A serious accident can change your life in seconds — but you don’t have to face it alone. As you try to pick up the pieces, the at-fault party's insurance company will likely offer you a settlement and ask you to sign a document called a "release of liability."

This isn't just a piece of paper. It's a legally binding contract where you agree to accept a sum of money in exchange for giving up all future rights to sue over that accident. Signing it is a final, irreversible step, and you need to understand exactly what that means for you and your family.

Understanding a Release of Liability in Texas

After something as traumatic as a Houston freeway crash or a life-altering injury, a quick check from an insurance company can feel like a lifeline. Adjusters often present a release of liability as a simple formality—just something you need to sign to close your claim and get your money.

But let's be clear: this document is one of the most powerful tools an insurer has to protect its own financial interests, not yours. It is designed to end their responsibility to you for the lowest possible cost.

Think of it like this: signing that release is like permanently closing and locking a door. Once it’s shut, you can almost never reopen it, no matter what new problems or expenses pop up down the road.

The Finality of a Signed Release

Imagine you're in a wreck on I-10 in San Antonio. At first, your injuries seem minor—some bruises, maybe a little whiplash. The other driver’s insurance company swoops in with an offer of $5,000 to cover your initial doctor's visit and "for your trouble." You're hurting, overwhelmed, and eager to put the whole thing behind you, so you sign their release form.

A month later, the real trouble starts. You develop severe back pain, and a specialist diagnoses a herniated disc. Now you're facing surgery, months of physical therapy, and a mountain of medical debt, all while being unable to work.

Because you signed that release, you have legally forfeited your right to seek another dime from the at-fault driver or their insurer. You're left to handle the devastating financial and physical fallout all on your own.

This scenario is tragically common. Signing a release without fully understanding your long-term medical needs and financial losses can leave you with a fraction of the compensation you truly deserve.

Why Insurers Push for a Quick Signature

Insurance adjusters are skilled negotiators whose job is to resolve claims for the lowest possible amount. They know that injuries—especially after a serious car or truck crash—can take weeks or months to fully reveal themselves. The true cost of an accident is almost always higher than it first appears.

By pressuring you to sign a release quickly, they aim to lock in a low settlement before you realize the full extent of your damages.

And it works. With nearly 400,000 personal injury claims filed in the U.S. each year and over 96% settling out of court, these releases are the primary tool insurers use to limit their payouts. You can find more details about these statistics and how they impact victims in this comprehensive legal industry report.

Before you even think about signing a document from an insurance company, you need to understand your rights under Texas law and the permanent consequences of that signature.

Decoding Your Release of Liability Form

The release form an insurance company sends you is filled with dense legal language designed to be confusing. It’s written by their lawyers to protect them, not you. Below is a simple breakdown of the key terms you’ll likely find and what they actually mean for your case.

| Legal Term | Plain English Meaning | How It Affects Your Claim |

|---|---|---|

| Release and Discharge | This means you are giving up your right to sue or make any future claims. | You completely and forever forfeit your ability to seek more money for this incident. |

| Indemnify and Hold Harmless | You agree to protect the at-fault party if someone else (like a health insurer) tries to sue them over your accident. | You could be on the hook for their legal bills if another party tries to collect from them. |

| Known and Unknown Injuries | This covers all injuries, even those you don't know about yet. | You can't ask for more money later if a new injury appears or a known one gets worse. |

| Consideration | This refers to the settlement money you receive in exchange for signing the release. | This is the one-time payment you get. Once accepted, you can't ask for more. |

| Full and Final Settlement | This language emphasizes that the agreement is permanent and cannot be changed. | The door is closed. The amount is set in stone, no matter what happens in the future. |

Don't let these terms intimidate you. They all boil down to one thing: signing this document ends your claim for good. If you're unsure about any part of a release, it’s a major red flag that you need to stop and get professional legal advice before you sign away your rights.

Recognizing a Liability Release in Different Scenarios

When you've been in a serious accident, you might think a "release of liability" form only shows up when you're ready to accept a final settlement. But that's not always the case. Insurance companies are notorious for sliding these critical documents in front of you at various stages, often when you’re most vulnerable and least expect it. Knowing when and where these forms can pop up is your first line of defense.

A classic example? The check for your car repairs. You're anxious to get your vehicle out of the shop and back on the road, so you sign the attached form without a second thought. This is a common and costly trap. Tucked away in the fine print is often broad, sweeping language that doesn't just settle your property damage—it releases the insurer from all other claims, including every penny related to your personal injuries.

