A serious accident can change your life in seconds, but you don't have to face it alone.

You may be sitting in an ER parking lot, back home on the couch with a sore neck, or staring at discharge papers and wondering how any of this gets paid. If you don't have health insurance, the fear is immediate and practical. Can I get treatment without insurance after a Texas accident? Yes, you can. The harder question is how to keep treatment going once the first visit is over.

That's where a clear plan matters. In Texas, accident cases often involve overlapping insurance options, provider billing issues, and legal deadlines. If you know what to do early, you can protect both your health and your injury claim.

Your Guide to Medical Care After a Texas Accident

If you were hurt in a crash and don't have health insurance, start with this: don't let fear of the bill stop you from getting care. Texas accident victims often have more than one possible path to payment, even when they have no private health coverage. The problem is that a clear roadmap is often not provided when it's needed most.

A common example is a Houston driver who gets rear-ended on the freeway, goes home thinking the pain will pass, then wakes up the next morning barely able to turn their head. They know they need help, but they also know they don't have insurance through work and can't pay a specialist upfront. That's when confusion turns into delay, and delay often creates bigger medical and legal problems.

What this process usually looks like

The practical path usually involves a few moving parts working together:

- Emergency care first: Get checked right away if you may have a serious injury.

- Crash documentation: Police reports, photos, and witness names matter more than people realize.

- Auto coverage review: Your own policy may include benefits that help before a settlement arrives.

- Ongoing treatment planning: Follow-up care may require provider coordination, lien-based treatment, or attorney-arranged help.

Practical rule: The first goal is treatment. The second goal is creating a clean paper trail that ties your injuries to the crash.

If you want a broader look at common injuries and how treatment connects to an injury claim, this guide on motor vehicle accident injuries and treatment is a helpful companion resource.

Your Immediate Right to Emergency Medical Care

Your health comes first. If you think you may have a serious injury, go to the emergency room or seek urgent medical attention right away. People often hesitate because they don't have insurance, but waiting can make both the injury and the claim harder to handle.

Hospitals that provide emergency care must stabilize patients who need emergency treatment, regardless of insurance status or ability to pay. That means the door isn't closed to you just because you're uninsured. For many people, the ER is the first step, not the full solution.

Why the first medical visit matters so much

The first visit does two jobs at once. It gets you evaluated, and it creates medical records that connect the crash to your symptoms. That connection matters because insurance companies look for gaps. If you wait, they often argue the injuries were minor or unrelated.

Texas-focused claims guidance also stresses the same sequence after a crash: call police so the collision is officially recorded, gather photos and witness details, seek medical care right away, and notify your insurer. Those early records become the core proof for a later claim, and delaying treatment can weaken causation arguments, as explained in this Texas uninsured driver claims guidance.

What to do the same day if possible

Try to handle these tasks as soon as you safely can:

- Call law enforcement: A police report can anchor the timeline.

- Take scene photos: Vehicle damage, road position, visible injuries, and debris all help.

- Get names and contact details: Witnesses can become important if fault is disputed.

- Tell the doctor what hurts: Don't minimize symptoms just because adrenaline is high.

- Follow discharge instructions: If the ER tells you to see an orthopedist, neurologist, or physical therapist, take that seriously.

Early treatment isn't only about proving a case. It's how hidden injuries get found before they become harder to treat.

What doesn't work well

A lot of people make understandable mistakes in the first few days:

- Waiting to “see if it goes away”: Soft tissue injuries, concussions, and back injuries often worsen later.

- Making side deals with the other driver: Informal cash offers can create big problems if symptoms grow.

- Downplaying symptoms in the chart: Medical records are built from what you report.

If you're asking whether you can get treatment without insurance after a Texas accident, the answer starts here. Yes, and you should.

How Medical Bills Are Paid After a Texas Accident

Once emergency care is underway, the next question is usually blunt: who pays for this?

Texas is a fault state, which means the at-fault driver's liability coverage is ultimately responsible for accident-related losses up to available policy limits. Texas law also requires auto insurers to offer Personal Injury Protection, and the legal minimum PIP limit is $2,500 unless the policyholder declines it in writing. Common Texas minimum liability limits are $30,000 per injured person, $60,000 per crash, and $25,000 for property damage, as discussed in this Texas car accident treatment overview.

