Skip to content

Skip to content A serious accident can change your life in seconds—but you don’t have to face it alone. The physical pain is one thing, but the financial stress that follows can feel just as overwhelming. That’s where Personal Injury Protection (PIP) comes in—it’s like a financial first-aid kit built right into your Texas auto insurance policy.

What makes PIP so valuable is that it’s "no-fault" insurance. This means it gets to work right away, covering your immediate medical bills and lost wages without waiting to figure out who caused the wreck. This guide will explain how PIP works and how a compassionate Texas personal injury lawyer can help you use it to protect your family.

Your Financial First Aid Kit After a Texas Car Accident

Imagine you’re injured in a pile-up on a Houston freeway or a T-bone collision on a quiet street. The last thing you should have to worry about is how to pay for the ambulance ride or cover next month's rent. This is exactly why Personal Injury Protection (PIP) coverage is a lifeline for every Texas driver. It’s designed to provide immediate relief when you need it most.

Instead of getting stuck in a months-long battle while insurance companies investigate and point fingers, your PIP benefits kick in to help you manage essential expenses. It’s about giving you the breathing room to focus on what really matters: getting better.

To give you a clearer picture, here’s a quick summary of what PIP is all about.

PIP Coverage at a Glance

This table breaks down the core features of Personal Injury Protection and explains how it helps you right after a collision.

| Key Feature | How It Helps You After an Accident |

|---|---|

| No-Fault Coverage | Pays out quickly, regardless of who caused the crash. No waiting on blame. |

| Medical Bills | Covers immediate expenses like ambulance rides, ER visits, and doctor's appointments. |

| Lost Wages | Replaces a portion of your income if your injuries keep you from working. |

| Essential Services | Helps pay for services like childcare if your injuries prevent you from doing them yourself. |

| Funeral Expenses | Provides benefits to cover funeral costs in the event of a fatal accident. |

This coverage is designed to be your first line of financial defense, ensuring you’re not left in a lurch while waiting for a larger settlement.

What PIP Does for You Immediately

Think of PIP as the first responder for your wallet. Its whole purpose is to give you fast access to funds for your most pressing needs after an accident. This coverage steps up to handle the costs that can pile up in a hurry, including:

- Emergency room visits and ambulance rides

- 80% of your lost income if you can't work

- Follow-up doctor's appointments and physical therapy

- Prescription medications for your injuries

While PIP acts as your financial first aid, it's also smart to know what to do for physical injuries. For instance, dental trauma is common in accidents, and you'll want guidance on handling specific injuries like a knocked-out tooth.

The value of this coverage can't be overstated, especially as healthcare costs continue to climb. In fact, recent data reveals that PIP claim payouts have jumped 11% since late 2023, a direct reflection of the rising expense of post-accident medical care. Having this protection means you aren't left waiting for the other driver's insurance to finally pay up.

At The Law Office of Bryan Fagan, PLLC, our experienced Texas personal injury lawyers often help clients use their PIP benefits as the crucial first step toward securing the full and fair compensation they truly deserve.

So, What Does Your PIP Insurance Actually Cover?

When you’re laid up and trying to get better, the last thing you need is a mountain of confusing insurance paperwork. Getting a straight answer on what your personal injury protection coverage includes can be a huge relief. Think of it this way: PIP is a set of benefits you've already paid for, ready to kick in the moment you need them.

The whole point of PIP is to cover your most immediate financial needs after a crash. It lets you focus on healing without having to wait for the insurance companies to duke it out and decide who was at fault. It's your policy, for your benefit, right away.

Immediate Medical Expenses

The single most important benefit of PIP is that it starts paying your medical bills from day one. And we're not just talking about major surgery—it covers a whole range of necessary care to get you back on your feet.

For instance, after a nasty wreck on I-10 that a truck crash lawyer in Houston might handle, your PIP could immediately cover the ambulance ride, the ER visit, and any X-rays or MRIs you need. It doesn't stop there, though. It also helps with follow-up care like:

- Doctor’s appointments and visits to specialists

- Physical therapy and rehabilitation sessions

- Crucial prescription medications

- Dental work if your teeth were damaged in the accident

This immediate coverage is a game-changer. It means you get the treatment you need without delay, which can make all the difference in how well—and how quickly—you recover.

