A serious accident can change your life in seconds—but you don’t have to face the fallout alone. That's where uninsured and underinsured motorist (UM/UIM) coverage comes in. It’s a crucial part of your own car insurance policy, acting as a financial shield when the driver who hit you has no insurance or not enough insurance to pay for the damage they’ve caused.

Your Financial Safety Net After a Texas Car Accident

After a crash caused by another driver's carelessness, the shock and confusion can be overwhelming. You're left dealing with physical pain, emotional trauma, and a sudden, massive disruption to your life. The very last thing you should have to worry about is how you're going to pay for it all.

In a perfect world, the at-fault driver's insurance would cover everything. But what happens when it doesn't? Unfortunately, this is a very common reality on Texas roads.

The Frightening Gap in Coverage

Picture this: After a Houston freeway crash, you're seriously hurt and need an ambulance, emergency room care, and weeks of physical therapy. You can't work, and the medical bills are piling up faster than you can count.

Then you get the devastating news. The driver who hit you was either completely uninsured or only had the bare-bones minimum liability coverage required by Texas law—which is nowhere near enough to cover your actual costs. You’re now facing a massive financial hole. Who pays?

This is the exact scenario where your own uninsured and underinsured coverage becomes the most important financial protection you have. It acts as a safety net, allowing you to file a claim with your own insurance company to get the compensation you need to recover.

Your UM/UIM policy is there to make you whole again, covering the losses that the at-fault driver should have paid for. It is a benefit you have paid for through your premiums, and using it is your right.

How UM/UIM Bridges the Financial Gap

To understand who pays for what, it helps to see a side-by-side comparison of where the money comes from.

Who Pays for Your Damages After a Texas Accident?

| Type of Expense | Covered by At-Fault Driver's Liability (If Sufficient) | Covered by Your UM/UIM Coverage (When Needed) |

|---|---|---|

| Medical Bills (ER, surgery, rehab) | ✔️ | ✔️ |

| Lost Wages | ✔️ | ✔️ |

| Pain and Suffering | ✔️ | ✔️ |

| Vehicle Damage | ✔️ | ❌ (Usually covered by Collision) |

| Wrongful Death Damages | ✔️ | ✔️ |

This table shows how UM/UIM coverage is designed to pick up where a negligent driver's policy leaves off, ensuring your most critical expenses are addressed.

Think of your UM/UIM policy as a shield protecting you and your family from the irresponsible actions of other drivers. In Texas, your claim is still based on the legal principle of negligence—meaning you still have to prove the other driver was at fault for the crash. Once you establish fault, your uninsured or underinsured coverage can step in to pay for a wide range of damages.

This coverage is specifically designed to provide funds for:

- Medical Expenses: This covers everything from the initial ambulance ride and hospital stay to surgeries, physical therapy, and any future medical care related to your injuries.

- Lost Wages: If your injuries prevent you from working while you recover, UM/UIM can compensate you for the income you've lost.

- Pain and Suffering: This compensates you for the physical pain and emotional distress the accident and your injuries have caused you.

- Wrongful Death: In the most tragic cases, this coverage provides vital financial support for families who have lost a loved one in a fatal accident caused by an uninsured or underinsured driver. A dedicated wrongful death lawyer in Texas can explain these rights in more detail.

A serious car or truck crash can leave you feeling powerless, but you have more control than you might realize. Understanding how uninsured and underinsured coverage works is the first step toward reclaiming your future. At The Law Office of Bryan Fagan, we are here to offer clear answers and compassionate legal guidance. You are not alone in this fight. Recovery is possible, and we can help you find the way forward.

The Growing Risk of Uninsured Drivers on Texas Roads

When you get behind the wheel on a Texas highway, you’re placing a certain amount of trust in the drivers around you. You trust they’ll drive responsibly and, just as importantly, that they have the insurance to cover the damage if they cause a crash. Unfortunately, that trust is broken far too often.

