A serious accident can change your life in seconds, but you don't have to face it alone.

You may already be dealing with pain, medical appointments, missed work, car repairs, and constant calls from adjusters. Then the denial letter arrives. It can feel like a second collision. Many people read that letter and assume the insurance company has made the final decision. In Texas, that usually isn't true.

If you're searching for what if insurance denies my claim Texas, the first thing to know is simple. A denial is often the insurer's position, not the last word on your case. Insurance companies deny claims for many reasons, including disputed fault, missing records, policy language, or a claim that they say was not documented well enough. Sometimes the denial is direct. Sometimes it shows up as a delay, a partial payment, or an offer that doesn't come close to covering what you've lost.

Texas personal injury law also matters here. Most injury claims turn on fault and negligence. In plain English, that means who caused the crash and whether that person failed to act with reasonable care. Texas also follows a modified comparative responsibility rule. If the insurer argues that you share blame, that can reduce or even block recovery depending on the facts. That is why the wording in a denial letter matters so much.

After a Houston freeway crash, for example, an insurer may say you changed lanes unsafely, even when the police report, vehicle damage, and witness statements tell a different story. In a truck collision, the carrier may focus on one small inconsistency in your account while ignoring the driver logbooks, black box data, or medical records that support your claim. In a wrongful death case, the family may be told the loss is being “reviewed” while key financial and medical evidence sits untouched.

You still have rights. You may be able to appeal. You may be able to challenge a low payment. You may need to make a claim under your own policy instead of waiting on the other driver's carrier. And if the insurer keeps acting unreasonably, you may need to escalate.

Introduction A Denial Is Not the Final Word

The worst time to receive a denial letter is when you're already overwhelmed. You've done what you thought you were supposed to do. You reported the accident, got treatment, answered questions, and sent documents. Then the company says no.

That doesn't mean your case is weak. It means the insurer has taken a position that now needs to be tested against evidence, policy language, Texas procedure, and the actual value of your losses.

Why denial letters cause so much confusion

Most denial letters are written in formal language. They may mention “insufficient proof,” “liability investigation,” “coverage concerns,” or “failure to substantiate damages.” Those phrases can sound final, but they often hide a simpler dispute.

Here is what the insurer may really be saying:

- They dispute fault: They think they can blame you, in whole or in part.

- They want more proof: They believe your medical records, photos, bills, or repair estimates are incomplete.

- They are relying on policy terms: They say a deadline, exclusion, or coverage limit applies.

- They are testing whether you'll push back: Some people give up after the first denial or low offer.

Practical rule: Treat every denial letter like a roadmap. It tells you where the fight is.

Texas fault rules still control many injury claims

In a Texas injury case, the legal questions usually start with negligence. Did another driver run a red light, follow too closely, speed, text while driving, or fail to yield? If so, that conduct may support liability.

Texas also uses comparative responsibility. If the insurer can persuade a jury that you were partly at fault, your recovery can be reduced. If they push the blame too far, they may try to cut off the claim entirely. That's why you should never accept the insurer's version of events without checking it against the evidence.

After a rear-end collision on I-10, the carrier might argue you stopped suddenly. After a commercial truck crash near Houston, the defense may claim visibility or traffic conditions made the wreck unavoidable. Those arguments often sound stronger in a denial letter than they do when matched against photos, witness statements, and medical timelines.

You have more than one path forward

A denied claim doesn't always require the same response. Some situations call for a direct internal appeal. Others require a stronger written dispute, a demand letter, or a shift to first-party benefits under your own policy. If the claim involves a fatal collision, catastrophic injury, or disputed long-term care needs, the right strategy becomes even more important.

People often wait too long because they think they need a perfect file before taking the next step. They don't. They need a prompt, organized response.