Lost Wages and Income Replacement

A serious injury almost always means time off work. But while your paycheck stops, the bills certainly don't. This is where the lost wages part of your PIP coverage becomes an absolute financial lifeline for you and your family.

Your PIP policy will typically step in to cover up to 80% of your lost income, right up to your policy's limit. This gives you a steady stream of money to handle the mortgage, groceries, and other household bills while you’re out of commission. To get this benefit rolling, you'll need a note from your doctor confirming your injuries are keeping you from doing your job. A Houston car accident attorney can be a huge help in gathering the right paperwork to make sure your claim goes through without a hitch.

Essential Services for Daily Life

Sometimes, an injury does more than just keep you from your job—it keeps you from running your own life. If a catastrophic injury leaves you unable to manage your home or care for your kids, PIP can cover the cost of what are called "essential services."

This could mean hiring someone to help with childcare, cleaning the house, or even just getting you to and from your doctor's appointments. These benefits are there to bring some stability back to your household and take a massive amount of stress off your plate, letting you pour all your energy into healing.

These three pillars—medical bills, lost wages, and essential services—are the foundation of your PIP coverage. Understanding them is the first step to making your policy work for you. If you're hitting a brick wall with your insurance company and they refuse to cover these costs, The Law Office of Bryan Fagan, PLLC, is here to fight for every dollar you're owed.

How PIP and Other Insurance Work Together

After a car wreck, the last thing you want to deal with is a confusing mess of insurance policies. Who pays for what? And when? It’s a completely valid question, and thankfully, Texas law makes the answer pretty simple.

Your Personal Injury Protection (PIP) coverage is designed to be your first line of defense. It's the policy that steps up to the plate immediately to handle your initial medical bills and cover lost wages.

This means your PIP benefits kick in right away, no matter who caused the crash. You don't have to wait around for your health insurance to approve a claim or argue with the other driver's liability carrier about who's to blame. This "first in line" approach gets you the medical care you need without delay, so you can focus on getting better.

For example, after a multi-car pileup on I-35 in Dallas, your $15,000 PIP policy can start covering your ER visit and hospital bills that very day. This gives you breathing room while our attorneys at The Law Office of Bryan Fagan, PLLC, get to work pursuing the at-fault driver's insurance for the full value of your claim.