Having solid uninsured and underinsured motorist coverage isn't just a "nice-to-have" anymore—it’s an essential shield for every Texas family. The number of drivers on our roads with no insurance at all, or with policies that are laughably inadequate, is a serious and growing problem. This isn't about fear; it's about being prepared.

Understanding the Numbers Behind the Risk

Statistically, every time you commute, you're likely sharing the road with someone who can't pay for the accident they might cause. The latest data paints a pretty clear picture.

According to a study from the Insurance Research Council, a shocking 15.4% of U.S. drivers—that’s more than one in seven—were uninsured in recent years. This number has been climbing, up from 12.4% just a few years earlier. When you add in the drivers who are underinsured—meaning they carry insurance, but not enough to cover a serious wreck—that figure jumps to an estimated 33.4% of all drivers.

This means that roughly one out of every three drivers you pass may not have enough insurance to cover your medical bills, lost wages, and pain if they cause a serious crash.

What This Means for You

Think about the aftermath of a major collision on a busy freeway like I-10 in Houston or I-35 cutting through San Antonio. The costs can spiral out of control in an instant. A single severe injury can easily result in hundreds of thousands of dollars in medical care, physical therapy, and lost income.

Yet, Texas law only requires drivers to carry a minimum of $30,000 in bodily injury liability coverage per person. Anyone who’s dealt with a major injury knows that $30,000 barely makes a dent in the true cost of recovery. If a driver with minimum coverage causes a crash that leaves you with $150,000 in damages, their policy pays the first $30,000. You are stuck trying to figure out how to cover the remaining $120,000 gap.

This is exactly why your own uninsured and underinsured motorist (UM/UIM) coverage is so vital. It’s not just another line item on your insurance bill; it’s the financial backstop that protects you and your family from someone else's irresponsibility. If you want to learn more, read our guide on what to do if someone hits you without insurance.

Your UM/UIM policy creates a path to recovery, no matter what the other driver’s insurance situation looks like. With a compassionate Texas personal injury lawyer on your side, you can hold your own insurance company accountable to pay the benefits you’ve been paying for. You don't have to carry this burden alone. Help is available.

How Uninsured and Underinsured Coverage Actually Works

Trying to make sense of an insurance policy can feel overwhelming, especially when you are recovering from an injury. But when it comes to uninsured and underinsured motorist (UM/UIM) coverage, the idea is actually quite simple. Think of it as a safety net you bought for yourself and your family—a guarantee that if a careless driver hurts you and can't pay for the damage they caused, you won't be left to bear the financial burden.

At its core, your uninsured and underinsured coverage is a way to use your own insurance policy to cover your losses when the at-fault driver either has no insurance or not enough. It’s a benefit you pay for, and you have every right to use it when you need it most.

The Different Layers of UM/UIM Protection

In Texas, this coverage is broken down into a few key parts. Each one protects you from a different kind of financial disaster after a crash.

- Uninsured Motorist Bodily Injury (UMBI): This is the heart of your protection. UMBI is what pays for your medical bills, lost income from being out of work, physical pain, and mental suffering if you're hit by a driver with no liability insurance whatsoever. It's also your lifeline in a hit-and-run crash where the other driver is never found.

- Uninsured Motorist Property Damage (UMPD): This part helps pay to fix your car if an uninsured driver hits you. In Texas, UMPD comes with a mandatory $250 deductible. Often, it’s easier and faster to use your own collision coverage to get your vehicle repaired.

- Underinsured Motorist (UIM) Coverage: This is your financial backstop when the at-fault driver does have insurance, but their policy limits are too low to cover your actual damages. For example, if your medical bills and lost wages total $100,000 but the other driver only carries the Texas minimum of $30,000, your UIM coverage is there to help cover that remaining $70,000 gap.

