A serious accident can change your life in seconds, but you don't have to face it alone.

You may be reading this from a hospital room, your living room couch, or the repair shop parking lot, asking one urgent question: How much can someone sue for a car accident in Texas? The honest answer is that there isn't one fixed number. A serious claim may be worth far more than the at-fault driver's first insurance offer, and in some cases far more than the driver's basic policy limits.

After a Houston freeway crash, many people assume the insurance company will readily pay "the maximum" and the case is over. That's often where confusion starts. Your case value depends on what the crash cost you, how Texas fault rules apply, what insurance exists, and whether other sources of recovery are available.

If you're dealing with headaches, dizziness, or delayed symptoms after a wreck, medical follow-up matters. Practical post-crash guidance like this expert advice from The Patients Guide can help you take symptoms seriously while your legal claim develops.

Your Life Changed in an Instant Now What

One moment you're driving to work, picking up your child, or heading home on I-45. The next, you're talking to police, answering calls from insurance adjusters, and trying to figure out whether your injury will heal or change your life for good.

That shock makes people look for a simple answer. They want one number. They want certainty. Texas law doesn't work that way.

Why there isn't one dollar amount

In a standard negligence case against a private person in Texas, there isn't a general statutory cap that sets one maximum amount for an ordinary car wreck claim. The value turns on your economic losses, your non-economic harm, the strength of the evidence, and whether Texas fault rules reduce recovery.

Practical rule: Your claim is not measured by the insurance card alone. It's measured by the harm the crash caused in your life.

Two people can be hurt in similar collisions and have very different cases. One may recover after chiropractic care and a short time off work. Another may need surgery, months of treatment, and help with daily tasks. The second claim will usually be much larger because the losses are larger.

Where people get misled

A lot of injured Texans hear that the other driver has "full coverage" or only "minimum coverage" and assume that's the same as the value of the case. It isn't. Insurance limits affect where money may come from. They don't automatically define what your losses are worth.

That's why the better question isn't just "How much can someone sue for a car accident in Texas?" The better question is, what is the full value of what this crash took from you, and how can you collect it?