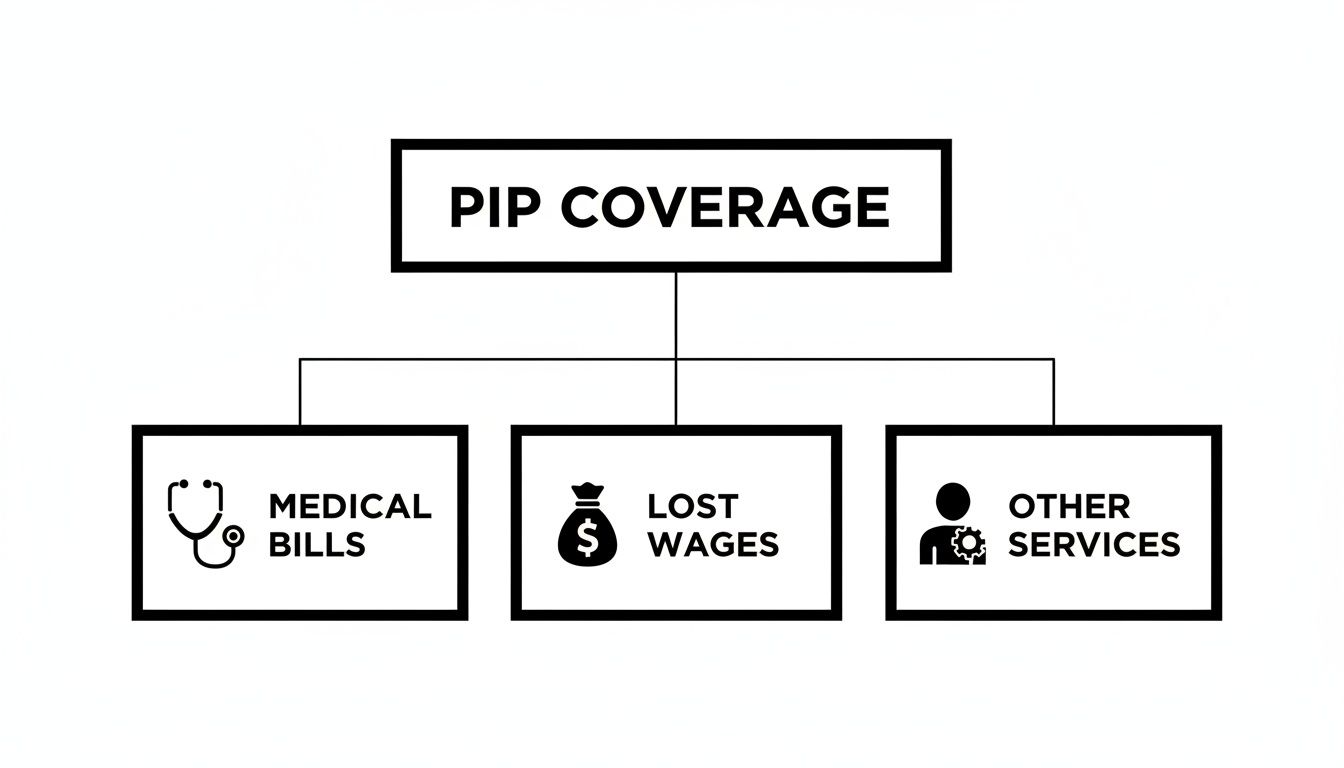

This diagram breaks down the main things your PIP policy is built to cover right after an accident.

As you can see, PIP acts as a crucial financial safety net for your most immediate needs.

What is Subrogation?

Once your PIP carrier pays for your medical treatment, they'll often use a process called subrogation. It sounds complicated, but it's really just a legal term for your insurance company's right to get its money back from the at-fault driver's insurance company down the road.

This all happens behind the scenes and actually works in your favor. It lets you get your bills paid now, while the insurance companies sort out the final financial blame later. An experienced Texas personal injury lawyer can oversee this process to make sure it doesn’t interfere with your final settlement.

PIP vs. Liability vs. Health Insurance

Think of the different insurance policies as a pecking order, designed to get you taken care of as efficiently as possible. Here’s how it works:

- Your PIP Coverage: This is your go-to policy. It pays first for all covered expenses, right up to your policy limit.

- Your Health Insurance: This can serve as a backup for medical bills that go beyond what your PIP policy covers.

- The At-Fault Driver’s Liability Insurance: This is the policy we go after to cover everything else. That includes medical costs that exceed your PIP limit, future medical care, any remaining lost wages, and your non-economic damages like pain and suffering.

But what if the other driver doesn't have enough insurance to cover your losses? It’s a scary and unfortunately common situation. That's why we also guide clients on the importance of having underinsured motorist coverage in Texas. It provides another essential layer of protection when you need it most.

The most important takeaway is this: Your PIP coverage is there to give you immediate financial breathing room. It is a no-fault benefit you paid for, and using it is the first step toward a stable recovery.

Choosing the Right Amount of PIP Coverage in Texas

In Texas, your auto insurance company is required by law to offer you Personal Injury Protection. You can say no, but you have to reject it in writing. Here at The Law Office of Bryan Fagan, PLLC, we believe that is a mistake. Declining PIP is like throwing a life jacket overboard before setting sail—it’s a risk you just don't need to take, and one that could leave your family in a financial hole after a crash.

Think of PIP as your first line of financial defense after a wreck. It’s designed to cover 80% of your medical bills and 80% of your lost wages, no matter who was at fault for the accident. In 2023 alone, a staggering 222,698 people died from preventable injuries in the U.S., and millions more needed medical care. Those numbers aren't just statistics; they're a stark reminder of why having a financial safety net is so important. Without enough PIP, many families are left completely exposed. You can learn more about insurance trends and their broader impact to see the full picture.

