly |

A weak approach usually looks different. People rely on phone calls instead of written confirmation, send incomplete records, accept delay after delay, or treat a denial as final. In many cases, a denial is the start of the dispute, not the end of it.

Choosing help at the right stage

Some claims stay manageable for a while. Others call for legal help early, especially when there is a serious injury, a commercial vehicle, a death, disputed fault, or an uninsured or underinsured driver.

One option is Law Office of Bryan Fagan, PLLC, which handles Texas motor vehicle injury claims, wrongful death matters, catastrophic injury cases, and uninsured driver disputes. The key is choosing counsel that can investigate early, deal directly with the insurer, and build the case with the end result in mind, not just the next phone call.

When to Hire The Law Office of Bryan Fagan, PLLC

Some people call a lawyer the same day as the crash. Others wait until the adjuster stops returning calls, the offer feels too low, or the medical issues become harder than expected.

In general, the right time to hire counsel is when the case starts affecting your health, income, or future in a serious way. That includes cases involving surgery, permanent symptoms, disputed fault, commercial trucks, fatal injuries, or uninsured drivers.

Cost is usually less of a barrier than people think

A lot of injured people delay because they assume they can’t afford representation. In Texas personal injury practice, that’s usually not how payment works.

According to Clio’s personal injury law statistics overview, personal injury firms typically work on a contingency fee basis, with an industry standard of 33.3% of the settlement. That means the fee is tied to recovery rather than an upfront retainer.

That structure matters for regular families. It lets you get legal help without paying out of pocket at the beginning of the case.

When legal help makes the biggest difference

Hiring a lawyer tends to matter most when:

- Liability is disputed: The insurer is trying to put blame on you.

- Injuries are serious: Your treatment is ongoing or your doctors are discussing long-term effects.

- The claim involves death or catastrophic harm: A family needs help gathering records and valuing losses.

- Coverage is complicated: There may be multiple policies, low limits, or UM/UIM issues.

- A lawsuit may be necessary: Negotiation only works when the other side believes you’re prepared to go further.

If you need a Houston car accident attorney, a truck crash lawyer Houston, or a wrongful death lawyer Texas families can turn to after a fatal wreck, legal support should reduce your burden, not add to it.

You shouldn’t have to figure this out while you’re in pain, grieving, or trying to hold your household together.

If you were hurt in a Texas crash, or if your family lost someone because another person acted carelessly, help is available. You can contact the Law Office of Bryan Fagan, PLLC to schedule a free consultation, get clear answers about your rights, and talk through the next steps with a Texas personal injury lawyer. Recovery is possible, and you don’t have to pursue it alone.