A serious accident can change your life in seconds, but you don't have to face it alone.

If you're reading this, you may be dealing with pain, car repairs, missed work, medical appointments, and nonstop calls from insurance adjusters. You may also be wondering whether the offer on the table is fair, whether you waited too long to get help, or whether a Texas personal injury lawyer can raise the value of your case.

The answer is that good cases usually aren't built by luck. They're built through fast action, complete records, and smart timing. That's especially true if you're trying to figure out how to maximize personal injury settlement texas after a crash in Houston, Dallas, Austin, San Antonio, or anywhere else in the state.

A stronger settlement usually comes from doing a few things well. Preserve evidence early. Get medical care without gaps. Prove not only what the injury cost you today, but what it may cost you later. Identify every possible source of insurance coverage. Don't let an adjuster push you into a cheap resolution before the full picture is known.

After a Houston freeway crash, for example, many people think the case is only about the police report and body shop estimate. It usually isn't. The claim may also involve future treatment, work restrictions, disputed fault, and questions about whether the at-fault driver has enough coverage. Those details often shape the final result more than people expect.

Your Path to Recovery After a Serious Texas Accident

The first days after a wreck can feel disorienting. One moment you're driving to work, picking up your kids, or heading home. The next, you're trying to remember what happened and whether the pain in your neck, back, shoulder, or head is going to get worse.

That stress is real. So is the pressure to “handle it quickly” and move on.

The problem is that quick decisions often help the insurance company more than the injured person. A settlement should reflect the full value of what happened to you, not just the bills sitting on your kitchen counter this week. If your injury affects your work, sleep, mobility, or future treatment, your claim needs to show that clearly.

What a strong claim usually looks like

A well-prepared injury claim has three moving parts:

- Liability proof: who caused the crash and why

- Damage proof: what the collision has cost you physically, financially, and personally

- Coverage analysis: which insurance policies and defendants may pay

If any one of those parts is weak, settlement value can drop. If all three are strong, your position in negotiations improves.

Practical rule: The best time to build a settlement case is before the insurance company decides your case is small.

A Houston car accident attorney or another Texas injury lawyer adds practical value. The work isn't just “filing a claim.” It's collecting records, preserving evidence, organizing treatment, spotting missing coverage, and presenting the case in a way that's hard to dismiss.

What actually moves settlement value

In practice, a higher-value claim usually comes from details that are easy to overlook at the start:

| Settlement factor | Why it matters |

|---|---|

| Clear fault evidence | It reduces room for blame-shifting |

| Consistent medical treatment | It helps connect the crash to the injury |

| Strong future-damage proof | It prevents the claim from being valued too early |

| Complete insurance search | It may uncover more than one recovery source |

| Careful communication | It avoids statements that weaken the case |

If you've lost a loved one, these same issues matter in a different but equally serious way. A wrongful death lawyer Texas families trust will look closely at liability, damages, and available coverage from the start. The same is true in severe collision cases involving surgery, spinal injuries, or life-changing impairments.

Protecting Your Claim From the Moment of Impact

The strongest claims usually start with disciplined evidence preservation. In Texas, guidance on maximizing compensation stresses a day-one workflow that includes immediate medical care, the police report, photographs of vehicles and injuries, road conditions, witness contacts, and a symptom-and-expense log, because strong claims document both economic and non-economic harms, as discussed in Texas injury claim evidence guidance.

After a crash, your first job is safety. Move only if it's safe to do so, call 911, and ask for medical help if anyone may be hurt. Then think like someone preserving evidence, not like someone trying to “tough it out.”

What to do at the scene

If you're physically able, gather facts before they disappear.

- Photograph the basics: Get wide shots and close-ups of all vehicles, license plates, skid marks, debris, lane positions, traffic signs, weather conditions, and visible injuries.

- Identify witnesses: Ask for names and contact information. Independent witnesses can matter when drivers tell different stories later.

- Ask how the crash will be documented: Find out whether law enforcement is preparing a report and how to request it.

- Watch your words: Be polite, but don't apologize or guess about fault.

A simple example. After a Houston freeway crash, one driver may tell the insurer that you changed lanes abruptly. A few phone photos showing impact points, road markings, and final vehicle positions may tell a very different story.