The catch is timing. Liability claims usually don't pay medical bills as treatment happens. They're often resolved later. So the main task is building a bridge between the date of the crash and the date the claim resolves.

Payment options side by side

| Payment Source | Who It Covers | How It Works | Key Benefit |

|---|---|---|---|

| PIP | Usually the named insured and others covered by the policy | Pays certain accident-related costs through your own auto policy, regardless of fault | Money may be available early |

| MedPay | People covered under the auto policy, depending on policy terms | Helps pay medical expenses under your own policy | Useful for immediate bills |

| At-fault driver liability coverage | The injured person with a valid claim | Paid through a claim against the driver who caused the crash | Main recovery source in many cases |

| UM/UIM coverage | Covered people under the policy when the other driver lacks enough coverage | Your own policy can step in if the other driver is uninsured or underinsured | Important fallback when liability coverage is missing or too low |

What each option does well, and what it doesn't

PIP is one of the most useful tools for uninsured crash victims because it can apply regardless of fault. If it's on your policy, it may help with early medical bills while the broader claim is still developing.

MedPay can also help with medical expenses, though policy language matters. Many drivers don't realize they bought it, or they confuse it with health insurance. It isn't the same thing, but it can still be valuable.

Liability insurance is often where the largest recovery comes from. But it usually doesn't solve the immediate cash-flow problem because providers want payment before a settlement check exists.

Key point: The at-fault driver's insurer may be responsible in the long run, but your treatment plan often depends on what can be accessed now.

If you're trying to understand provider invoices while treatment is ongoing, a plain-language balance billing guide can help you make sense of what medical offices and insurers are charging and why.

A practical way to think about it

After a Dallas intersection crash, for example, a person without health insurance may need to stack options. They might use PIP first, apply any available MedPay, continue treatment through a lien-based arrangement, and pursue the liability claim separately. That's often what works in real cases. Waiting for the other driver's insurer to “take care of it” usually doesn't.