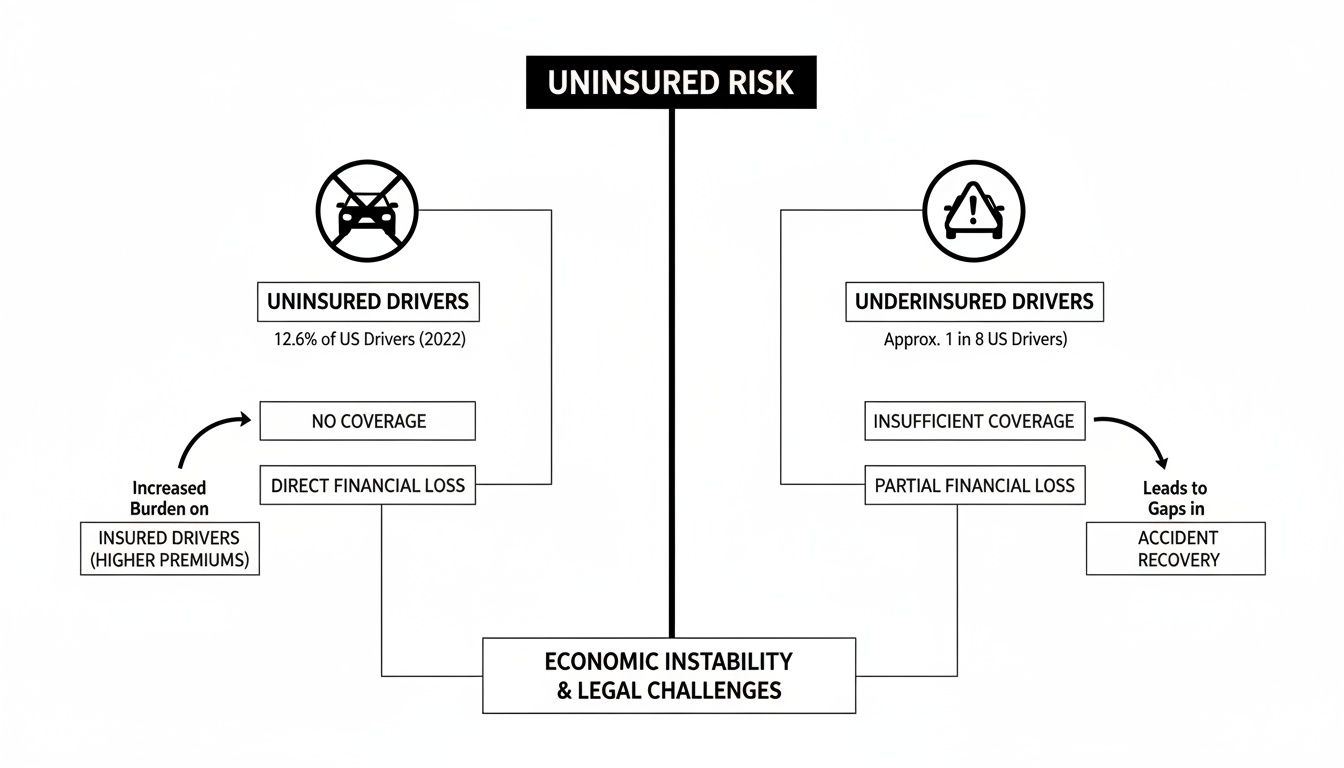

This flowchart breaks down the two types of high-risk drivers your UM/UIM policy is designed to protect you from.

As you can see, whether a driver has zero insurance or just not enough, the financial fallout for you is very real.

How Texas Law Protects You

The state of Texas knows just how crucial this protection is. That’s why insurance companies are legally required to offer you UM/UIM coverage anytime you buy a new auto policy. While you don't have to purchase it, you must actively reject it in writing.

If you do not formally reject UM/UIM coverage in writing, it is automatically included in your policy. This is a crucial safeguard designed to protect Texas drivers from devastating financial losses.

This "opt-out" requirement forces you to make a deliberate choice to go without this protection. From our experience, we strongly advise every driver to carry as much uninsured and underinsured coverage as they can comfortably afford. To dig into the finer points, you can learn more about underinsured motorist coverage in Texas in our in-depth guide.

