A serious accident can change your life in seconds, but you don’t have to face it alone.

You pull into a grocery store, school lot, hospital garage, or shopping center expecting an ordinary stop. Then a driver backs out without looking. A truck cuts across the lane. A pedestrian appears between parked cars. In the next moment, you’re shaken, hurting, and trying to figure out whether this is “just a parking lot accident” or something more serious.

It’s often more serious than people think. Parking lot crashes represent one in five of all U.S. vehicle accidents, and 14% of car insurance claims are tied to these incidents. They also lead to over 60,000 injuries and 500 fatalities annually, according to National Safety Council and industry data summarized here. Low speed doesn’t always mean low harm. Whiplash, broken bones, head injuries, and pedestrian injuries can all happen in a cramped lot or garage.

If you’re reading this right after a crash in Houston, Dallas, Austin, San Antonio, or another Texas community, you probably need clear answers fast. You need to know what to do at the scene, how to deal with insurance, who may be legally responsible, and what happens if the other driver has no coverage.

This guide focuses on the practical side of recovery. It also addresses two issues many people miss. First, a parking lot owner may share responsibility when poor lighting, missing signs, faded markings, or dangerous design helped cause the crash. Second, you may still have a path to compensation if the at-fault driver is uninsured.

A Serious Accident Can Change Your Life in Seconds

A parking lot collision can leave you with a strange mix of emotions. You may feel embarrassed because the crash happened at low speed, angry because the other driver insists it was your fault, or worried because your neck, back, or head didn’t start hurting until after the adrenaline wore off.

Those reactions are normal. Parking lots create confusion. Cars move in different directions. People back out at the same time. Shoppers walk between vehicles. Signs are easy to miss. Even careful drivers can find themselves in a bad situation when someone else is distracted or when the property itself isn’t reasonably safe.

Why these crashes deserve serious attention

Many people assume a parking lot crash means minor vehicle damage and a quick insurance call. That assumption causes problems. Injuries often show up later, and fault disputes are common because there may be no traffic signal, no obvious point of impact, and no immediate police investigation.

Practical rule: Treat a parking lot crash like any other injury case. Get medical care, preserve evidence, and don’t decide too early that it’s minor.

Texas law still applies in a private lot. A driver can be negligent for texting, failing to yield, backing up unsafely, or cutting through lanes too fast. A property owner can also face liability when a dangerous condition contributed to the crash. That matters because the path to recovery may be broader than you think.

What helps most in the first few days

The strongest claims usually start with calm, organized action. Focus on a few priorities:

- Get checked by a medical professional: You need treatment, and your records help connect the crash to your injuries.

- Report what happened: A police report or incident report creates a paper trail.

- Save what you can: Photos, witness names, and video locations can matter later.

- Be careful with insurance: Early statements can lock you into facts you didn’t mean to admit.

A Houston driver sideswiped in a mall garage may assume the insurer will sort it out. A Dallas parent hit while loading groceries may think the case is too small to pursue. Both can be wrong. The right next steps often make the difference between a disputed claim and a recoverable case.

Your First Moves After a Texas Parking Lot Crash

The first hour after a crash is usually messy. People are upset, traffic builds up, and everyone wants to decide fault on the spot. Don’t rush into that. Start with safety, then create a clean record.

Start with safety and medical needs

Check yourself first, then passengers, then anyone else involved. If someone may be hurt, call 911. That includes dizziness, neck pain, confusion, numbness, trouble walking, or any head strike. A “small” crash can still cause meaningful injury.

If the vehicles can be moved safely, move them out of the traffic lane. If they can’t, leave them where they are and wait for help. Turn on hazard lights if possible.

A low-speed impact in a busy Houston Galleria parking garage can quickly become a second hazard if cars stack up behind you. Your first job is to keep the scene from getting worse.

Exchange information, but don’t argue

You need basic facts from the other driver. You do not need a debate.

Get:

- Full name and contact details: Phone number, address, and email if available.

- Insurance information: Carrier name, policy number, and the name of the insured person.

- Vehicle details: License plate, make, model, and color.

- Driver details: If someone other than the owner was driving, note that clearly.