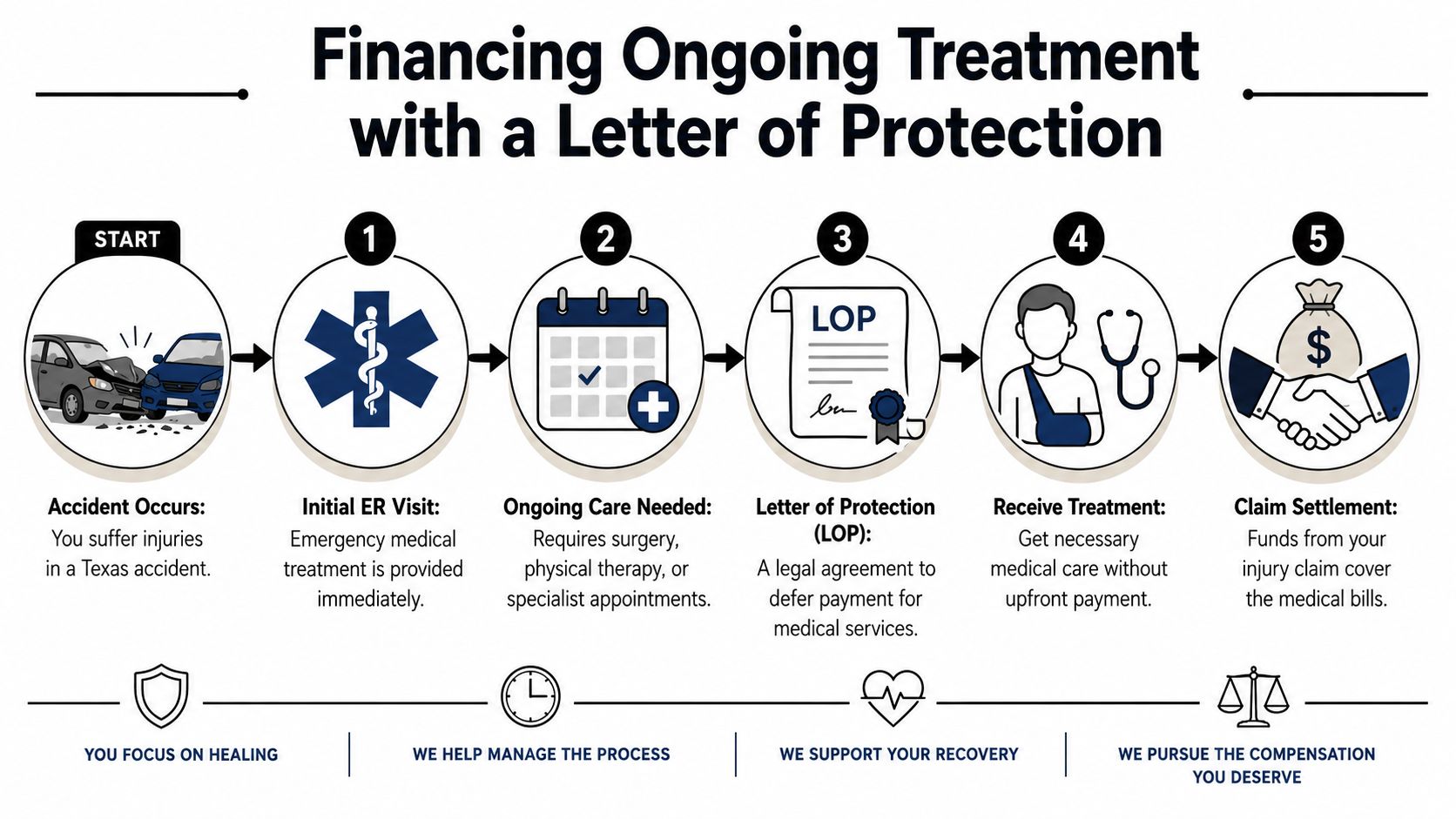

Financing Ongoing Treatment with a Letter of Protection

The hardest part for many uninsured accident victims isn't the ambulance ride or the first ER bill. It's the weeks that follow. That's when the doctor recommends imaging, pain management, orthopedic follow-up, or physical therapy, and the front desk asks for payment before the appointment is confirmed.

That gap is where a Letter of Protection, often called an LOP, can make a real difference.

How an LOP works in real life

An LOP is a document sent by your attorney to a medical provider. It says the provider will be paid from a future settlement or court recovery if the case succeeds. In practical terms, it lets some patients receive ongoing care without paying everything upfront.

This is why the main question for many injured people isn't whether they can be seen once. It's how they keep getting treated after the ER when they have no cash and no health coverage. Texas-focused guidance notes that a letter of protection often bridges that gap for follow-up care, imaging, and physical therapy that would otherwise require upfront payment, as explained in this discussion of post-accident treatment options.

A common Texas scenario

After a Houston freeway crash, a driver may leave the ER with muscle relaxers and instructions to follow up if pain continues. A week later, they still can't sleep, their lower back hurts, and their primary care doctor can't see them quickly. A physical therapy clinic wants payment at the first visit. An MRI center asks for upfront money. That's when people often feel stuck.

An attorney may be able to coordinate care with providers willing to work under an LOP. That can include:

- Imaging providers: MRI or other diagnostic follow-up when symptoms continue

- Specialists: Orthopedic, spine, or pain-focused doctors, depending on the injury

- Therapy clinics: Physical therapy or rehabilitation visits that need to happen consistently

Treatment tends to work best when there's a plan for continuity, not just a single emergency visit.

Trade-offs you should understand

An LOP is useful, but it isn't magic. You still need a viable claim. Providers may choose whether to accept this arrangement. Bills are still real, and they're generally resolved from the case proceeds if the claim succeeds. That means you should treat an LOP as a tool for necessary care, not a blank check for unlimited treatment.

It also works best when your legal team moves quickly, gathers records, and communicates clearly with providers. If you've heard about a lawyer letter of representation, that document often helps open the claim and start the process of coordinating treatment and protecting your case.