Why You Still Have to Prove Who Was at Fault

Here is a point that can be confusing: a UM/UIM claim isn't automatic. Even though you have this coverage, you still have the burden of proving that the other driver was legally at fault for causing the accident.

In legal terms, you must establish negligence based on a "preponderance of the evidence." This means you have to show that it's more likely than not that the other driver was careless—they were speeding, texting, or ran a red light, for example—and that their actions directly led to your injuries. This is exactly why getting an experienced Houston car accident attorney involved early is so critical. We take on the fight of proving fault so you can put all your energy into getting better.

What Damages Can You Recover Through a UM/UIM Claim?

When you make a claim against your own uninsured and underinsured coverage, the goal is simple: to make you “whole” again. In legal terms, this means putting you back in the same financial position you were in moments before the crash. Your UM/UIM claim is designed to cover the full spectrum of losses, not just the first ambulance bill.

Think of it this way: your coverage steps into the shoes of the at-fault driver. It’s there to pay for all the ways the accident turned your life upside down, from your physical and financial health to your emotional well-being. It's a safety net you paid for, and now it's time for it to do its job.

Economic Damages: The Tangible Costs

These are the straightforward, calculable losses that come with receipts, invoices, and pay stubs. Your UM/UIM claim is built to cover these immediate and long-term financial burdens so you can focus on healing.

- Current and Future Medical Bills: This goes far beyond the initial ER visit. We're talking about surgery, hospital stays, follow-up appointments with specialists, physical therapy, prescription drugs, and even necessary medical gear like crutches or a wheelchair.

- Lost Wages: If you can't work while you recover, your claim can replace that lost income. This is absolutely critical for keeping your family afloat.

- Diminished Earning Capacity: Sometimes, an injury is so severe it permanently impacts your ability to do your job—or to work at all. Your claim can compensate you for this devastating loss of future income.

Imagine a construction worker in Fort Worth who suffers a severe back injury in a catastrophic injury caused by an uninsured driver. He can no longer do manual labor. His UM/UIM claim wouldn't just cover his surgeries and rehab; it would also account for the difference in income he’ll lose over the rest of his career.

Non-Economic Damages: The Human Cost

These damages are much harder to put a price tag on, but they are just as real and just as devastating. This is compensation for the human toll of the accident, and your uninsured and underinsured coverage is meant to address these profound personal losses.

- Physical Pain and Suffering: This acknowledges the daily physical pain, chronic discomfort, and genuine hardship your injuries have caused.

- Mental Anguish: This is for the emotional trauma—the anxiety, depression, fear, and even post-traumatic stress disorder (PTSD) that often follow a violent crash.

- Permanent Disfigurement: If the accident left you with scars or other permanent marks, your claim can provide compensation for the emotional and social impact.

- Physical Impairment: This covers the loss of enjoyment of life. It’s for not being able to play with your kids, participate in your hobbies, or even just handle daily activities without pain.

A common misconception is that UM/UIM claims only cover medical bills. In Texas, you are entitled to seek compensation for the full range of both economic and non-economic damages, up to your policy limits.

When the Unthinkable Happens: Wrongful Death

In the most tragic cases, a wreck with an uninsured or underinsured driver can result in the loss of a loved one. For a grieving family, a UM/UIM policy can offer a path to justice and much-needed financial stability during an impossible time. A wrongful death lawyer in Texas can help you file a claim to recover damages for:

- Lost earning capacity of the person you lost

- Loss of companionship and the family's mental anguish

- Lost inheritance

- Funeral and burial expenses

Beyond the physical and emotional toll, your UM/UIM coverage can also help with vehicle damage. For some insight into what repair bills might look like, you can check out a helpful Auto Repair Cost Comparison.

With so many drivers on Texas roads without enough insurance, your own policy is often your best—and only—line of defense. According to the Insurance Research Council, about one-third of U.S. drivers were recently either uninsured or underinsured. Even with rising state minimums, a catastrophic injury can easily result in hundreds of thousands of dollars in damages, quickly exhausting an at-fault driver's minimal policy. As you can see by reading more about why this coverage matters, your UM/UIM policy is your lifeline.