Avoid saying “I’m sorry,” “I didn’t see you,” or “This was probably my fault.” Those statements can be used against you later, even when the full picture shows shared fault or unsafe property conditions.

Keep your words simple. “Let’s exchange information.” “I’m going to call the police.” “I’d like to document the scene.”

Report the crash

Even in a private lot, reporting the crash helps. Call law enforcement if anyone is injured, if a driver appears impaired, if there’s a hit and run, or if the other person refuses to cooperate. If the crash happened at a business, ask management to create an incident report.

A report won’t decide the whole case, but it often preserves timing, location, party names, and first observations. That can matter a great deal later.

What not to do at the scene

Some mistakes create lasting problems:

- Don’t leave too soon: If you go without exchanging information or reporting the crash, the other side may tell a different story.

- Don’t minimize your injuries: You don’t know yet how your body will feel tomorrow.

- Don’t accept cash on the spot: Quick payment offers usually protect the other driver, not you.

- Don’t get pulled into blame games: Parking lot fault is often more complicated than people think.

A calm response protects your health and your claim. The scene is not the place to settle the case.

Gathering Critical Evidence to Build Your Claim

The evidence you collect right away often decides whether your claim is strong later. Parking lot cases can turn on details that disappear quickly. Vehicles get repaired. Witnesses leave. Security video is overwritten. Rain washes away marks. Store managers change shifts.

Your phone is one of the best tools you have in that moment.

Use your phone like an investigator

Take more photos than you think you need. Start wide, then move close.

Capture:

- The full scene: Show the lane, parking spaces, nearby storefronts, curbs, and traffic flow.

- Vehicle positions and damage: Photograph each side of both vehicles, license plates, and debris.

- Signs and markings: Stop signs, arrows, crosswalks, faded lines, missing signs, and blocked sight lines.

- Visible injuries: Bruising, swelling, cuts, and torn clothing.

Short video can help too. Walk the scene slowly and narrate what you’re seeing if you can do so safely. Mention the time, weather, and where each car came from.

Witnesses matter more than people expect

Parking lot crashes often become one driver’s word against another’s. An independent witness can break that tie.

Ask nearby shoppers, employees, delivery drivers, or pedestrians if they saw what happened. Get names and contact information. If they’re willing, ask them to text or email you a short summary while the memory is fresh.

A witness who says, “The SUV was speeding down the lane while the other car was already backing carefully,” can change the entire direction of a claim.

Don’t worry about getting a polished statement. Basic facts are enough. What they saw. Where they were standing. Which direction each vehicle moved.

Look for cameras before you leave

Parking lots and garages often have surveillance from stores, banks, apartment buildings, office buildings, or parking management companies. Don’t assume someone will save that footage for you.

Write down where cameras are located. Note the business name closest to each one. If possible, ask the store or property manager how video requests are handled. That early note can help your lawyer send a preservation request before footage disappears.

If police responded, ask when and how to obtain the report. This guide on how to read a Texas police accident report can help you understand what to look for once it becomes available.

Save evidence beyond the scene

Evidence doesn’t stop with photos from the lot. Keep a simple recovery file with:

- Medical paperwork: Discharge papers, visit summaries, imaging orders, prescriptions.

- Work records: Missed shifts, supervisor emails, pay records showing lost income.

- Repair estimates: Property damage documents can support the force of impact.

- A pain journal: Brief daily notes about sleep problems, pain levels, and activity limits.

That file helps tell the story insurance companies often try to shrink. A parking lot collision may not look dramatic, but the effect on your life can still be substantial.

Navigating Insurance Calls and Avoiding Early Mistakes

Insurance contact usually starts fast. Sometimes your own carrier calls first. Sometimes the other driver’s insurer does. The tone may sound friendly, but the goal is business. The adjuster is evaluating risk and looking for ways to limit what the company pays.

That doesn’t mean you should be hostile. It does mean you should be careful.

What to say when the adjuster calls

You can report the basic facts. Date, time, location, vehicles involved, and whether you sought medical care. Keep it short and factual.

Good examples include:

- Basic identification: Confirm your name, policy information, and contact details.

- Crash facts: State where the collision happened and that the matter is under review.

- Medical status: Say you’re being evaluated or are still receiving treatment if that’s true.