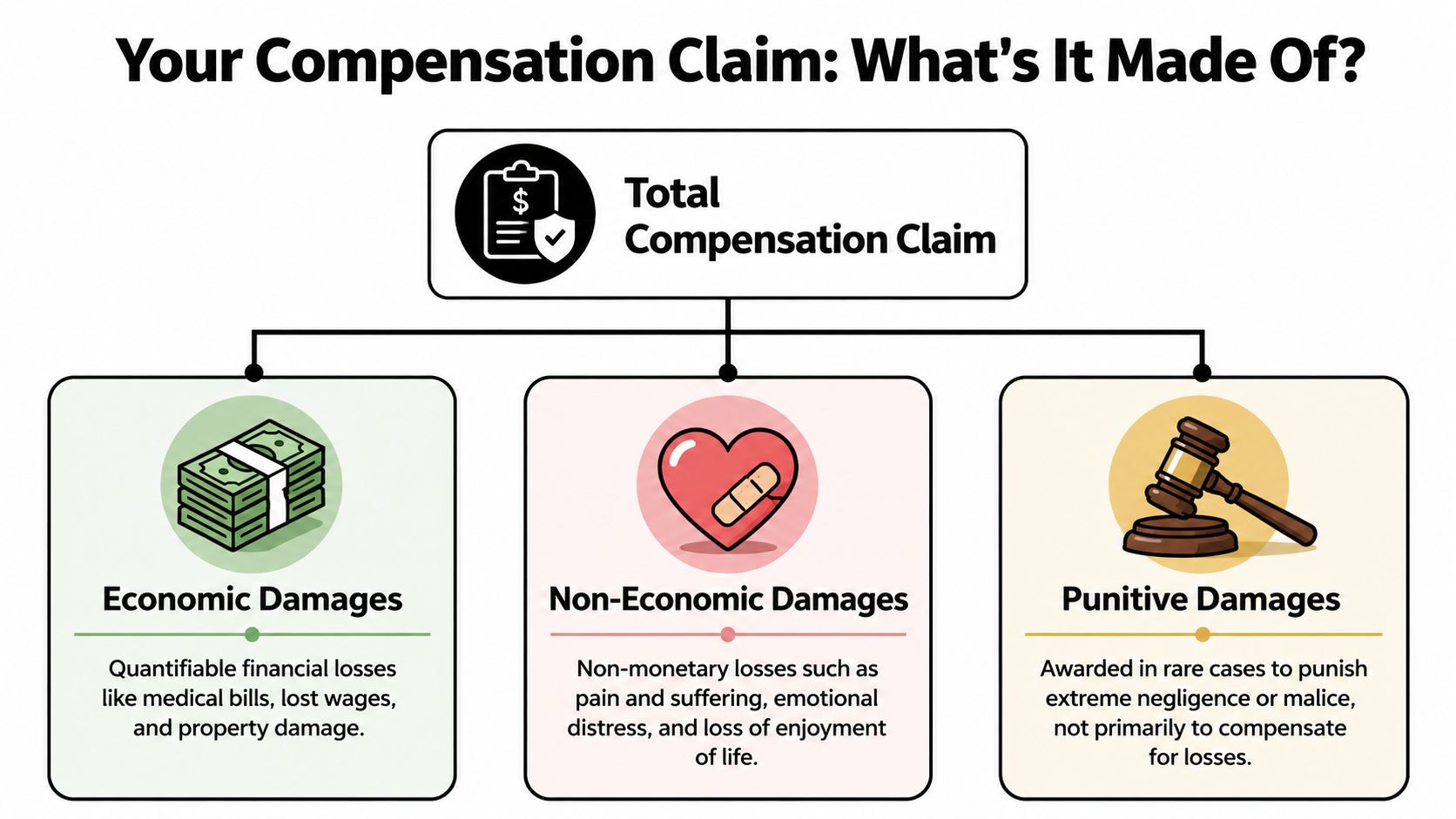

The Building Blocks of Your Compensation Claim

Before you can value a case, you need to know what belongs in it. Most claims are built from different categories of damages, not one lump sum. That distinction matters because insurance companies often focus on the easiest numbers and downplay everything else.

Economic damages

These are the concrete financial losses you can usually document with bills, receipts, pay records, and estimates.

Economic damages often include:

- Medical care: Emergency treatment, hospital bills, follow-up appointments, physical therapy, prescriptions, and future care tied to the crash.

- Lost income: Wages you missed while recovering, plus reduced earning ability if you can't return to the same work.

- Property damage: Vehicle repair or replacement and other damaged personal property.

- Out-of-pocket costs: Transportation to appointments and other necessary expenses caused by the injury.

If you want a clearer breakdown of these categories, this guide on economic vs. non-economic damages is a useful starting point.

Non-economic damages

These losses don't come with a neat invoice, but they are still real. Pain, physical limitations, emotional distress, and the loss of normal daily life often shape the true weight of a serious injury case.

A parent who can't lift a child. A worker who can't sleep because of back pain. A spouse who lives with constant anxiety after a violent collision. Those harms may not show up on a repair estimate, but they matter.

Serious injury claims are often undervalued when people count bills and ignore how the injury changed ordinary life.

For a practical overview of the categories involved, What Damages Can You Recover in a Texas Injury Case? outlines the categories of compensation available to Texas injury victims.

Punitive damages

Punitive damages are different. They are not mainly about repaying your losses. They may come into play in rare cases involving extreme misconduct, such as conduct resembling drunk driving or other especially dangerous behavior. They are not part of every case, and most claims turn primarily on economic and non-economic damages.

Why injury severity matters so much

Settlement values vary widely. Verified data states that there are no statewide average settlement statistics for Texas, but the average bodily injury settlement in the U.S. for 2022 was $26,501, while Texas cases involving minor to moderate injuries often range between $20,000 and $30,000. That same verified data states that severe or catastrophic injuries can result in settlements from $500,000 to over $1 million (Fact 9).

Here is the practical takeaway:

| Type of harm | What often drives value |

|---|---|

| Minor to moderate injuries | Length of treatment, missed work, documented pain |

| Surgery-related injuries | Medical costs, recovery time, lasting impairment |

| Catastrophic injuries | Future care, permanent disability, life impact |

The bigger the disruption to your health, income, and daily life, the bigger the claim usually becomes.