What to Do After an Accident with an Uninsured Driver

In the moments after a car crash, your mind is a blur. The shock, pain, and adrenaline make it nearly impossible to think straight. But knowing what to do right after getting hit by an uninsured or underinsured driver is one of the most powerful things you can do to protect your ability to recover.

The steps you take at the scene—and in the days that follow—create the foundation for both your physical and financial recovery. This is your roadmap to taking back control and giving yourself the best shot at securing the compensation you’re owed through your own uninsured and underinsured coverage.

Practical Advice for What to Do at the Scene

Your absolute first priority is safety. If you can, get your vehicle out of traffic and to a safe spot. Once you're out of harm's way, focus on these critical actions. They are essential for creating the official record needed to prove your case.

Call 911 Immediately: Never agree to "handle it without insurance," especially if the other driver seems hesitant to call the police. A police report is one of the most vital pieces of evidence you can have. It officially documents the facts of the crash, identifies everyone involved, and often includes the officer's initial thoughts on who was at fault.

Seek Medical Attention: Get checked out by paramedics at the scene or go to an emergency room, even if you think you feel fine. Adrenaline is a powerful painkiller and can easily mask serious injuries like whiplash or internal damage. A professional medical evaluation creates a crucial, time-stamped link between the accident and the harm you suffered.

Gather Evidence and Information: If you're physically able, use your phone to document everything. Take photos and videos of the damage to both cars, their positions on the road, any skid marks, the weather conditions, and your visible injuries. Be sure to get the other driver’s name, address, and phone number, and do the same for anyone who witnessed the crash.

A common mistake people make is thinking their own insurance company will automatically be on their side. They are still a business, and their goal is to pay out as little as possible—even on your own UM/UIM claim. Every piece of proof you gather helps your attorney hold them accountable to their policy.

How to Handle Insurance Companies in the Days that Follow

Once you're safe and have gotten initial medical care, the next steps are just as crucial for protecting your future. Time is not on your side, and acting quickly and strategically can make all the difference.

You must notify your own insurance company about the accident to open a claim under your uninsured and underinsured coverage. This is where you have to be extremely careful.

Do not give a recorded statement to any insurance adjuster without speaking to an attorney first. Adjusters are trained to ask leading questions designed to get you to downplay your injuries or accidentally admit some fault. A Houston car accident attorney will handle these conversations for you, making sure your words aren't twisted and used against you later.

How Long Do You Have to File a Claim in Texas?

In Texas, the law sets a strict time limit for taking legal action after an accident. This deadline is called the statute of limitations, and for most personal injury claims, it is two years from the date of the crash. If you miss this deadline, you lose your right to file a lawsuit forever.

Two years might sound like a lot of time, but building a strong case is a long process. Your legal team needs to thoroughly investigate the wreck, collect all your medical records, and calculate the full extent of your damages. That’s why it’s so important to act quickly.

Beyond documenting the scene, you'll also have to deal with your vehicle's condition. Knowing the local requirements for a vehicle safety inspection can help you figure out the next steps for repairs and staying compliant with the law.

Suffering a serious injury can make you feel completely alone, but you have rights and you have options. At The Law Office of Bryan Fagan, we’re here to give you the clear answers and strong advocacy you need. Recovery is possible, and getting the right help is the first step.

When to Call a Lawyer for Your UM/UIM Claim

After you've been hit by a driver with little or no insurance, you might expect your own insurance company to step up and do the right thing. After all, you’ve faithfully paid your premiums for exactly this kind of situation. The protection you paid for should be there when you need it.

Sadly, that’s often not how it works.

A claim for uninsured and underinsured coverage can quickly turn into an uphill battle. Your own insurance company becomes an opponent. They are a business, and their goal is to pay out as little as possible to protect their profits. This is the moment an experienced Texas personal injury lawyer becomes your greatest asset.