Releases Beyond the Initial Crash Report

A release of liability isn't just for a standard fender-bender. These documents are a routine part of nearly every type of claim a Houston car accident attorney handles, including some of the most serious cases imaginable:

- Commercial Truck Crashes: After a devastating wreck with an 18-wheeler on I-45, the trucking company’s insurer will be incredibly aggressive. They want a quick signature on a release to shut down their massive financial exposure before the true costs of a catastrophic injury are known. A skilled truck crash lawyer in Houston can protect you from this pressure.

- Wrongful Death Claims: Grieving families are particularly susceptible to this tactic. An insurer might offer what seems like a substantial amount of money right away, but it comes with a release that permanently closes the door on recovering the full, fair compensation a family needs after losing a loved one.

- Uninsured/Underinsured Motorist (UM/UIM) Claims: You might think you're safe when dealing with your own insurance company for a UM/UIM claim, but the process is the same. To finalize your settlement and get the money you're owed under your policy, you will have to sign their release.

For example, let's say you were rear-ended by someone with the bare minimum insurance coverage, which doesn't even begin to cover your medical bills. Your own Underinsured Motorist (UIM) policy is there to bridge that gap. Once your insurer agrees to pay out on that policy, they will require you to sign a release, officially ending their obligation to you for that accident.

The Danger in a Property Damage Release

The sneakiest scenario, and the one that trips up the most people, almost always involves the property damage claim for your vehicle. An adjuster will call with good news: "We've approved the payment for your car repairs. I'm just sending over a quick form for you to sign so we can cut the check."

It sounds simple and harmless, but this is a critical moment. That "quick form" is almost certainly a release of liability. If you see phrases like "in full and final settlement of any and all claims" or language that releases them from liability for "known and unknown injuries," stop. Signing that document could mean you've just accidentally signed away your right to any compensation for your medical treatment, lost income, and physical pain.

You have to treat every single document you get from an insurance company with extreme caution. Before you put a pen to anything—even if it looks like a simple authorization for car repairs—it is absolutely essential to have an experienced attorney review it first.

Hidden Clauses Insurers Hope You Overlook

Insurance adjusters are professional negotiators. Their goal is to protect their company’s bottom line, which they do by settling your claim for as little money as possible. The release of liability form is their most powerful weapon, often loaded with confusing legal jargon and hidden traps designed to strip you of your rights.

You have to remember that the first settlement offer is almost never the best one. Think of it as the opening bid in a negotiation. Adjusters are banking on you being too stressed and overwhelmed to push back. They hope you'll just sign on the dotted line, overlooking the fine print that permanently slams the door on the full compensation you and your family actually deserve.

Watch for These Red Flags

When an adjuster sends over a release, they aren’t just trying to settle your current medical bills. They are trying to wipe their hands clean of all future responsibility. Before you even think about signing, you need to scan that document for specific, toxic clauses that can have life-altering consequences down the road.

Here are a few of the most dangerous terms insurers love to sneak in:

- "All Known and Unknown Claims": This is the big one. This phrase means you’re signing away your right to seek money for any injury or medical condition that hasn't shown up yet. If that "minor" back pain from a truck crash turns out to require major surgery a year later, you will have absolutely no way to get it covered.

- Confidentiality or Non-Disclosure Clauses: These terms legally gag you, preventing you from ever discussing the accident or your settlement. It might seem harmless, but it can stop you from sharing your story or warning others about a dangerously negligent driver or company.

- Subrogation Waivers: This little clause can be a financial nightmare. It could force you to use your settlement money to pay back your own health insurance company for the medical bills they already covered. An experienced attorney can often negotiate these liens down, but signing blindly can leave you with pocket change after everyone else gets paid.

A Family's Story of Pressure and Loss

Imagine a family in Texas reeling from the sudden loss of their father in a catastrophic collision caused by a reckless driver. While they're still in shock and trying to plan a funeral, the at-fault driver's insurance company swoops in with a settlement offer and a release form.

The adjuster applies the pressure, hinting that this is the best deal they’ll get and that a lawsuit would only drag out their pain. The family, emotionally drained and now facing unexpected final expenses, feels completely trapped.