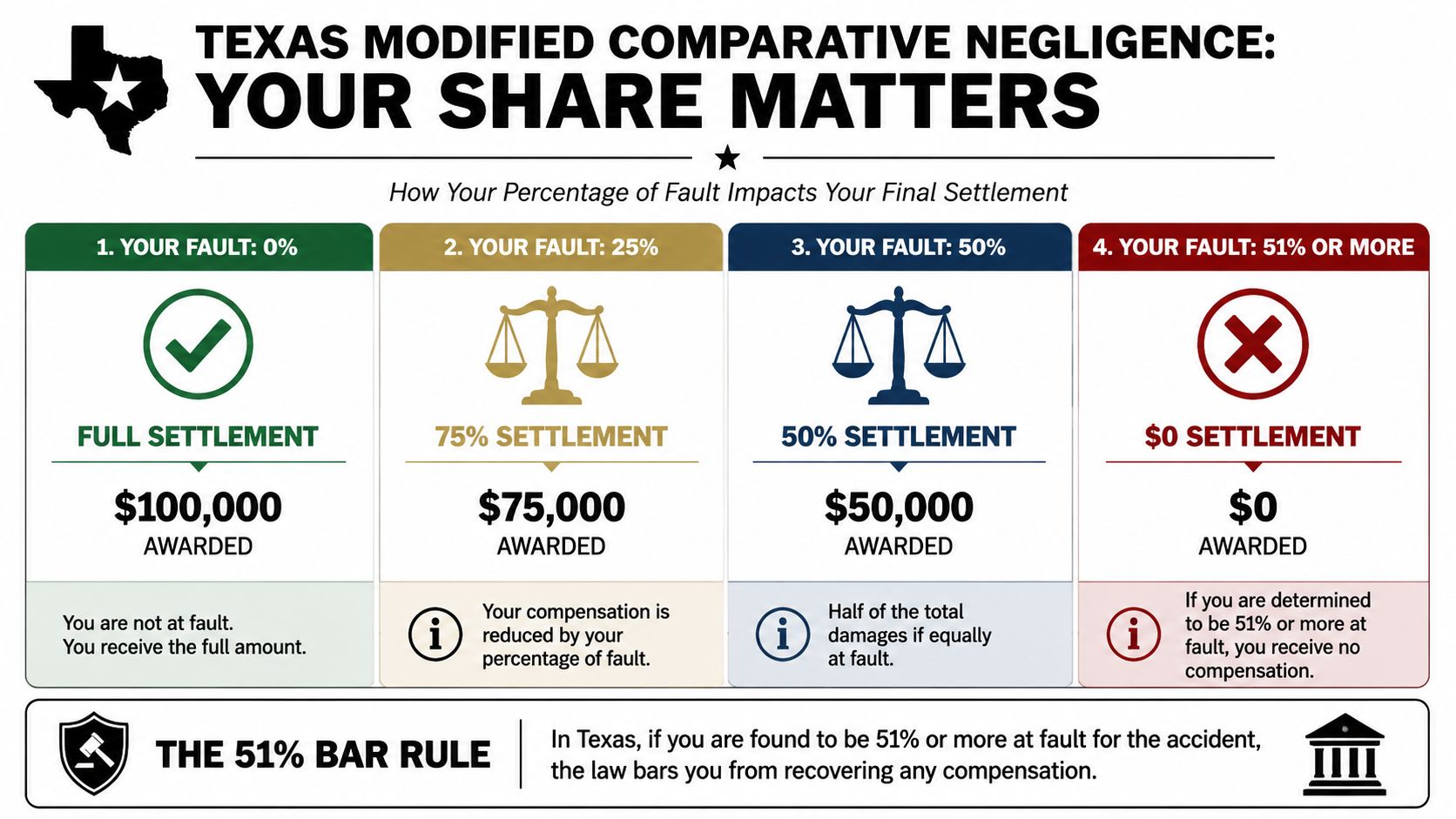

How Texas Law Can Impact Your Final Settlement

Your injuries may be serious. Your medical bills may be real. Even so, Texas law can still reduce what you recover if the other side persuades an adjuster, judge, or jury that you share part of the blame for the crash.

That catches many injured people off guard.

The 51 percent bar rule

Texas follows modified comparative fault. In plain terms, your compensation can be reduced by your share of fault. If you are 51% or more at fault, you recover nothing. If you are 50% or less at fault, you can still recover, but the amount is reduced to match your percentage of responsibility. You can read a fuller explanation on how comparative fault affects settlement in Texas.

The rule is easier to understand with numbers. If your damages are $100,000 and you are found 30% at fault, your recovery drops to $70,000. Verified guidance summarized in Fact 7 uses that same example and confirms that recovery is barred at 51% or more fault.

Fault percentages matter because they change the value of the claim before anyone even gets to the question of who can pay it. In a serious injury case, that reduction can create a large gap between what you need and what you ultimately receive.