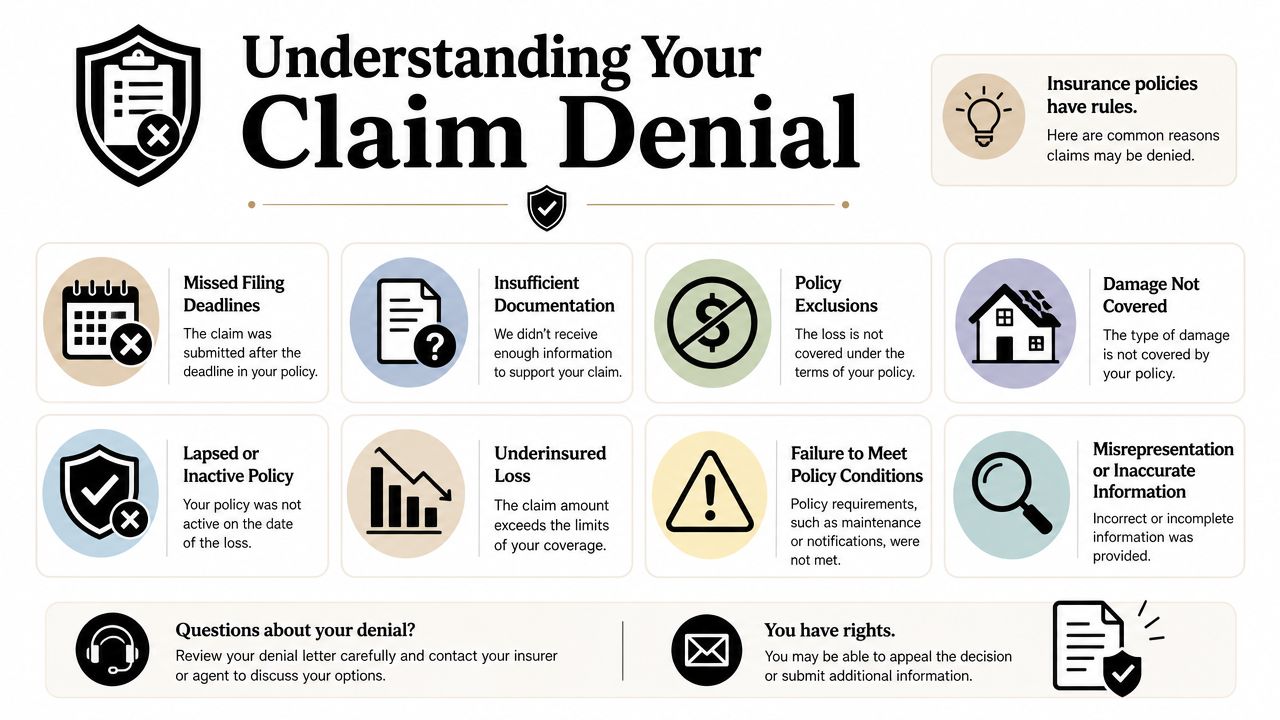

Understanding the Reasons Behind Your Claim Denial

Before you challenge a denial, you need to decode it. The insurer's stated reason matters because your response has to meet that reason head-on.

In 2023, insurers on HealthCare.gov denied 20% of all in-network and out-of-network claims, and Texas policyholders are told to appeal directly to the insurer first and act quickly because deadlines are strict, according to the Texas Medical Association summary of the Texas denial and appeal process. That same practical lesson applies across many Texas insurance disputes. The denial reason drives the next move.

The most common denial arguments

Some denial letters are blunt. Others are vague on purpose. These are the patterns I see most often in Texas injury and accident claims.

Disputed liability

The insurer says its driver didn't cause the crash, or that you caused part of it. After a Houston freeway wreck, this often shows up when both drivers blame each other for a lane change or sudden stop.Pre-existing injury claims

The carrier argues your pain, surgery, or treatment came from an earlier condition instead of the collision. That doesn't automatically defeat the claim. It means the medical evidence has to show how the crash changed your condition.Lack of documentation

This can involve missing bills, gaps in treatment, missing photos, incomplete repair estimates, or weak proof of lost wages.Policy exclusions or coverage defenses

The insurer may point to policy language, reporting issues, or categories of damage it says are excluded.

A denial reason is not a verdict. It's an argument drafted by the company that has to pay if your claim succeeds.

Read between the lines

If the letter says “we cannot determine liability,” ask what evidence they relied on. If it says “treatment was not medically necessary,” compare that statement to your doctor's records. If it says “damages are unsupported,” look for the missing piece. It may be wage records, an imaging report, or a more detailed repair estimate.

For property-related disputes, it can help to review examples of common roof insurance claim rejections because they show how insurers frame exclusion, wear-and-tear, and documentation arguments. The same logic often appears in auto and injury files, even when the loss is completely different.