Why the State Minimum Is Not Enough

The minimum PIP coverage Texas requires insurers to offer is just $2,500. That might sound like a decent amount, but the truth is, medical bills from even a minor car accident can blow past that number in a hurry. A single trip to the emergency room can wipe it out completely.

Let’s imagine a common scenario: you get rear-ended on a Houston freeway. You walk away with whiplash and a mild concussion. Your immediate costs could easily look like this:

- Ambulance Ride: $800 – $2,000+

- Emergency Room Visit: $1,500 – $3,000+

- Diagnostic Scans (X-ray/CT): $500 – $2,500+

Suddenly, that $2,500 minimum is gone before you've even thought about follow-up doctor visits or physical therapy. That's why it's so critical to see the minimum as a starting point, not a realistic safety net for your family's finances.

Choosing higher PIP limits is one of the smartest and most affordable investments you can make in your car insurance. It gives you immediate access to money when you need it most, so your recovery doesn't get put on hold because of financial stress.

Investing in Higher Limits for Your Security

It’s much smarter to opt for higher PIP limits—like $10,000, $25,000, or even more. This gives you a much stronger cushion against the crushing costs of an unexpected injury. The extra cost on your premium is usually small, but the peace of mind it buys is priceless.

Higher limits mean you have the funds to cover your initial medical care, replace a bigger chunk of your lost paychecks, and handle your daily bills while you focus on getting better.

If you’re not sure what your policy covers or you're stuck trying to get a claim paid, a Texas personal injury lawyer can cut through the confusion. We can review your policy, explain what you’re entitled to, and lay out your options. Making a smart choice now can save your family from serious financial trouble down the road. A free consultation with our team can give you the clarity you need to protect your future.

How to File Your PIP Claim in Texas

When you’re already reeling from the stress and pain of an accident, the thought of filing an insurance claim can feel completely overwhelming. But knowing the right moves to make can smooth out the process, ensuring you get the benefits you're entitled to without frustrating delays. Think of this as your roadmap to tapping into your Personal Injury Protection (PIP) coverage.

On Texas highways, whether it's a packed San Antonio freeway or a quiet rural road outside Houston, personal injury protection (PIP) coverage is the tool that gets your bills paid first. It lets you sidestep the initial back-and-forth over who was at fault. In fact, paid outcomes for injured victims have jumped 11% since late 2023, which really shines a light on the rising costs of accidents and why filing promptly is so critical. For more on insurance market trends, you can read the full data report from the NAIC.

Your Action Plan After an Accident

Following a clear game plan is the absolute best way to protect your rights and get your claim started on solid ground. Even small mistakes can lead to denials, but a structured approach helps you dodge those common pitfalls.

- Seek Immediate Medical Attention: Your health is everything. Head to the ER or see a doctor right away, even if you think you feel okay. This creates a medical record that directly connects your injuries to the accident.

- Report the Accident and Get a Police Report: Always, always call the police to the scene. That official police report is a vital piece of evidence that locks in the facts of the crash.

- Notify Your Own Insurance Company Promptly: Don't put this off. Call your insurer as soon as you can to report what happened and start the process of filing your claim. Insurance policies have strict deadlines, and missing one could jeopardize your entire claim.

- Keep Detailed Records of Everything: Start a file—physical or digital—and hang on to everything related to the accident. We're talking medical bills, prescription receipts, photos of the scene and your injuries, and even notes about how the injury is impacting your day-to-day life.

- Submit Your Claim Forms Accurately: Fill out every insurance form completely and honestly. Be precise when describing your injuries and how the crash happened.

Trying to navigate the claims process on your own can be a real headache. An experienced Texas personal injury lawyer can handle all these details for you, making sure every form is filed correctly and every deadline is met. That leaves you free to focus on what truly matters: your recovery.

If you’ve been injured and you’re not sure what to do next, you don’t have to figure it out alone. The Law Office of Bryan Fagan, PLLC, is here to help. Contact us for a free consultation to discuss your rights and get the clear, compassionate guidance you deserve.

When to File a Lawsuit if PIP Is Not Enough

Your Personal Injury Protection (PIP) coverage is a crucial first line of defense after a crash, but it's important to understand its limitations. It's not a blank check. Think of it like a first-aid kit for your immediate financial injuries.