They are being pushed to sign a document before they can possibly grasp the full financial devastation of losing their primary provider—all the future lost income, the loss of companionship, and the profound emotional toll on their family. This is exactly what the insurance company wants.

A wrongful death lawyer in Texas would have told them to stop all communication with the insurer immediately. A professional needs to step in to calculate the true, long-term value of their claim and protect the family's future. Signing that release would have been an irreversible mistake, costing them the financial security their loved one would have wanted for them.

How Signing a Release Limits Your Financial Recovery

The true cost of signing a release of liability becomes painfully clear when you look at your financial future. When you sign, you are accepting a one-time payment and permanently slamming the door on your right to seek another dollar for that accident—no matter how your life changes down the road.

This is a final, binding decision. It means you can't get money for future medical treatments that you might not even know you need yet. It cuts off your ability to be compensated for lost earning capacity if your injuries keep you from returning to your old job. It closes the book on compensation for ongoing physical therapy, chronic pain, and the deep emotional toll that follows a traumatic event.

How Insurance Companies Use Texas Law Against You

Insurance adjusters know Texas law, and they often use it to pressure accident victims into accepting lowball offers. One of their favorite tactics involves Texas's modified comparative fault rule (also known as proportionate responsibility).

Under this rule, you can still recover damages as long as you are not found to be 51% or more at fault for the crash. However, your total compensation will be reduced by your percentage of fault. So, if you have $100,000 in damages but are found to be 20% at fault, you can still recover $80,000.

An adjuster might try to exploit this after a Dallas collision by aggressively claiming you were partially to blame, even with flimsy evidence. They might say, "Our investigation shows you were 30% at fault, so our offer reflects that." Their goal is to make you doubt your claim's strength and rush you into signing a release for a reduced amount, hoping you won't realize you're still entitled to the other 70%.

This is a calculated strategy. Insurers know that an unrepresented victim is far more likely to accept a flawed argument and sign away their rights for a fraction of what their case is truly worth.

Why You Must Understand Your Full Damages First

Before you can even think about a settlement, you need a complete picture of your total losses—both now and in the future. This requires a full medical diagnosis from your doctors, not the insurer's, and a detailed calculation of every single loss you have suffered due to the other party's negligence.

A quick offer from an adjuster will almost never account for the full scope of your damages. The table below shows the difference between what an insurer's first offer usually covers and the full range of damages a Texas personal injury lawyer can help you secure.

Early Settlement vs Full Compensation

| Type of Damage | What an Early Insurance Offer Typically Covers | What a Full Legal Claim Can Recover |

|---|---|---|

| Medical Expenses | Only immediate, documented medical bills. | All past, present, and future medical costs (e.g., surgery, physical therapy, medication). |

| Lost Income | Wages lost right after the accident, if any. | All lost wages, plus future loss of earning capacity if your career is impacted. |

| Pain and Suffering | Usually ignored or severely undervalued. | Full compensation for physical pain, emotional distress, and mental anguish. |

| Property Damage | Basic repair or "blue book" value for your car. | Fair market value for your vehicle, plus potential loss of use damages. |

| Disability & Disfigurement | Almost never included in an initial offer. | Compensation for permanent impairments, scarring, or loss of bodily function. |

| Future Needs | Not considered. | Costs for things like home modifications, in-home care, or assistive devices. |

As you can see, there's a huge gap between a quick check and true financial recovery. To learn more about what goes into calculating a fair amount, you can review the key elements of a Texas auto accident settlement. A thorough evaluation protects your financial stability and ensures you don't pay the price for someone else's negligence for years to come.