If you want a broader look at insurer tactics, this guide on why insurance companies deny claims is also useful.

A Houston example

A driver is hit on the Katy Freeway. The other vehicle drifts into her lane. The insurer denies the claim and says she may have been comparatively responsible because traffic was heavy and the lane position is “unclear.”

That sounds serious until the file is rebuilt. Her vehicle damage matches a sideswipe from the left. A witness confirms the lane drift. Her treatment began right away. The police report identifies the other driver. The denial may collapse once those pieces are organized and presented together.

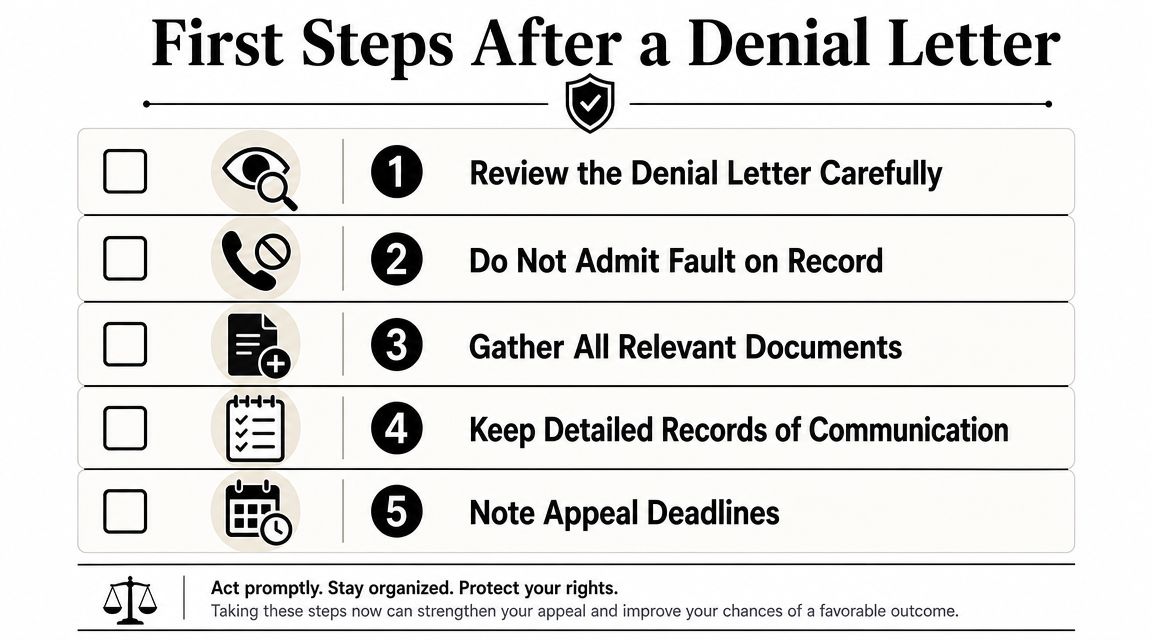

Your First Steps After Receiving a Denial Letter

The first hours after a denial are more critical than generally acknowledged. Don't call the adjuster in anger. Don't guess at facts. Don't give a recorded statement without legal advice if the claim is disputed.

Start by protecting the file.

A practical Texas claims-denial workflow includes preserving the denial letter, requesting the full claim file, and filing a written dispute. One Texas guide recommends acting within 72 hours to preserve evidence and notes that appeal timing is often about 180 days, so missing the deadline can cost you the right to challenge the denial, as explained in this Texas insurance denial appeal guide.

What to do immediately

Use a simple checklist and keep everything dated.

Save the denial letter

Keep the envelope, email header, or portal screenshot showing when you received it.Request the complete claim file in writing

Ask for the adjuster notes, estimates, photos, recorded statements, and all documents the insurer relied on.Build one evidence folder

Include crash photos, police report, medical records, bills, pharmacy receipts, towing invoices, rental car charges, and wage-loss proof.Write a timeline

Start with the collision and list what happened next. Treatment dates, symptoms, adjuster calls, inspections, and missed work all belong here.Keep communication in writing

Follow up phone calls with email. Written records are easier to use later.

For readers dealing with home or storm-related documentation issues, guidance on getting your hail damage claim approved can be helpful because it shows how detailed photos, estimates, and prompt follow-up strengthen a disputed file.

What not to do

Some mistakes hurt good claims.