The scene changes fast. Tow trucks arrive, vehicles move, weather shifts, and witnesses leave. Your photos often become the only record of what the roadway looked like.

What to do in the next few days

A claim can weaken quickly if your records are thin or inconsistent. The days after the wreck matter almost as much as the scene itself.

- Get medical evaluation promptly. Even if the adrenaline is masking symptoms, early care helps connect the injury to the crash.

- Follow through with treatment. If you're told to see a specialist, physical therapist, or follow-up provider, go.

- Start a simple injury file. Keep discharge papers, prescriptions, bills, mileage, work notes, and receipts together.

- Track symptoms daily. Write down pain, headaches, sleep problems, mobility limits, and tasks you can't do.

- Limit insurance conversations. Give basic claim information, but don't treat the first adjuster call like a full interview.

What hurts a claim early

Some mistakes are common, and insurers know how to use them.

- Gaps in treatment: They may argue you weren't seriously hurt.

- Missing photos: They may minimize the force of impact.

- Informal statements: They may take a casual comment and treat it like a formal admission.

- Early settlement talks: They may push resolution before your diagnosis is clear.

This is one reason many injured people contact counsel early. A law firm such as Law Office of Bryan Fagan, PLLC can handle evidence collection, insurer communication, and record organization while you focus on treatment.

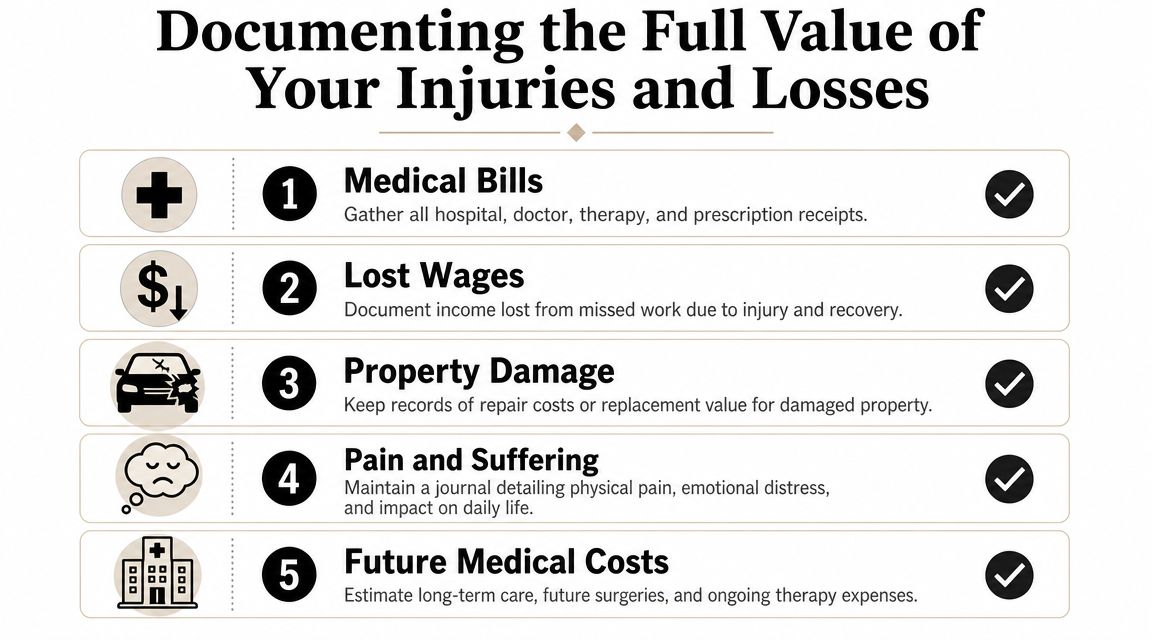

Documenting the Full Value of Your Injuries and Losses

A settlement should reflect more than the bills you've already paid. It should reflect the full harm the injury caused and the losses that are still unfolding.

That's where many claims get undervalued. People gather emergency room records and a few invoices, but they don't build proof for what comes next. If your injury affects your ability to work, sleep, lift, drive, care for family, or live without pain, that needs to be documented with the same care as a hospital receipt.