You don’t have to fight this battle on your own. Having a dedicated legal team in your corner levels the playing field, ensuring your rights are protected from the very beginning.

We Conduct a Thorough Investigation

The first thing we do is launch our own investigation into the accident. We never just take the insurance adjuster's version of events at face value.

Our team immediately gets to work to:

- Secure the official police report and comb through every single detail.

- Track down and interview eyewitnesses to build a clear, undeniable narrative of how the crash occurred.

- Bring in accident reconstruction experts, if necessary, to scientifically prove the other driver was 100% at fault.

This detailed evidence gathering is the foundation we build on to win your UM/UIM claim.

Calculating the Full Value of Your Claim

Insurance companies will almost always try to pressure you into a quick, lowball settlement that barely covers your immediate bills. We don't let that happen. Our job is to calculate the full, true value of all your losses.

This goes far beyond just your current medical bills and missed paychecks. We account for the long-term costs, like future surgeries or physical therapy, a diminished earning capacity if you can't return to your old job, and the very real non-economic damages like your physical pain and emotional trauma.

Your insurance adjuster will not help you add up these future and intangible losses. A truck crash lawyer Houston has the experience to ensure every single damage is identified and accounted for, so you can demand the maximum compensation you are owed.

Fighting Back Against Insurance Company Tactics

Your insurance company has a team of adjusters and lawyers whose entire job is to minimize or deny your claim. Our job is to counter their every move.

We handle all communications, shielding you from their high-pressure tactics and tricky, leading questions.

If your insurer tries to unfairly deny, delay, or lowball your claim, we are ready to hold them accountable. This behavior can sometimes cross the line into insurance bad faith. You can learn more about what constitutes a bad faith insurance claim and how to fight back.

At The Law Office of Bryan Fagan, we take this entire burden off your shoulders so you can focus on the one thing that matters: your recovery. We work on a contingency-fee basis, which means you pay absolutely no fees unless we win your case. Help is available, and with our team fighting for you, you can get the justice you deserve.

Answers to Your Texas UM/UIM Questions

After a crash, you’re bound to have questions. Here are some clear, straightforward answers to the questions we hear most often from our clients about uninsured and underinsured motorist claims in Texas.

Does My UM/UIM Coverage Pay for My Car Repairs?

That depends on the exact coverage you have. If the other driver had no insurance at all, your Uninsured Motorist Property Damage (UMPD) coverage is designed to step in and cover your vehicle repairs. But under Texas law, this specific coverage always comes with a mandatory $250 deductible.

Honestly, it's often faster and less of a headache to use your own collision coverage to get your car back on the road. If the at-fault driver was just underinsured, their policy would pay what it can first, but your collision coverage is usually the most direct path for vehicle repairs.

Will My Insurance Rates Go Up if I File a UM/UIM Claim?

No. This is a vital point every single driver in Texas needs to understand.

Texas law explicitly prohibits your own insurance company from raising your premiums or penalizing you in any way for filing a claim for uninsured and underinsured coverage when the accident was not your fault.

You are simply using a benefit you have already paid for with your premiums. You can't be punished for accessing the protection you rightfully purchased.

What if My Own Insurance Company Denies My UM/UIM Claim?

If your own insurer denies your claim without a good reason, makes a ridiculously low settlement offer, or just drags the process out forever, you need to speak with an attorney right away. These are often red flags for insurance "bad faith."

A Texas personal injury lawyer can step in and challenge the company’s unfair decision. We can take over the frustrating negotiation process to demand what you are truly owed and, if they still won't do the right thing, file a lawsuit to enforce the rights you have under the very policy you paid to protect you.

A serious accident can make you feel completely lost and overwhelmed, but you don’t have to find your way forward alone.

At The Law Office of Bryan Fagan, PLLC, our compassionate attorneys are here to give you clear answers and fight for the full compensation you deserve. We take on the legal battle so you can put all your energy into healing.

Your recovery is our priority. For a free, no-obligation consultation to discuss your case and understand your options, please contact us online or call us today.