- Don't fill in gaps from memory if you're unsure: Guessing can create inconsistencies.

- Don't accept the adjuster's summary of your injuries: Your records and doctors matter more.

- Don't assume silence means review is ongoing: It may mean your file is stalled.

- Don't miss the internal deadline: Late responses can shut down an otherwise valid challenge.

If the company has stopped responding, this article on an insurance company not responding to a claim may help you spot the difference between ordinary delay and a claim that needs stronger action.

Here's a short explainer that covers common denial issues and next steps:

Keep your proof of loss separate from your opinions. Photos, bills, records, and reports usually carry more weight than frustration, even when your frustration is justified.

When to call a lawyer early

If the denial involves major injuries, a fatal crash, a commercial vehicle, or conflicting fault evidence, early legal help can protect your claim. A Texas personal injury lawyer can organize medical proof, preserve witness evidence, and stop damaging communications before they happen.

That matters in a Houston car accident attorney context, but also in truck and wrongful death cases where the insurer's first position may be built around minimizing future losses before your family even understands the full financial impact.

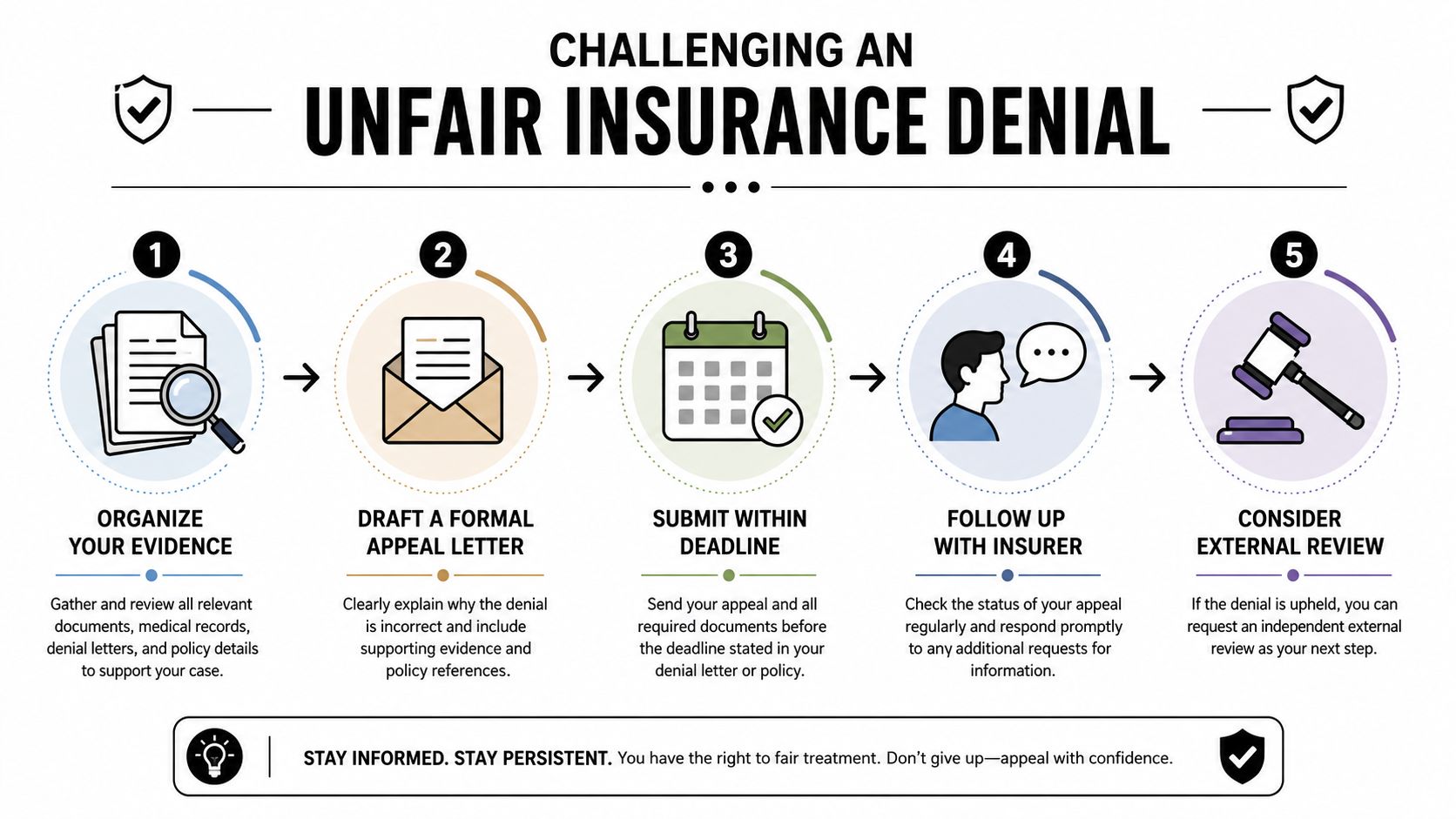

How to Formally Challenge an Unfair Denial

You open the denial letter, read it twice, and realize the insurer is treating its version of events as final. It is not. In Texas, a formal challenge works best when it is organized, documented, and aimed at the exact reason the claim was denied.

A good challenge does two jobs at once. It gives the adjuster a clean path to reverse course, and it creates a record in case the company keeps digging in. That matters because some disputes can still be resolved through a focused written response, while others need a stronger step, such as a demand letter, a complaint, or a claim under your own policy if waiting on the other driver's insurer is slowing your recovery.

The Texas Department of Insurance dispute guidance explains that Texas policyholders can request appraisal in writing in the right case. It also outlines complaint options when a carrier will not fairly address a dispute.

Build your challenge around the denial letter

Start with the letter itself. Do not argue in general terms. Pull out each stated reason for denial and answer it one by one, in the same order the insurer used.

That structure keeps the dispute focused.

| Part of your appeal | What it should do |

|---|---|

| Claim identification | List the policy number, claim number, date of loss, and your contact information |

| Statement of dispute | State plainly that you dispute the denial or underpayment |

| Point-by-point response | Answer each denial reason with facts, records, and attached exhibits |

| Supporting records | Include medical records, bills, photos, repair estimates, wage proof, and witness statements if they apply |