In the aftermath of a severe accident, like a catastrophic injury from a truck wreck or other serious collision, the costs can spiral far beyond a typical PIP policy maximum of $10,000 or $25,000. PIP was designed to handle initial needs, not the full financial fallout.

When Your Damages Exceed Your Policy

The most clear-cut reason to consider legal action is when your expenses simply overwhelm your PIP benefits. It’s a matter of simple math.

If you need extensive surgery, long-term physical therapy, or ongoing medical care, your bills can blow past your policy’s cap in a heartbeat. At that point, your focus must shift from your own insurance to holding the at-fault party accountable for the rest.

Beyond the numbers, PIP only covers economic damages—things with a clear price tag, like doctor's bills and lost paychecks. It provides absolutely zero compensation for non-economic damages, which include:

- Physical pain and suffering

- Emotional distress and mental anguish

- Loss of enjoyment of life

- Permanent disfigurement or disability

Often, these non-economic losses represent the most significant part of a serious injury claim. The only way to recover them is by going after the negligent driver’s insurance.

How Long Do You Have to File a Claim in Texas?

If your injuries are severe, the other driver’s insurance company is giving you the runaround, or your costs have already shot past your PIP limit, it’s time to talk to a Texas personal injury lawyer.

Texas law is unforgiving when it comes to deadlines. You have a limited window to file a lawsuit, and understanding the statute of limitations for a Texas car accident is critical to protecting your rights. Miss that deadline, and you lose your chance to get compensation forever.

A personal injury lawsuit isn’t about replacing PIP; it’s about pursuing the full and fair compensation you need to truly rebuild your life. This is where we step in to fight for every dollar you deserve.

Don't wait until you're buried under a mountain of bills and stress. A free consultation with the experienced attorneys at The Law Office of Bryan Fagan, PLLC, can give you the clarity and direction you need. We are here to make sure you don’t have to face this fight alone.

Still Have Questions About PIP? Here Are Some Common Ones

After a car wreck, your head is probably swimming with questions. It's completely normal to feel overwhelmed and unsure about what to do next. Let’s clear up some of the most common concerns we hear from people just like you about Personal Injury Protection coverage here in Texas.

Can I Still Use PIP if the Accident Was My Fault?

Yes, you absolutely can. This is the single biggest advantage of having PIP coverage in the first place.

Because it’s “no-fault” insurance, it’s there for you no matter who caused the crash. PIP kicks in to cover your medical bills and a chunk of your lost wages, giving you critical financial breathing room while everyone else figures out who was legally responsible for the collision.

Will Filing a PIP Claim Make My Insurance Rates Go Up?

This is a huge worry for a lot of people, but Texas law offers some protection. Insurance companies are generally not allowed to jack up your rates for a single claim where you weren’t the one at fault.

Think of it this way: PIP is a benefit you've already paid for through your premiums. If your insurer tries to bully you or threatens a rate hike after a not-at-fault accident, that’s a massive red flag. It’s the perfect time to get an experienced Houston car accident attorney in your corner to protect your rights.

What Happens if the Other Driver Is Uninsured?

This is exactly the kind of nightmare scenario where PIP coverage becomes a true lifesaver. It acts as your first line of defense, providing immediate funds for your medical care and lost income.

It’s also why having Uninsured/Underinsured Motorist (UM/UIM) coverage is so critical. Once you’ve used up your PIP benefits, your UM/UIM policy can step in to cover the rest of your damages. Our team helps clients navigate both of these claims all the time.

While you can certainly file a PIP claim on your own, talking to a personal injury lawyer is always a smart move, especially if you’ve been seriously hurt. An attorney makes sure your claim is filed correctly, you don’t miss any crucial deadlines, and the insurance company treats you fairly from day one.

A free consultation can give you immediate peace of mind and get your recovery started on the right foot.

A serious accident can change your life in seconds—but you don’t have to face the aftermath alone. Recovery is possible, and legal help is available. The experienced team at The Law Office of Bryan Fagan, PLLC is here to provide the compassionate support and aggressive advocacy you need. Schedule your free, no-obligation consultation today by visiting https://texaspersonalinjury.net or calling us.