What you should avoid is just as important. Don’t guess about speed, distance, visibility, or fault. Don’t say you’re “fine” if you’re still sore, dizzy, or waiting for an appointment. Don’t speculate about what the other driver “must have thought.”

A detailed guide on what to say to insurance after an accident can help you prepare before that first conversation.

Recorded statements and quick settlement offers

You’re usually better off not giving a recorded statement to the other side early in the case. Adjusters ask broad questions because broad answers can later be used against you. A simple inconsistency can become the excuse for a reduced offer.

Quick settlements are another trap. A person in Austin may get a call after a store-lot crash and hear that the insurer wants to “help close this out quickly.” The offer might cover a tow bill and a first clinic visit. Then the neck pain worsens, imaging is ordered, and the file has already been signed away.

Bottom line: If you don’t know the full extent of your injuries, you don’t know the value of your claim.

Common mistakes that weaken claims

Some errors hurt people over and over again:

| Early mistake | Why it causes problems |

|---|---|

| Saying “I’m okay” too soon | The insurer may treat that as proof you weren’t injured |

| Accepting the first check | You may waive the right to pursue more compensation |

| Posting on social media | Photos and comments can be taken out of context |

| Missing follow-up care | The insurer may argue your injuries weren’t serious |

The same problem appears in many forms. The injured person tries to be reasonable. The insurance company treats that reasonableness as a discount.

A better approach

Report the claim. Get medical care. Save your paperwork. Don’t sign releases you haven’t reviewed carefully. If the facts are disputed, if you were hurt, or if a property hazard may have contributed, legal guidance early in the process usually protects more than it costs.

That’s especially true in parking lot cases because liability isn’t always limited to one driver.

