A serious accident can change your life in seconds — but you don’t have to face it alone. At The Law Office of Bryan Fagan, PLLC, we guide you with clarity, compassion, and experience so you know your rights and next steps.

Average Settlement Figures In Texas

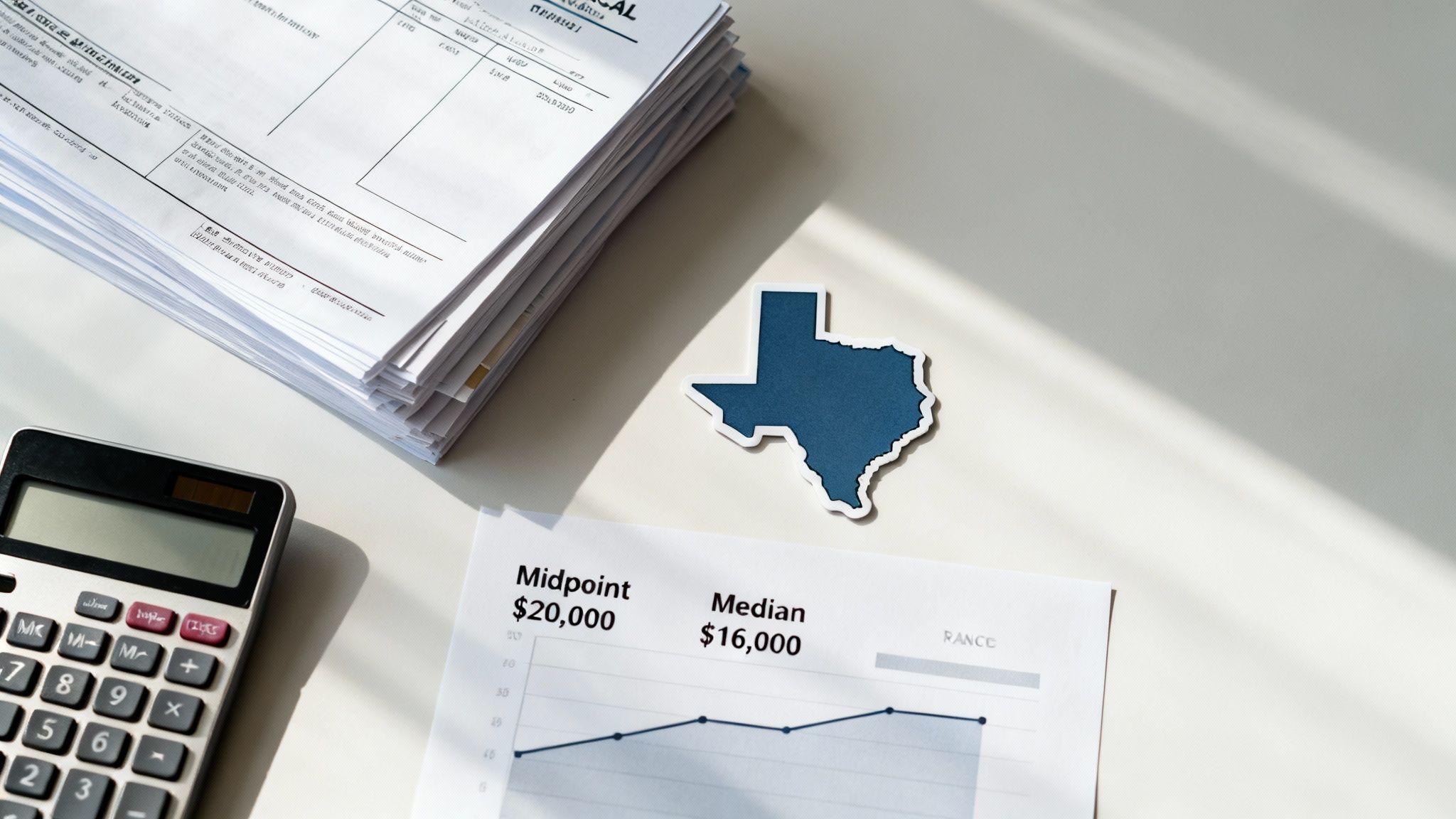

If you’re wondering what a typical car accident payout looks like in Texas, the numbers offer a helpful starting point. On average, claimants see about $22,700, while the median award lands near $16,000. Your own settlement may be higher or lower depending on your unique situation.

Under Texas personal injury law, fault and negligence rules play a crucial role in setting these averages. Below are the core benchmarks for Texas car accident settlements:

- Industry data puts the average bodily injury settlement in Texas in the low-to-mid $20,000s, often pegged at $22,734. That figure blends everything from minor soft-tissue cases to multi-million-dollar verdicts. For a deep dive, check out the Texas car accident settlement data from ULG Law.

- The median settlement in Texas sits at around $16,000, showing what most claimants actually receive.