Why insurers argue about fault so aggressively

Insurance companies often focus on fault because it is one of the fastest ways to cut the amount they may have to pay. They may argue that you were speeding, following too closely, distracted, tired, or that you had enough time to avoid the crash.

A rear-end wreck is a good example. Many people assume the driver in back is always fully responsible. Often that is true. But an insurer may still claim you braked suddenly, had broken brake lights, or made an unsafe lane change right before impact. In a chain-reaction crash, the finger-pointing usually gets worse because each insurer tries to shift part of the blame to someone else.

That is why early evidence matters so much. Photos, witness names, dashcam video, black box data, and the crash report can help show what really happened before memories fade and stories start changing.

A short video can help make that concept easier to follow.

Deadlines can end a valid claim

Texas law also sets a strict time limit for filing most car accident injury lawsuits. In most cases, the deadline is two years from the date of the crash.

For example, if a wreck happened on January 15, 2023, the lawsuit usually had to be filed by January 15, 2025. Miss that deadline, and the court can dismiss the case even if your injuries are severe and the other driver was clearly at fault, as summarized in Fact 6.

That deadline matters for another reason. Serious cases often take time to understand fully. A person may still be treating, missing work, or learning whether the injury will cause permanent problems. Starting early gives your lawyer time to gather evidence, identify every possible source of recovery, and protect the claim before the clock runs out.