| Requested action | Ask for a specific result, such as reversal of the denial, a new evaluation, or payment by a stated deadline |

How one responds to a denial can make many valid claims stronger or weaker. If the insurer says your treatment was unrelated, answer causation with doctor records, imaging, and a clear timeline. If it says the damage was minor, use photos, repair documentation, and any expert opinion that explains what was missed.

Match your proof to the insurer's excuse

A denial challenge should read like a response to a problem list.

If the insurer claims there is no proof of medical necessity, attach the records that show why treatment was ordered and how the injury affected your daily function. If the company says the repair bill is too high, compare the estimates line by line and identify omitted labor, materials, or procedures. For property-related disputes, resources on crafting Xactimate supplement letters can help show how itemized disagreements are presented clearly.

Keep the tone calm. Keep the facts tight. Angry language rarely changes an adjuster's position, but organized proof often does.

Key point: A strong challenge answers the insurer's stated reasons with evidence, not conclusions.

Decide whether appraisal fits the dispute

Appraisal can help in the right case, but it is not a cure-all. It is usually a value dispute tool. It does not usually resolve a true coverage fight.

Appraisal may make sense when:

- The insurer and repair shop agree there is covered damage, but disagree on the amount

- The carrier's estimate leaves out repair items or uses pricing that does not reflect the actual scope

- The fight is over value, not liability, exclusions, or whether the policy applies at all

In injury cases, appraisal is usually not the main tool. The better question is often whether to keep pressing the at-fault carrier, push back against a low valuation, or use parts of your own policy, such as MedPay or uninsured/underinsured motorist coverage, to avoid unnecessary delay. That is a practical decision, not just a legal one.

Use a demand letter when the dispute is bigger than paperwork

An internal appeal asks the insurer to reconsider. A demand letter puts legal consequences on the table.

In a serious Texas injury claim, the demand letter should explain fault, summarize treatment, document lost income, and describe the losses the first review ignored or minimized. That includes future care when the medical record supports it. In a wrongful death case, it should also address the family's financial loss and the human loss tied to the death.

A demand letter also helps you test the insurer's real position. Some carriers correct course when they see the file is developed and trial-ready. Others respond with another denial or a low offer dressed up as compromise. That response tells you a lot about whether continued negotiation makes sense or whether it is time to shift strategy.