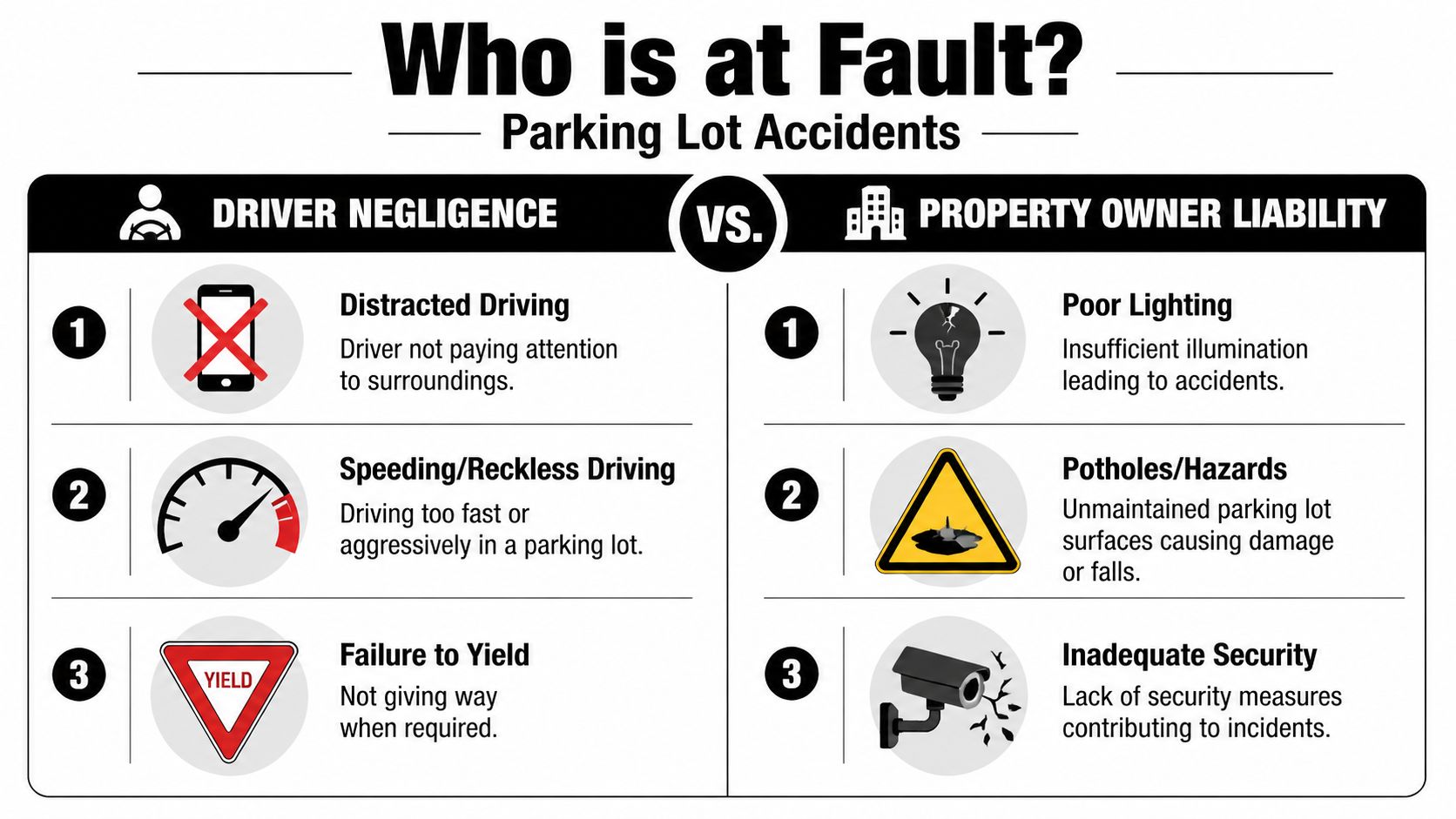

Who Is Really at Fault? Driver Negligence vs Property Owner Liability

A parking lot crash can look simple for about five minutes. Then the stories split. One driver says the other cut across the row. The other says there were no visible arrows or stop signs. A pedestrian says the area was so dark that neither driver could see clearly.

That is why fault in these cases often has two parts. One part is the driver’s conduct. The other is the condition of the property.

When the driver caused the crash

Many parking lot claims start with ordinary negligence. The driver was backing up without looking, cutting diagonally across parked rows, checking a phone, driving too fast for a crowded lot, or failing to yield to a car already traveling through the lane.

Small details decide these cases. I look at who had the better view, which vehicle was established in the lane first, whether anyone ignored signs or pavement markings, and what witnesses or cameras captured.

Common examples include:

- Unsafe backing

- Distracted driving

- Failure to yield in travel lanes

- Ignoring pedestrian walkways

- Speeding through a busy lot

Texas uses proportionate responsibility rules. More than one person can share fault. That matters because insurance companies often try to turn a clear case into a shared-blame argument to reduce what they pay.

When the property owner may share responsibility

Many injured people never get told this part. The driver may not be the only one responsible.

If poor lighting, missing signs, faded striping, broken pavement, blocked sight lines, or a dangerous layout contributed to the collision, the property owner or manager may also be liable under Texas premises liability law. If you want a plain-English overview of that legal framework, this explanation of Texas premises liability law is a good starting point.

The key question is not whether the crash happened on private property. The question is whether the owner knew, or should have known, about an unsafe condition and failed to fix it or warn people about it.

That distinction can make a major difference in recovery. It can open another insurance policy. It can also matter when the at-fault driver has little coverage or none at all.

What unsafe conditions look like in practice

Property cases are usually built on conditions people have seen for weeks or months before the collision:

- Poor lighting that makes drivers, pedestrians, and curbs hard to see

- Faded arrows or lane markings that leave traffic flow unclear

- Missing, damaged, or hidden signs at intersections and exits

- Potholes, broken pavement, or uneven surfaces that force sudden swerves

- Overgrown landscaping, cart corrals, or fixtures that block visibility

A responsible owner is expected to inspect and maintain the lot. This parking lot maintenance checklist shows the kinds of issues that should be caught and addressed, including lighting, signage, striping, and pavement conditions.

How these cases are proved

Property owners are not automatically liable because a wreck happened on their land. Proof matters. The claim has to connect the dangerous condition to the crash and show the owner had notice of the problem.

That usually means getting evidence fast. Useful records include maintenance logs, inspection reports, repair requests, prior incident reports, surveillance video, photos of the scene, and complaints from tenants or customers. If a light had been out for weeks, the striping had worn away, or prior near-misses were reported, those facts can shift the case.