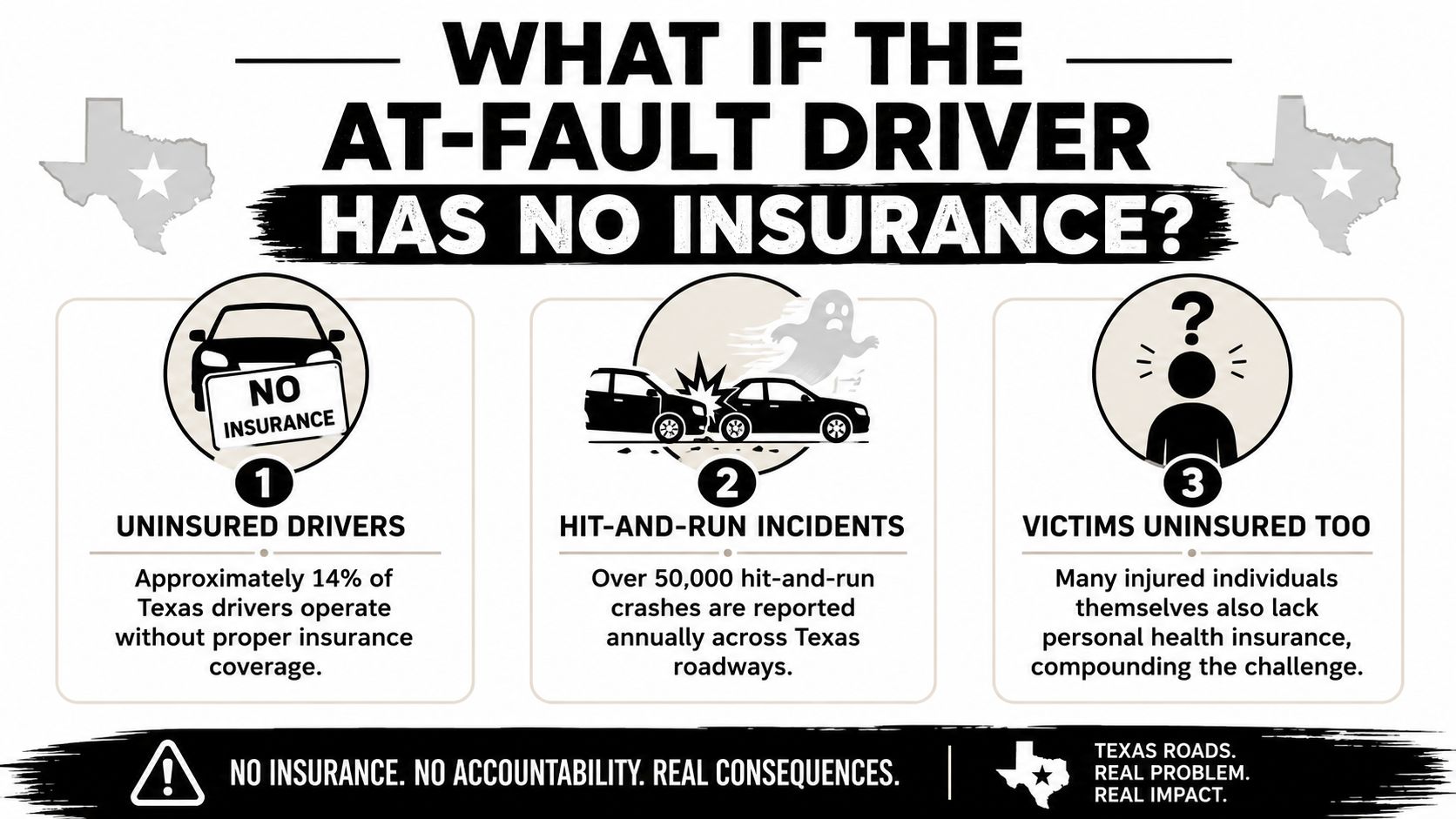

What If the At-Fault Driver Has No Insurance?

You leave the ER with discharge papers, a prescription, and instructions to get follow-up care. Then you find out the driver who hit you may not have insurance, or only carries a small policy that will not come close to covering what happened. That is the moment many people assume they are out of options.

You are not. The path just changes.

The first place to look is your own auto policy for UM/UIM coverage. That means uninsured or underinsured motorist coverage. If that coverage is on your policy, it may pay for damages the at-fault driver should have paid. In many cases, it becomes the main source of recovery after a serious crash.

The Insurance Information Institute reports that uninsured driving remains a real problem nationwide, according to its uninsured motorist facts and statistics. In practice, I tell clients not to assume the other driver has enough coverage until we verify it.