- Fender-benders with minimal injuries frequently resolve for under $5,000, while catastrophic crashes can push awards over $1,000,000.

- Key drivers of these outcomes include medical bills, lost wages, pain and suffering, and insurance policy limits.

Summary Of Average And Median Settlements

Below is a concise look at the primary settlement metrics for Texas car accident cases.

| Metric | Amount |

|---|---|

| Average Settlement | $22,734 |

| Median Settlement | $16,000 |

| Low-End Range | <$5,000 |

| High-End Range | >$1,000,000 |

The image above maps out common crash types and injury patterns. It illustrates how impact level and collision style can influence the severity of harm—and ultimately, the size of your claim.

Understanding Reported Settlement Averages

Average and median figures each tell a different story:

- The average often skews upward because a handful of high-value cases pull the mean higher.

- The median sits at the midpoint, so half of all settlements fall above and half below that number.

- Insurers sometimes lean on the mean to set expectations, but the median generally reflects what most people actually see in their bank accounts.

Grasping this distinction helps you gauge whether a settlement offer aligns with real-world outcomes.

Case Factors That Shift Benchmarks

Every claim carries its own unique mix of variables. Here are the most influential:

- Liability: A clear assignment of fault tends to generate stronger opening offers.

- Severity: Broken bones, surgeries, or long-term care needs drive economic damages higher.

- Insurance Limits: The at-fault driver’s policy cap can limit your recovery, regardless of actual losses.

- Comparative Responsibility: Texas follows a modified comparative negligence rule—any percentage of fault you share can directly reduce your award.

Understanding how these pieces fit together will help you set realistic goals and build a strategy for pursuing fair compensation.

How Settlements Are Calculated In Texas

A serious accident can turn your world upside down in an instant. Understanding how Texas law puts a dollar amount on your losses helps you plan ahead and set realistic expectations for your car accident settlement.

Settlements in Texas blend economic damages—like hospital bills and lost wages—with non-economic damages such as pain, suffering, and emotional distress. Insurance adjusters break each claim into categories, factor in Texas’s comparative negligence rules, then apply policy limits.

- Medical Expenses: Emergency room charges, surgeries, physical therapy and future care

- Lost Income: Paychecks, bonuses and any reduction in earning capacity

- Property Damage: Repairs or replacement costs for your vehicle and personal belongings

- Pain & Suffering: The physical and psychological toll following a crash

Texas follows a modified comparative negligence system. If you bear 51% or more fault, you can’t recover any damages. Otherwise, adjusters subtract your percentage of blame from the total damages to land on a final offer.

Keep detailed records of your injuries, bills and any evidence pointing to the other driver’s fault. That documentation can stop unfair percentage cuts in their tracks.

You also have just two years under Texas’s statute of limitations to file a lawsuit or risk losing your rights. And remember, even if a jury awards more, insurance policy limits often cap what you actually collect. For instance, if the at-fault driver’s bodily injury limit is $30,000, that’s the most you’ll see—no matter how steep your bills climb.

Economic Damages Explained

Economic damages are the out-of-pocket costs you can prove with bills, pay stubs and invoices. Adjusters add up:

| Damages Type | Examples |

|---|---|

| Medical Bills | ER visits, surgeries, therapy |

| Lost Wages | Salary, benefits, overtime pay |

| Future Care | Home modifications, assistive devices |

After a Houston freeway crash that left someone with a spinal injury, past hospital bills might total $50,000, and projected nursing care and mobility aids can send future costs into six figures.

Non-Economic Damages And Multipliers

Non-economic damages cover pain, emotional trauma and loss of life’s pleasures. Texas doesn’t cap these in most auto cases, but adjusters often use a multiplier to arrive at a fair figure.

- Tally your total economic damages.

- Select a multiplier—usually 1.5x to 5x—based on how serious the injuries are.

- Multiply the economic sum by that factor.

- Add the result to your demand for pain and suffering.

Insurance caps apply separately to each category, so a generous multiplier won’t help if you hit the policy limit.

A seasoned Texas personal injury lawyer can argue for a higher multiplier and push back against lowball offers.

Check out our guide on how to calculate car accident settlements in Texas for a step-by-step walkthrough.

Policy Limits And Negotiation Impact

Every insurance policy has a ceiling. When at-fault drivers carry only minimum coverage, you may hit that ceiling fast. In those cases, consider:

- Underinsured Motorist Coverage: Your own policy may step in

- Additional Parties: Exploring other liable defendants

- Demand Letters: Laying out both economic and non-economic demands

- Mediation: A neutral mediator can bridge gaps outside court

- Pre-Suit Negotiations: Your attorney meets insurer reps face-to-face

- Filing Suit: If talks stall, moving toward trial to seek the full amount

Insurers often sweeten their offers once they realize you’re ready to go before a jury.