The losses most people think about first

Start with the straightforward categories. These are often easier to collect and organize.

| Type of loss | Examples of proof |

|---|---|

| Medical expenses | Bills, itemized statements, prescriptions, therapy records |

| Lost income | Pay records, employer letters, missed time records |

| Property damage | Repair estimates, photos, total-loss paperwork |

| Out-of-pocket costs | Mileage, medical devices, over-the-counter supplies |

Those records matter. But they rarely tell the whole story by themselves.

The losses that often make the biggest difference

Future damages are where many claims are won or lost. Texas injury guidance notes that many victims don't realize they should build proof for future losses immediately through specialist opinions, work restrictions, life-care planning, and evidence showing how the injury changed daily function. It also warns that delays in treatment or gaps in records can weaken causation and can separate a modest recovery from fuller compensation in serious cases, as explained in Texas guidance on proving future injury losses.

If your doctor believes you may need future care, don't wait for the adjuster to ask questions. Get the issue documented.

Consider gathering:

- Specialist opinions: Orthopedic, neurological, pain-management, or other treating-provider opinions about future needs

- Work restrictions: Notes showing lifting limits, driving limits, or reduced job capacity

- Daily-function evidence: A journal describing pain levels, sleep problems, missed family activities, and physical limitations

- Family observations: Statements from people who see how your routine changed after the crash

Key takeaway: A stack of bills shows what happened to your wallet. A well-kept record shows what happened to your life.

Building a record that insurers can't easily dismiss

Good documentation is organized, dated, and consistent. That sounds simple, but it takes discipline over time.

A practical system looks like this:

- Create one timeline: Put the crash, every appointment, every missed-work date, and every major symptom change in date order.

- Keep originals where possible: Save PDFs, discharge instructions, scans, and photos in one folder.

- Match symptoms to care: If your back pain worsened before you saw a specialist, note that in your journal and keep the appointment record beside it.

- Track future recommendations: If a provider discusses surgery, injections, therapy, or long-term restrictions, save that note immediately.

If gathering complete records becomes difficult, even smart clients can fall behind. In that situation, resources like Matil insights on records retrieval can help you understand how medical-record collection works and why delays in retrieval can affect case preparation.

A real-world example

Suppose you're rear-ended in Dallas and think the case is simple. At first, it looks like a soft-tissue claim. A month later, you're still missing sleep, physical therapy isn't resolving the issue, and your job becomes harder because sitting for long periods causes pain.

If your file only contains the first urgent-care note, the insurer may value the case like a short-term inconvenience. If your file also includes follow-up treatment, work restrictions, your symptom journal, and a treating doctor's view of future care, the claim tells a very different story.