The coverage people forget to check

UM/UIM can matter in three common situations:

- The other driver had no insurance

- The other driver had insurance, but the limits are too low

- The crash was a hit-and-run and the driver cannot be identified

People often expect their own insurer to handle these claims without much resistance. Sometimes that happens. Sometimes your insurer disputes fault, questions treatment, or argues your injuries are less serious than your records show. A UM/UIM claim still needs proof. That includes the crash facts, your medical records, and a clear explanation of how the injuries affected your life.

Other possible paths

If you do not have UM/UIM, the next step is a full policy search. That includes PIP or MedPay on your own policy, coverage on the vehicle you were riding in, and sometimes a household policy that may apply depending on the facts. A careful review often turns up options people did not know they had.

Suing the uninsured driver is sometimes legally possible. Collecting is a separate question. If the driver has no meaningful assets or income, a lawsuit may produce a judgment on paper but very little actual payment. TexasLawHelp explains the practical limits of collecting from someone who cannot pay in its discussion of collecting a judgment in Texas.

That is why early coverage review matters so much. It affects not just the legal claim, but how treatment gets coordinated while the case is pending. If you want a clearer explanation of how these claims work, read more about uninsured motorist coverage in Texas.

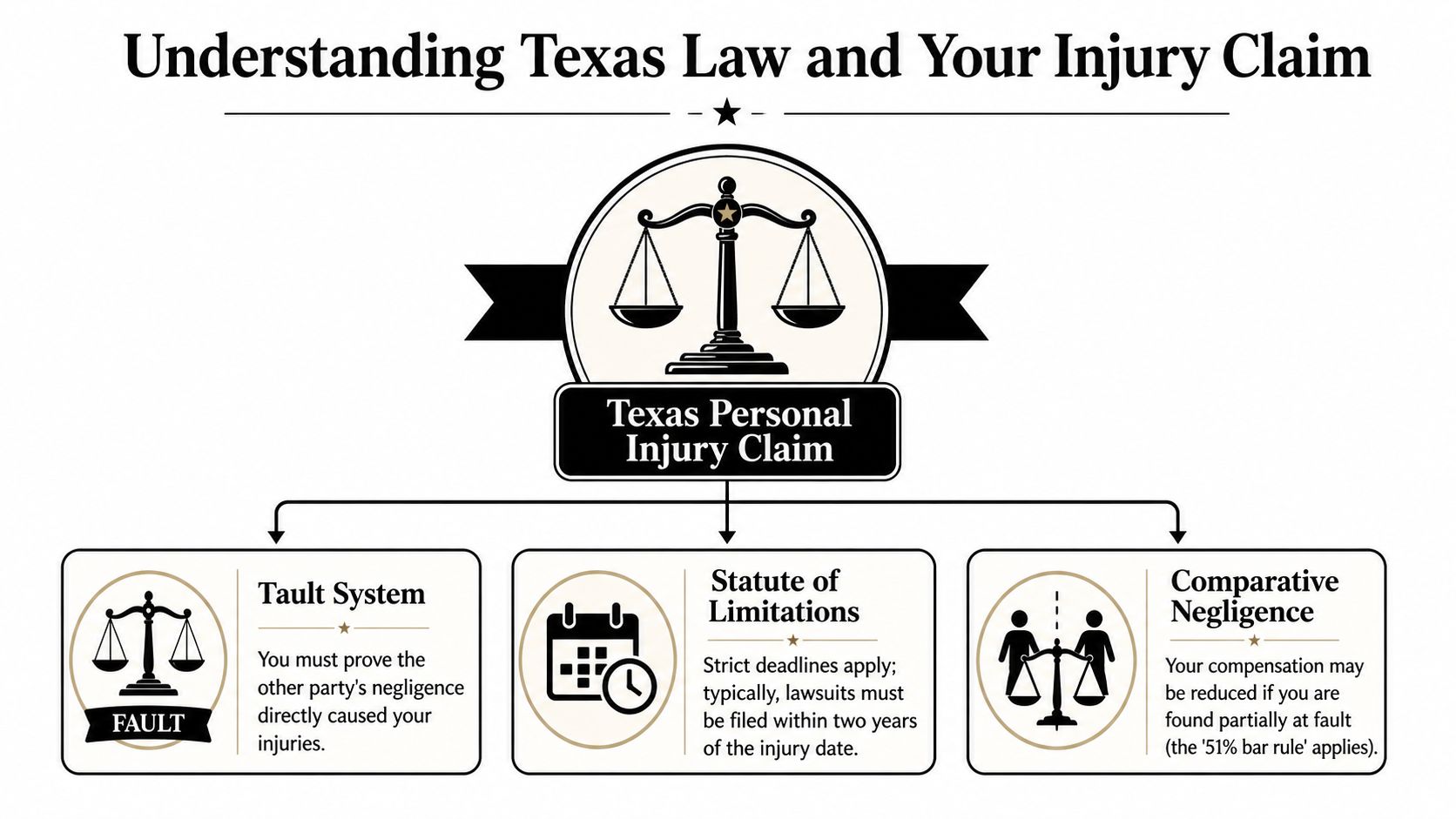

Understanding Texas Law and Your Injury Claim

A lot of uninsured crash victims make the same mistake. They focus on how to get the next doctor visit paid for, but they do not realize that the legal rules in Texas can affect whether those bills are ever reimbursed and whether treatment arranged on a case basis stays financially workable.

Fault and negligence

Texas uses a fault-based system for injury claims arising from car and truck wrecks. To recover money, you usually need proof that another driver or company acted carelessly and that the carelessness caused your injuries.

That sounds simple until an insurance adjuster starts picking the case apart.

After a serious crash, proof often includes the police report, witness names, photos of the scene, vehicle damage, medical records, and sometimes black box data, company records, or surveillance footage. In a truck case, those extra records can matter a great deal. In a regular car wreck, early photos and prompt medical documentation often carry much of the weight.

Comparative responsibility

Texas also reduces compensation if the injured person shares some of the blame. If you are found more responsible than the other side, recovery may be barred. If you are partly at fault but still legally allowed to recover, your compensation is reduced by your percentage of responsibility. The Texas Civil Practice and Remedies Code explains this rule in Chapter 33 on proportionate responsibility.

That rule affects real money. If an insurer claims you were speeding, turned without enough warning, or were looking at your phone, it is not just an argument about what happened. It is an argument about how much of your medical care, lost income, and pain the insurer will agree to pay.