What to Do When the Insurer Makes a Lowball Offer

Many people expect a clear yes or no. What they get is worse. The insurer offers something, but not enough to cover the full loss.

That can happen after a car wreck, truck crash, catastrophic injury, or wrongful death claim. The company sends a check or a settlement number and hopes the stress you're under will do the rest.

The Texas Department of Insurance recognizes that many disputes involve claims the company “didn't pay enough” and advises consumers to get the reason in writing and submit supporting documents, as explained in this Texas Department of Insurance page on denied or underpaid claims.

Why low offers happen

A low offer often reflects one of three things:

The insurer is ignoring future losses

This is common when treatment is ongoing or your doctor hasn't finalized restrictions yet.The file is incomplete

Missing wage proof, specialist records, or imaging results can depress value.The insurer is negotiating from the bottom

Some carriers open low to see whether you know the difference between a quick payment and a fair one.

A real-world example

After a Dallas collision kills a parent, the insurer may quickly focus on final medical bills and funeral expenses while saying very little about the long-term financial and emotional loss to the family. That is not the full value of a wrongful death claim.

A wrongful death lawyer Texas case may involve lost income, lost household support, and the human losses that come with the death itself. If those parts of the claim are missing from the demand package, the insurer has room to pretend the claim is smaller than it is.

How to answer a lowball offer

Don't reject it with anger alone. Reject it with structure.

- Ask for the basis in writing: Make the carrier explain how it valued the claim.

- Correct the record: Send updated treatment records, prognosis information, wage documents, and itemized losses.

- Address future harm: If your injury will affect work, mobility, or ongoing care, that needs to be documented.

- Counter with a supported number: Your response should tie the amount to evidence, not frustration.

If a check doesn't cover the loss, cashing it or signing a release too early can create a second problem that's harder to fix than the first.

In a truck crash lawyer Houston matter, low offers are especially dangerous because commercial cases often involve complicated medical issues, multiple insurance layers, and long-term limitations that aren't obvious in the first weeks after a wreck.

When to Escalate Your Fight and Hire a Texas Lawyer

Some claims can be fixed with a sharp written dispute. Others can't. If the insurer keeps delaying, denying, or underpaying after you've supplied the evidence, it may be time to escalate.

One overlooked move is shifting focus away from the at-fault driver's carrier. When that insurer refuses to pay, a Texas accident victim may be better served by turning to their own Uninsured/Underinsured Motorist or Med-Pay coverage, which can provide a faster path to recovery while preserving the right to pursue the other carrier later, as discussed in this analysis of when the at-fault driver's insurer refuses to pay in Texas.

Escalation options that make sense

A practical escalation path may include:

A formal complaint to the insurer

This creates a cleaner record and sometimes gets the file in front of a different decision-maker.A complaint to the Texas Department of Insurance

This can put pressure on the company to explain its conduct and respond more carefully.A first-party claim under your own policy

UM/UIM and Med-Pay can matter when liability is being stalled or the other driver lacks enough coverage.A lawsuit

Sometimes that is the only way to force production of evidence, challenge bad conduct, and pursue full damages.

When legal help becomes important

Hire a lawyer when the case is serious or the insurer's conduct shows that informal efforts won't be enough. That includes disputed-fault crashes, serious injuries, death claims, commercial vehicle wrecks, and cases involving ongoing medical treatment or future impairment.

A lawyer also helps you stay aligned with the rules that shape Texas injury cases. Fault still matters. Negligence still has to be proved. Comparative responsibility can still reduce recovery. And deadlines still control what you can do in court. The statute of limitations can become a major issue if the insurer delays long enough and you don't act.

If the company's conduct looks unreasonable, you may also need to examine whether the case involves bad faith. This overview of bad faith insurance claims in Texas is a helpful starting point.

A denial can leave you feeling cornered. You are not cornered. You may need a stronger record, a better strategy, or a different insurance path, but recovery is still possible.

If an insurance company has denied your claim, delayed payment, or offered far less than your case is worth, legal guidance can help you protect deadlines, gather the right proof, and choose the right path forward. The Law Office of Bryan Fagan, PLLC offers free consultations for Texas accident victims and families dealing with car wrecks, truck crashes, catastrophic injuries, UM/UIM disputes, and wrongful death claims. You don't have to sort through this alone. Help is available, and your next step can start today.