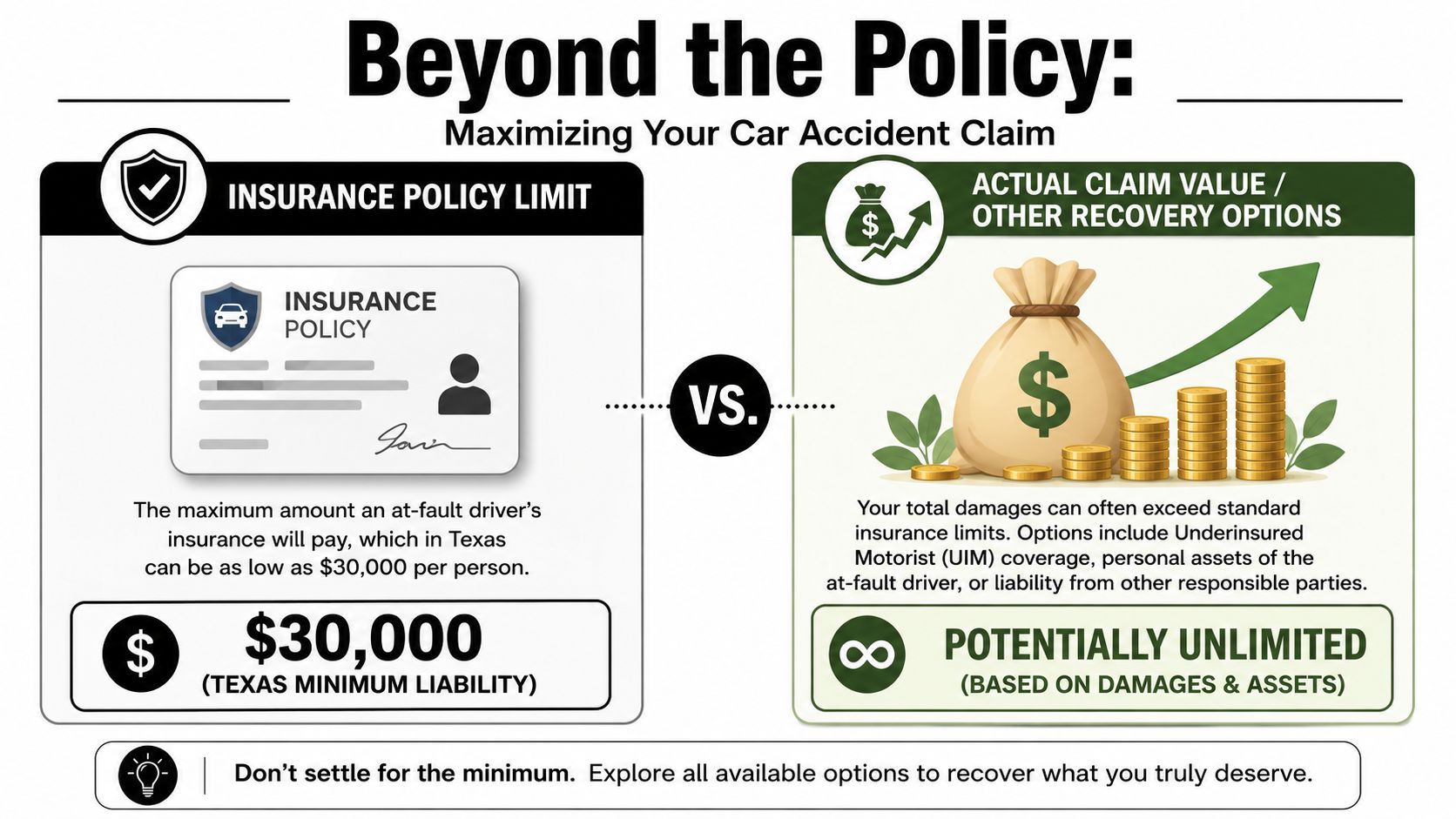

Why an Insurance Policy Limit Is Not Your Claim's Limit

Many serious cases go off track. A person learns the at-fault driver carries minimum insurance, hears a low number, and assumes that's all there is.

In Texas, the minimum required liability coverage is 30/60/25. That means $30,000 for bodily injury per person, $60,000 total per accident for bodily injury, and $25,000 for property damage. But that minimum policy only limits the insurer's initial payout. It does not automatically cap the value of your claim.

The floor and the ceiling are different

Verified Texas-specific data makes this clear. Texas requires the minimum 30/60/25 policy, which can limit an insurer's initial payment to $30,000 per person, but an injured person can still sue for the full value of the injuries. The same verified data states that minor accidents may settle near that range, while catastrophic Texas cases have produced verdicts and settlements from over $1 million to $4.5 million (Fact 1).

That is the gap many people miss. The policy limit is often the start of the collection problem, not the end of the case value analysis.

Ways people may recover beyond the other driver's basic policy

If your losses are greater than the at-fault driver's insurance, several paths may still exist:

- Your own UIM coverage: Underinsured motorist coverage may help when the other driver's policy isn't enough. This overview of underinsured motorist coverage in Texas explains that option in more detail.

- Personal assets of the at-fault driver: In some cases, a judgment can be pursued beyond insurance.

- Other liable parties: A commercial employer, vehicle owner, rideshare company issues, or another negligent driver may expand the available recovery.

Why early offers can be misleading

An adjuster may talk as if the claim is simple. If your injuries are serious, it usually isn't. The insurer may offer the available policy limit quickly, hoping you'll treat that number as final without looking for other coverage or defendants.

A Houston car accident attorney often investigates whether there are additional policies, umbrella coverage, employer involvement, or other facts that change the financial picture. In the right case, a claim that first looked small can become much larger because the available recovery sources were not obvious on day one.

A Real-World Example of a Texas Car Accident Claim

After a serious crash on I-610 in Houston, a driver is taken to the hospital with a broken leg, a head injury, and weeks of missed work ahead. The other driver admits he drifted into the lane, but later the insurer argues the injured driver may also share some blame because traffic was moving fast and both vehicles changed position just before impact.

The first thing people usually want to know is how the math works in real life. Start with the damages.

What the case may include

Suppose the injured driver has:

- substantial medical bills from emergency care, follow-up treatment, and rehabilitation

- lost pay because work was missed during recovery

- ongoing pain, limited mobility, and anxiety about driving

- major vehicle damage

Those losses create the value of the case. The exact amount depends on records, testimony, and how long the injury lasts. If the broken leg heals well, the claim may look one way. If the head injury creates lasting problems, the value may be much higher.

Where fault changes the result

Now add Texas comparative responsibility. If the evidence shows the other driver was mostly responsible but the injured driver also made a smaller mistake, the final recovery can be reduced by that share of fault.

For example, Texas law recognizes that a person found partly at fault can still recover if they stay below the bar discussed earlier. In practice, that means even a good claim can lose value when fault is divided. The better the evidence, the better your chance of protecting the full value of the case.

In a close-liability crash, the fight is often not just about what your injury is worth. It's about who gets blamed for it.

This is also why some collisions need a different level of investigation. If the crash involved a delivery van, company pickup, semi-truck, or contractor vehicle, a truck crash lawyer Houston families trust may need to review driver logs, company records, vehicle maintenance, and corporate insurance layers that don't exist in an ordinary two-car wreck.

If the collision caused a fatality, the case may shift into a family claim handled by a wrongful death lawyer Texas families can turn to for answers about funeral costs, lost support, and the human loss left behind.

Steps You Must Take to Protect Your Right to Compensation

The first days after a serious crash often feel like a blur. You may be trying to manage pain, answer insurance calls, arrange a ride, and figure out how you will pay the next bill. What you do during this period can protect both your health and your claim, especially if your injuries are worth far more than the at fault driver's minimum coverage.