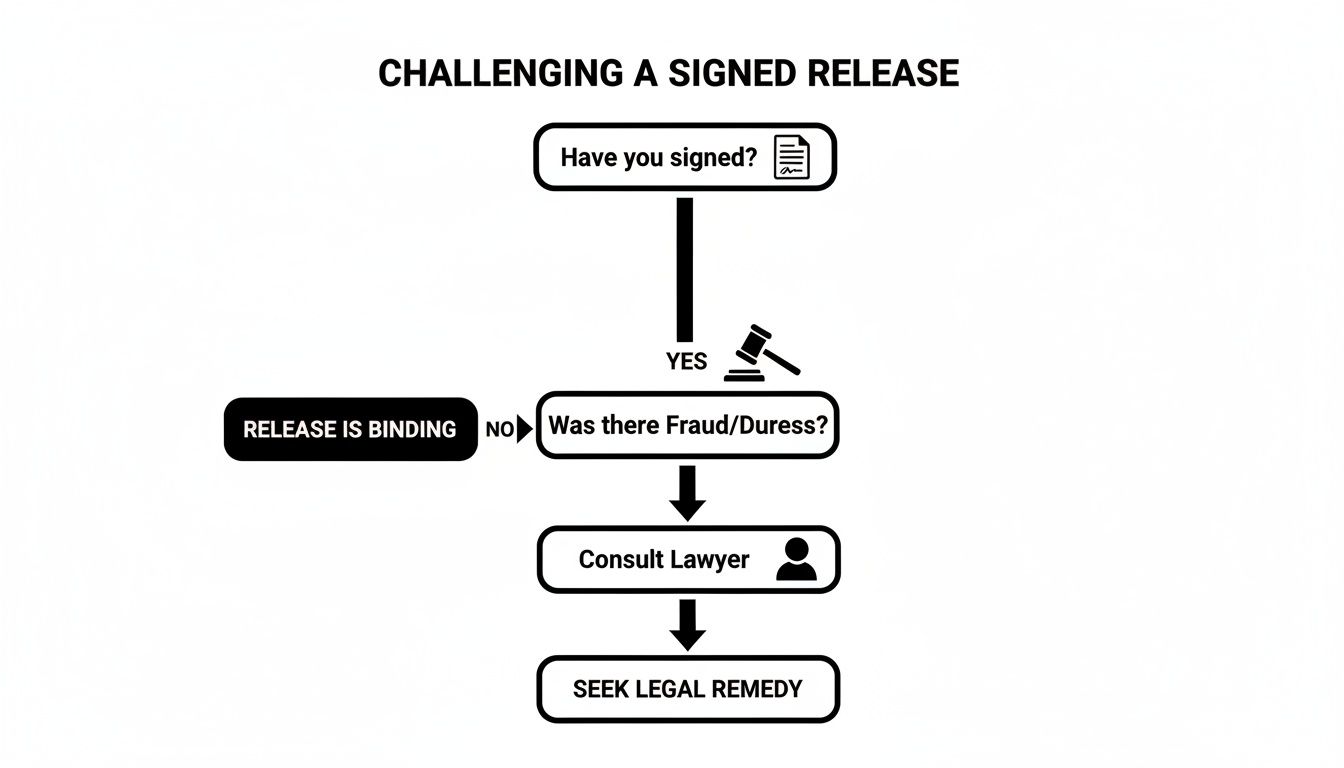

Challenging a Signed Release of Liability in Texas

Once you’ve put your signature on a release of liability, that decision is almost always final. The insurance company will hold up that document as ironclad proof that you accepted their offer and closed the book on your claim forever. But while it's tough, Texas law does recognize a few extremely rare exceptions that can invalidate a signed release.

Let's be upfront: successfully challenging a release you’ve already signed is an incredibly difficult, uphill legal battle. Courts are very hesitant to throw out a signed contract. This reality highlights just how crucial it is to have an experienced Texas personal injury lawyer review any settlement papers before you even think about signing. Think of legal counsel as your proactive shield—it’s there to protect you from making a permanent decision you can't take back.

Limited Grounds for Overturning a Release

You can’t challenge a release just because you have second thoughts or later realize the settlement was far too low. To have any chance, you must prove the contract itself is legally invalid on very specific grounds.

These narrow circumstances include:

- Fraud or Misrepresentation: This isn't just about feeling misled. You would need to prove the insurance adjuster intentionally lied about a critical fact to trick you into signing. A classic example is if they told you the document was just a receipt for an initial payment when it was actually a full and final release of all claims.

- Duress: This means you were forced to sign under an immediate and unlawful threat. Simply feeling the weight of financial pressure isn't enough to meet this high standard. The situation must rise to the level of coercion, leaving you with no other reasonable choice but to sign.

- Mutual Mistake: This is a very specific exception. It applies when both you and the insurance company were fundamentally mistaken about a core fact underlying the agreement when you signed it—not just an injury that pops up later.

Proving any of these is exceptionally challenging. Insurance companies document every phone call and email, and their adjusters are trained to avoid saying anything that could be used against them. Trying to fight this battle on your own is nearly impossible, especially when you might be dealing with tactics that cross the line into bad faith. You can learn more about how to spot and fight back against an insurer’s dishonest behavior by understanding what qualifies as a bad faith insurance claim.