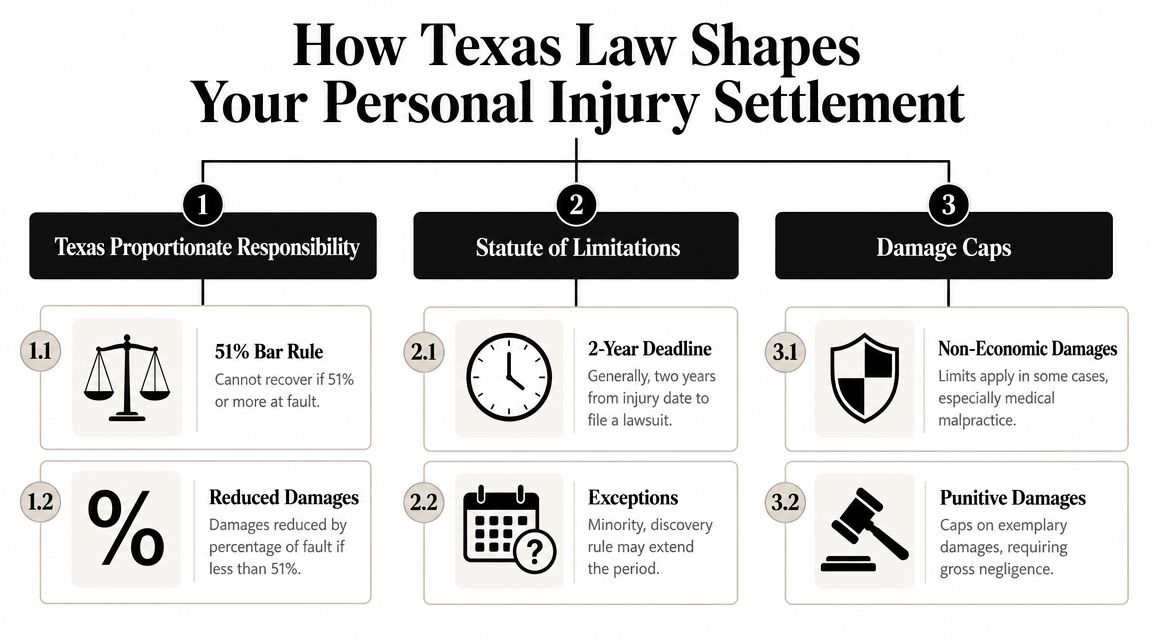

How Texas Law Shapes Your Personal Injury Settlement

Texas law affects settlement value in direct ways. The two rules that matter most in many cases are comparative fault and the filing deadline. If you don't understand those rules, it's easier for an insurer to frame your claim on terms that favor them.

Here is the legal side in plain English.

Texas comparative fault can reduce or block recovery

Texas uses a modified comparative fault rule. If you're found 51% or more at fault, you can't recover damages. If you're 50% or less at fault, your recovery is reduced by your share of fault. One example often used in Texas settlement discussions shows that if a jury awards $500,000 and finds you 30% at fault, your recovery becomes $350,000, as described in Texas comparative fault guidance.

That's why fault arguments matter so much, even in cases that look obvious at first.

A few common examples:

- Intersection crash: The other driver ran a light, but the insurer claims you were speeding.

- Truck collision: The trucking company blames your lane position or following distance.

- Multi-vehicle wreck: Each insurer tries to push a larger share of blame onto someone else.

If the defense can increase your percentage of fault, they can reduce the value of the claim. In some cases, they can eliminate recovery altogether.

For a closer look at issues that often affect claim value, review factors that affect an injury settlement in Texas.

How long do you have to file a claim in Texas

In most Texas personal injury cases, the general rule is that you have two years from the date of injury to file suit. Some situations can involve exceptions or special notice requirements, but waiting is still risky because evidence gets harder to secure, witnesses become harder to reach, and records may not be preserved as cleanly.

That deadline matters even if settlement talks are ongoing. Negotiations don't automatically protect your right to sue.

Don't confuse an open insurance claim with a protected legal claim. They are not the same thing.

Here's a helpful video that explains part of the process in a more visual way.

Why these rules change strategy

Texas law rewards preparation. If fault is likely to be disputed, the case should be built with that fight in mind from the start. If the filing deadline is approaching, your lawyer may need to move quickly to protect the claim even while treatment is still ongoing.

That's one reason injured people often reach out earlier than they expected. A Houston car accident attorney or truck crash lawyer Houston clients call after a serious wreck isn't just arguing about money. They're protecting timing, preserving proof, and positioning the case under Texas law before the insurer defines it for you.

Navigating Negotiations and Dealing with Insurance Adjusters

Insurance adjusters are trained to evaluate exposure, control claim costs, and close files. Some are professional and reasonable. Some push hard for a fast, cheap result. Either way, you should assume that every conversation has a purpose.

The most common mistake injured people make is treating the adjuster like a neutral problem-solver. The adjuster's job is to protect the company's interests.

What adjusters often do

Many negotiation tactics are predictable.

- They ask for a recorded statement early: This can lock you into details before you know the full extent of your injuries.

- They focus on gaps or inconsistencies: A missed appointment or delayed complaint becomes an argument that the injury wasn't serious.

- They make an early offer: The number may sound helpful when bills are piling up, but early offers often come before future care is clear.

- They narrow the claim: They may discuss the ER visit and property damage while ignoring long-term pain, work limits, or future treatment.

Texas-focused settlement guidance also emphasizes that the ceiling on recovery is often shaped not just by injury severity, but by policy limits and proof of every available coverage source. A practical strategy is to request policy declarations early, identify all liable parties, and document future medical needs before the first offer arrives, as explained in Texas settlement guidance on policy limits and coverage sources.

What works better than reacting

A strong negotiation position usually comes from preparation, not pressure. Before serious settlement talks begin, your side should know what evidence supports fault, what records prove damages, and what coverage may apply.