Start with your health and the basic proof

Get medical care as soon as you can. Some injuries show up hours or days later. Early treatment protects you and creates a record that connects the crash to your symptoms.

Report the collision and save what you can. If you are physically able, take photos of the cars, the road, skid marks, debris, visible injuries, and anything else that helps explain what happened. Get witness names and contact information before people leave.

Notify your own insurer. Stick to the basic facts. Date, time, location, vehicles involved, and that you are receiving medical care is often enough at the start.

A claim is built piece by piece. Medical records, scene photos, witness information, and repair documents work together like bricks in a wall. If too many are missing, the insurer has more room to argue about fault, the seriousness of the injury, or what the case is really worth.

Avoid mistakes that can shrink the value of the claim

- Do not admit fault at the scene. A polite apology made in shock can later be treated like a statement of blame.

- Do not give a recorded statement to the other driver's insurance company before you understand your injuries. Adjusters often ask narrow questions early, before the full medical picture is clear.

- Do not minimize your symptoms. If you have headaches, dizziness, back pain, numbness, sleep problems, or trouble working, tell your doctor clearly and keep updating them.

This matters for another reason many injured people do not realize right away. If the other driver has only basic insurance, the insurer may act as if the policy limit defines the case. It does not. Your records still need to show the full harm you suffered, because that proof can matter in claims involving underinsured motorist coverage, additional liable parties, or assets beyond the basic policy.

Create a paper trail while you recover

Keep every medical record, bill, work excuse, prescription receipt, mileage log, and repair estimate. Save emails from your employer about missed time or changed duties. Start a simple journal and write down pain levels, sleep problems, activities you miss, and tasks you now need help with.

That journal gives context to the numbers on a bill. A hospital invoice shows treatment. A daily note about not being able to lift your child or finish a shift shows how the injury changed your life.

If you need legal guidance, Law Office of Bryan Fagan, PLLC handles Texas injury matters including car, truck, catastrophic injury, and wrongful death cases. A lawyer can help identify every possible source of recovery instead of stopping at the other driver's first insurance number.

Watch the filing deadline

Texas law generally gives injured people two years from the date of the accident to file most personal injury lawsuits. For example, if a crash happened on January 15, 2023, the filing deadline would generally be January 15, 2025 (Fact 6).

That deadline can arrive faster than people expect. While you are still treating and the insurance company says it is reviewing the claim, the clock keeps running. Missing it can end the case, even if your injuries are serious and even if the available insurance was never enough to cover the loss.

You Are Not Alone We Are Here to Help

A serious car wreck creates more than one problem at a time. You're trying to heal, manage bills, answer insurance questions, and make decisions that can affect your future for years. That is a lot for any family to carry.

The legal side is especially hard because it doesn't turn on one issue alone. The value of a case depends on the full scope of damages. Recovery may be reduced if fault is disputed. And the money available may involve more than the at-fault driver's basic insurance.

Why legal help changes the process

A lawyer's job isn't just to file paperwork. It is to gather records, develop proof of damages, challenge unfair fault arguments, identify all available insurance, and prepare the case as if it may need to go to court.

That matters in both settlement and litigation. Many cases do settle, but insurers often pay more attention when they know the injured person is ready to prove the case fully.

A fair settlement usually comes from preparation, not from trusting the first number on the table.

The two rules you cannot afford to miss

Verified Texas guidance puts two legal milestones at the center of any claim: the 51 percent bar and the two-year statute of limitations. If you are found too far at fault, you can lose the right to recover. If you miss the filing deadline, you can lose the claim completely (Fact 2).

That is why timing and evidence matter so much after a major collision. Waiting too long or handling the claim casually can damage a case that might otherwise have supported your recovery.

Focus on healing while your case is protected

You don't have to know every legal rule today. You don't have to answer every adjuster perfectly. And you don't have to figure out the full value of your case while you're still in pain.

You do need clear advice, careful documentation, and a plan that looks beyond the other driver's minimum insurance. Whether your case involves a routine collision, a life-changing injury, a commercial vehicle, or a fatal crash, recovery is possible and help is available.

If you need answers about your rights after a wreck, schedule a free consultation with Law Office of Bryan Fagan, PLLC. Our team helps Texans evaluate car accident, truck accident, catastrophic injury, and wrongful death claims, explain what compensation may be available, and take practical next steps toward financial recovery.