Timing matters here more than many people realize. Parking lots get patched, restriped, cleaned, and repainted. Video gets erased. Witnesses forget details.

A Texas example

Take a retail center outside Fort Worth. Two vehicles collide at dusk near the end of a parking row. At first glance, it looks like a routine dispute between drivers.

Then the evidence fills in the picture. The directional arrows are barely visible. Several overhead lights are out. A stop sign is partly hidden by tree growth. Store employees say people had complained about the area before.

Now the case has two tracks. One driver may have made a bad decision. The property owner may also have allowed a dangerous condition to stay in place.

That broader view matters, especially in serious injury cases and in uninsured-driver claims. When one source of recovery falls short, a careful look at property owner liability can change the outcome.

Calculating the Full Value of Your Parking Lot Accident Claim

A parking lot wreck can leave relatively minor vehicle damage and still produce a serious injury claim. I often see cases where the photo of the bumper looks modest, but the client is dealing with weeks of treatment, missed work, and pain that affects ordinary tasks at home.

Claim value turns on impact. How badly were you hurt. What care did you need. What income did you lose. What parts of daily life became harder, slower, or impossible. In Texas, a careful claim should measure all of that, especially when the case may involve both a negligent driver and an unsafe parking lot condition.

Economic losses you can document

These are the financial losses tied to the crash and your recovery. They usually include ambulance bills, ER care, follow-up visits, physical therapy, imaging, prescriptions, lost pay, and property damage. In some cases, they also include future treatment and reduced earning capacity if the injury limits the type of work you can do.

A Texas parking lot case can produce a surprisingly long paper trail. A parent struck in a school pickup lot may need orthopedic care and miss shifts for appointments. A delivery driver hurt in a retail center may lose income for as long as lifting, bending, or prolonged driving remains painful. Those losses should be counted, not brushed aside as inconvenience.

Helpful records include:

- Medical bills and treatment records

- Doctor's notes about work restrictions

- Pay stubs or other proof of lost income

- Receipts for medication, braces, rides, and other out-of-pocket costs

- Repair estimates, photos, and vehicle damage invoices

The key trade-off is simple. Waiting until the end of treatment may give a clearer picture of the full loss, but early settlement pressure often starts long before that. A quick payment can leave future care unpaid.

The part of the claim that has no receipt

Pain matters. So does loss of sleep, limited movement, anxiety in parking garages, headaches, trouble focusing, and the strain an injury puts on parenting, work, and relationships.

These losses are harder to measure, but they are no less real. A back injury may keep someone from lifting a child. A concussion may interfere with concentration for months. A pedestrian hit in a crowded lot may become fearful every time a car backs out nearby.

Strong cases show the human effect of the injury with specifics. Keep a short journal. Note pain levels, missed events, work problems, activity limits, and bad days that do not appear in a billing statement. Honest detail carries more weight than exaggeration.

Uninsured drivers can change the recovery strategy

Parking lot crashes often involve hit-and-runs, drivers with no insurance, or drivers whose policy limits are too low for the harm they caused. That does not end the case. It changes where recovery may come from.

In Texas, your own Uninsured/Underinsured Motorist coverage may apply if the at-fault driver cannot pay the claim. The Texas Department of Insurance explains how uninsured and underinsured motorist coverage works and what it may cover: Texas Department of Insurance guide to UM/UIM coverage.

That issue becomes especially important in parking lot cases because low-speed assumptions can hide significant injuries, and because another source of recovery may exist. If poor lighting, missing signs, broken pavement, or faded traffic markings contributed to the crash, the value analysis should also consider a potential claim against the property owner. In some cases, that additional claim is what makes full recovery possible.

Your own insurance company may still dispute injury severity, fault, or whether a hit-and-run qualifies under the policy. I tell clients to treat those claims with the same care they would use against the other driver's insurer. Give prompt notice. Be accurate. Do not guess. Do not let an adjuster reduce the claim to car damage alone.