That often includes a demand package with:

| Demand package component | Why it matters |

|---|---|

| Liability summary | Shows why the other party is responsible |

| Medical chronology | Connects treatment to the crash |

| Wage-loss support | Proves income disruption |

| Future-damage support | Prevents undervaluation of ongoing needs |

| Settlement demand | Anchors negotiation with documented reasoning |

If you've never seen one, this sample personal injury demand letter shows the kind of structure lawyers use when presenting a case to an insurer.

A demand letter works best when it tells a complete story, not when it simply attaches a pile of bills.

Don't overlook UM and UIM coverage

One of the most overlooked ways to maximize a settlement is to identify every possible policy. If the at-fault driver is uninsured or underinsured, your own policy may matter. In other cases, there may be additional defendants, vehicle owners, commercial policies, or layered coverage questions.

This issue comes up often in serious crash cases, especially where a truck crash lawyer Houston families consult is dealing with a commercial vehicle, multiple companies, or disputed responsibility.

Here are situations where coverage analysis becomes especially important:

- Uninsured driver: Your UM coverage may be a critical source of recovery.

- Underinsured driver: The at-fault policy may not cover the full loss.

- Employer-related driving: A business policy may be involved.

- Multiple vehicles or defendants: More than one policy may apply.

What not to do during negotiations

Some practical limits are worth keeping in mind.

Don't guess about your prognosis. Don't tell the adjuster you're “fine” if you're still treating. Don't assume the first policy disclosed is the only one that matters. And don't settle a case just because the insurer says it's the best they can do before your records are complete.

Negotiation is where preparation turns into an advantage. If the case is documented well, the adjuster has fewer openings to devalue it.

When to Hire a Texas Personal Injury Attorney

Some injury claims can be resolved without a lawyer. Many should not be.

If your injuries are significant, fault is disputed, multiple vehicles are involved, or the insurance picture is messy, legal help often changes the course of the case. The more serious the losses, the more expensive it becomes to make a mistake early.

Signs you shouldn't handle it alone

These situations usually call for prompt legal review:

- Serious injury: Surgery, long-term treatment, chronic pain, or permanent limitations raise future-damage issues that need careful proof.

- Disputed fault: If the other side is blaming you, the case can turn on evidence and legal framing.

- Wrongful death: A wrongful death lawyer Texas families trust can help protect evidence, identify liable parties, and pursue the full range of losses allowed by law.

- Commercial or truck crash cases: These often involve layered insurance, corporate defendants, and rapid-response defense teams.

- Denied or delayed claim: If the adjuster is stalling, minimizing your injuries, or pushing a low offer, the process has already become adversarial.

For a fuller discussion of timing, see when to hire a personal injury lawyer in Texas.

What an attorney actually does

A lawyer's value isn't limited to filing paperwork. In a serious case, counsel may help:

- preserve evidence before it disappears

- coordinate records and billing support

- identify additional insurance coverage

- organize proof of future damages

- prepare a settlement demand

- file suit before the deadline if needed

- negotiate from a position backed by evidence

That work matters whether your case involves a rear-end collision, a commercial truck wreck, a catastrophic injury, or the loss of a family member.

What about legal fees

Many people wait too long to get help because they assume they can't afford it. In personal injury practice, that concern is common and understandable.

Most firms in this space, including Texas plaintiff firms, handle cases on a contingency-fee basis. That means there usually isn't an upfront attorney fee, and the lawyer is paid from the recovery if the case succeeds. The fee arrangement should always be explained clearly before representation begins, and you should feel comfortable asking questions about costs, expenses, and how disbursement works.

The right time to ask whether you need a lawyer is usually sooner than you think. Early action protects evidence. It also gives you a clearer picture of whether your claim is being valued fairly.

If you were hurt in a crash or lost a loved one in Texas, legal help is available. The Law Office of Bryan Fagan, PLLC offers free consultations for injury and wrongful death cases involving car accidents, truck wrecks, catastrophic injuries, and uninsured or underinsured drivers. You can speak with a Texas personal injury lawyer about your options, your deadlines, and the steps that may help protect the full value of your claim. Recovery is possible, and you don't have to sort through this alone.