The legal landscape around liability is always shifting. Broader legislative changes in other states, like the recent Florida Tort Reform, can offer valuable insights into the national environment where these releases are negotiated and challenged.

Your Action Plan When an Insurer Hands You a Release

Feeling pressure from an insurance adjuster is a huge red flag. It’s a clear signal that you need to slow down and take back control of the situation. When they slide any document across the table, especially a release of liability, your next moves are absolutely critical. Don’t let them rush you into a decision you can never undo.

Here’s a straightforward, step-by-step game plan to protect yourself and your family:

- Do Not Sign Immediately. Calmly and politely tell the adjuster you need time to review the document and discuss it with your family. Never, ever sign anything at the scene of an accident or while you're on the phone with them.

- Request Everything in Writing. Verbal promises from an adjuster are not legally binding. Insist that the full settlement offer and any other agreements be sent to you in writing. This creates a clear record of what’s actually on the table.

- Decline to Give a Recorded Statement. You are not required to give a recorded statement to the other party's insurer. Adjusters are trained to ask leading questions designed to get you to say something that hurts your claim. Politely decline until you’ve spoken with an attorney. For more advice, check out our guide on how to deal with insurance adjusters.

- Consult an Attorney Before Responding. This is, without a doubt, the most important step you can take. Before you sign any papers, reply to an offer, or even cash a check they send, let an experienced personal injury lawyer review everything. Most offer a free consultation, so you have nothing to lose and everything to gain.

As you navigate this process, it's also smart to get a handle on how to negotiate an insurance settlement to make sure you're getting a fair shake.

The flowchart below shows just how limited your options become if you’ve already signed a release without getting legal advice first.

As you can see, trying to undo a signed release is an uphill battle, only possible under very specific circumstances like proving you were a victim of fraud or signed under duress. This is exactly why getting proactive legal counsel is so essential.

How Long Do You Have to File a Claim in Texas?

In Texas, the statute of limitations for most personal injury cases, including those from car accidents, is two years from the date of the incident. This means you have a two-year window to file a lawsuit. While that may seem like a long time, building a strong case takes time. It’s crucial to speak with an attorney as soon as possible to preserve evidence and protect your rights. Waiting too long can mean losing your right to seek compensation forever.

Frequently Asked Questions About Liability Releases

The aftermath of a serious accident is confusing enough without having to decipher the legal documents an insurance company sends your way. Here are some clear, straightforward answers to the questions we hear most often from our clients about liability releases and the settlement process.

Does Cashing the Settlement Check Mean I Have Accepted the Release?

Yes, in nearly every case. Cashing a settlement check is legally the same as signing on the dotted line. It’s a binding acceptance of the insurance company's offer.

Insurers often print phrases like “full and final payment for all claims” right on the check. Once you deposit or cash it, you’ve likely settled your entire case for that amount, whether that was your intention or not. Never cash a check from an at-fault driver's insurance company without first speaking to a Houston car accident attorney.

What if the Release Only Mentions My Car Damage?

Watch out for this one—it’s a common and dangerous trap. An adjuster might tell you a document is just a simple release for your property damage, but the fine print often contains broad, sweeping language.

This hidden language can release the insurer from liability for all claims tied to the accident, including “all known and unknown” personal injuries. You could sign what you think is a form to get your car fixed and accidentally give up your right to any money for medical bills, lost income, or your pain and suffering.

Can I Negotiate the Terms of a Release Form?

Absolutely. A liability release isn't a take-it-or-leave-it proposition. It’s just one piece of the larger settlement negotiation. An experienced Texas personal injury lawyer can negotiate both the final dollar amount and the specific terms inside the release to make sure your rights are fully protected.

For instance, a lawyer can draft language into the release that specifically protects your right to make a future claim against another at-fault party or ensures that all outstanding medical liens are properly paid from the settlement. This is a complex legal process and not something you should ever try to do alone.

A skilled attorney makes sure the final agreement is fair and actually addresses your needs, not just the insurance company’s desire to close your file.

A serious injury can turn your world upside down, but you don’t have to face the legal system on your own. Recovery is possible, and help is available. The experienced and compassionate attorneys at The Law Office of Bryan Fagan, PLLC are here to protect your rights and fight for the full and fair compensation you are owed. We invite you to contact us for a free, no-obligation consultation to talk about your case and learn how we can help.