Fatal parking lot crashes and family claims

Some parking lot collisions lead to fatal injuries, especially when a pedestrian, child, older adult, or cyclist is struck. In those cases, surviving family members may have a wrongful death claim under Texas law, along with related claims tied to medical expenses, funeral costs, lost financial support, and the loss of the relationship itself.

These cases require a wider damages review than a standard injury claim. If the crash involved reckless driving, a commercial vehicle, or dangerous premises on private property, every source of liability and insurance coverage needs to be examined carefully.

When to Contact a Texas Parking Lot Accident Lawyer

You leave a store, pull into the driving lane, and a crash that looked minor at first turns into weeks of doctor visits, missed work, and arguments with insurers about who caused it. That is the point when many people realize a parking lot case is not simple at all.

The right time to call a lawyer is usually earlier than people expect, especially in Texas parking lot cases involving unclear fault, uninsured drivers, or unsafe property conditions. Those claims can turn on video footage, incident reports, maintenance logs, and witness statements that do not stay available for long.

The cases that need legal help fastest

Call a lawyer promptly if your case involves more than a scraped bumper and a quick repair. In my experience, these cases need immediate attention:

- Your injuries keep interfering with daily life: Pain that lasts, new symptoms, or treatment beyond an urgent care visit usually means the claim needs medical proof and careful presentation.

- Fault is disputed: Parking lot collisions often involve two drivers blaming each other for backing, speeding, cutting across lanes, or failing to yield to pedestrians.

- Unsafe property conditions may have played a role: Poor lighting, faded arrows, broken pavement, missing stop signs, or blocked sight lines can create a separate claim against the property owner.

- The other driver has no insurance or cannot be found: Uninsured and hit-and-run claims require quick notice to your own carrier and close attention to policy terms.

- A family member suffered catastrophic injuries or died: Those cases need immediate evidence preservation and a broader damages review.

Commercial vehicle involvement also changes the case. If a delivery driver, contractor, rideshare driver, or company vehicle was involved, you may be dealing with an employer, a business policy, and records that should be requested before they disappear.

Why early representation can make a real difference

Early legal help is not about filing a lawsuit on day one. It is about protecting the facts before they change.

A lawyer can send preservation notices for surveillance footage, obtain store or apartment complex incident reports, identify whether the property owner outsourced maintenance, and document the condition of the lot before repairs are made. That work matters most in the two parking lot situations people overlook: cases where the property itself contributed to the crash, and cases where the at-fault driver has little or no insurance.

Here is what early action often looks like:

| Legal task | Why it helps |

|---|---|

| Send preservation letters | Helps keep video, reports, and maintenance records from being lost |

| Inspect the scene quickly | Documents lighting, striping, signage, pavement defects, and visibility issues |

| Collect witness statements | Preserves details before memories fade |

| Coordinate medical records and billing | Ties treatment to the crash and shows the full impact of the injury |

| Handle insurer communications | Reduces the risk of damaging statements and rushed settlements |

| Identify every liable party | Examines the driver, property owner, business operator, employer, and available insurance policies |

That wider review can change the outcome. A driver may have no usable coverage, but the property owner or business may still bear responsibility if unsafe conditions helped cause the collision.

Texas deadlines and practical urgency

Texas injury claims are subject to filing deadlines, and waiting is risky even when the deadline has not arrived. Parking lot evidence is fragile. Video may be overwritten in days. A manager may transfer to another location. Lane markings may be repainted after a complaint. A broken light may be fixed before anyone documents it.

Premises-related claims often require more than showing a crash happened. You may need proof that a dangerous condition existed, that the owner knew or should have known about it, and that the condition contributed to the injury. That proof is much easier to gather at the beginning than months later.

Cost concerns should not keep you from getting answers

A consultation gives you information. It does not commit you to a lawsuit.

Many Texas personal injury lawyers handle these cases on a contingency fee basis, which means attorney's fees are paid from a recovery rather than upfront. That arrangement lets injured people get legal advice while they are dealing with treatment, car repairs, and lost income.

If your case involves disputed fault, an uninsured driver, a hit-and-run, or signs that the parking lot itself was unsafe, get legal advice soon. A good lawyer should be able to tell you where the claim stands, what evidence needs to be preserved, whether a property owner may share fault, and what recovery options exist. You should not have to sort through all of that on your own.