This is one reason treatment records matter beyond your health. Consistent care creates a timeline. It helps connect the crash to the injury, shows how symptoms developed, and makes it harder for an insurer to argue that you were not really hurt or that something else caused the problem. Related discussions from Midwest Pain & Wellness also show how medical documentation and legal claims often rise or fall together.

The statute of limitations

Texas injury claims also have a filing deadline. In many cases, you have two years from the date of the wreck to file suit. Waiting creates practical problems long before that deadline arrives. Witnesses stop answering calls. Video is erased. Vehicles get repaired or sold. Providers may be slower to produce records once time has passed.

Families dealing with a fatal crash face the same pressure, often while still in shock. Early legal work is often about preserving evidence before it disappears.

Where legal help fits in

A personal injury lawyer does more than argue with an insurance company. Good legal help ties the medical and financial sides of the case together. That can include gathering proof, protecting you from recorded statement traps, identifying every available policy, and helping arrange treatment that can continue while the claim is pending.

That matters most when money is tight. The legal claim is often what supports the treatment plan, especially for someone relying on provider agreements, delayed billing, or attorney-arranged care. If the evidence is weak or the deadlines are missed, the medical side of the case gets harder too.

The goal is not just to file paperwork. The goal is to build a claim strong enough to support your recovery from the first appointment through settlement or trial.

You Don't Have to Face This Alone Take Control of Your Recovery

Being hurt in a crash without health insurance is frightening, but it isn't hopeless. There is usually a path forward if you act early, document carefully, and use the right combination of medical and legal tools. The people who struggle most are often the ones who wait too long, trust the insurance company to explain their options, or stop treatment because they assume they have no way to continue.

It also helps to learn how injury care and legal claims overlap in other settings. For example, this article from Midwest Pain & Wellness on workers' comp and personal injury claims gives useful context on how medical treatment, documentation, and claim strategy often connect when someone is trying to recover physically and financially.

If your injuries are affecting your work, your family, or your daily life, get answers sooner rather than later. Recovery is possible, and the right guidance can make the process much less overwhelming.

If you need help after a crash, Law Office of Bryan Fagan, PLLC can review your situation, explain your options, and help you pursue care and compensation after a car, truck, catastrophic injury, or wrongful death case in Texas. A free consultation can give you a clearer next step when everything feels uncertain.