Why Legal Guidance Matters

A practiced Texas personal injury lawyer knows how to document every facet of your claim and counter common insurer tactics. They:

- Gather and organize medical records

- Quantify your pain and suffering with supporting evidence

- Watch deadlines like a hawk to keep your case alive

- Negotiate or litigate on your behalf, so you focus on healing

For catastrophic or family loss cases, our wrongful death lawyer Texas and truck crash lawyer Houston teams are ready to help.

Our team at The Law Office of Bryan Fagan, PLLC fights tirelessly for maximum compensation and stands by you.

Every dollar you’ve spent, every moment of pain—Texas law recognizes it. With a clear grasp of settlement calculations, you can approach negotiations confidently and protect the full value of your claim. Schedule your free consultation today and let us handle the rest.

Key Factors That Affect Settlement Values

Every Texas car accident claim is like a puzzle with many pieces. Your total recovery depends on how each piece—medical evidence, liability proof, insurance limits—fits together. Knowing what drives up a settlement and what drags it down gives you a real edge.

Medical Documentation And Evidence

Your medical records are the foundation of any strong claim. Insurers want a clear timeline: ER visits, follow-ups, rehab notes. Gaps or inconsistencies almost always lead to reduced offers.

- Itemized hospital invoices showing emergency care

- Attending physician letters outlining long-term effects

- Expert opinions from medical specialists

When your medical evidence is airtight, you gain real bargaining power.

Imagine you’re in a Houston freeway wreck and liability is in dispute. Detailed MRI findings and daily pain logs can push an initial $15,000 offer past $45,000.

Injury Severity And Personal Factors

How badly you’re hurt—and who you are—matters. A soft-tissue injury might land around $5,000, while complex fractures can top $100,000. Your age, occupation and lifestyle shifts all feed into the final calculation.

- Young professionals with decades of earning ahead often see higher awards

- Manual-labor workers facing permanent restrictions can claim future wage loss

- Pre-existing conditions must be untangled by medical testimony

Think of building your case like stacking Lego blocks—each piece of proof adds height to your total value.

Liability And Comparative Fault

Texas follows a modified comparative negligence rule: if you’re over 51% at fault, you recover nothing. Even a small fault percentage reduces what you get.

- Pin down the other driver’s responsibility with crash reports

- Gather witness statements and expert reconstructions

- Dispute unreasonable fault percentages with hard evidence

Accurate fault assignment can swing your settlement dramatically.

| Factor | Impact on Settlement |

|---|---|

| Clear Fault Evidence | Raises potential by 10–30% |

| Extensive Medical Costs | Justifies higher pain and suffering |

| Insurance Policy Limits | Caps the maximum payout |

Insurance Coverage And Attorney Involvement

Every Texas driver must carry at least $30,000 per person. If that cap is too low, your lawyer can explore uninsured/underinsured motorist coverage or other liable parties.

Hiring an attorney often boosts settlements by 30% or more. A seasoned lawyer will:

- Negotiate aggressively with insurers

- Handle all claim paperwork and deadlines

- Present pain-and-suffering multipliers clearly

- Represent you in catastrophic injury and wrongful death cases

Key Steps To Involve Your Attorney Early

- Contact a Texas personal injury lawyer within days to lock in evidence

- Let your attorney manage insurer communications and recorded statements

- Tap into your lawyer’s network for medical and reconstruction experts

For a deeper dive on valuing non-economic losses, check out our guide on how to prove pain and suffering.

Additional Settlement Influencers

- Age and overall health shape non-economic damage awards

- Occupation and future earning potential drive lost-wage claims

- Pre-existing conditions require clear medical testimony to separate old from new

- Emotional distress and lifestyle impacts carry real monetary weight

Piecing together solid documentation, clear liability, and strong legal advocacy paints the clearest picture for insurers. Ready to build your strongest claim? Schedule a free consultation with our Texas personal injury team today—and let’s demand the compensation you deserve.

Settlement Ranges By Injury Severity

In Texas, knowing how courts and insurers view different injury levels can save you from guessing games. By examining actual verdicts and settlements, you’ll see clear patterns from minor strains to life-altering harm.

Minor soft-tissue injuries, like whiplash, typically settle between $2,500–$30,000.

Moderate injuries, such as fractures or herniated discs, usually fall into the $50,000–$250,000 bracket.

When you’re dealing with catastrophic injuries or wrongful-death claims, figures often climb past $1,000,000, thanks to long-term care costs and emotional damages.

For a deeper dive, read the full insights on average car accident settlements.

Settlement Bands By Injury Type

Here’s a side-by-side comparison of injury severity, typical settlement ranges, and how long each case usually takes to wrap up.

| Injury Category | Settlement Range | Usual Timeline |

|---|---|---|

| Minor Soft-Tissue | $2,500–$30,000 | 3–6 months |

| Moderate Fractures | $50,000–$250,000 | 6–12 months |

| Severe Catastrophic | Exceeding $1,000,000 | 1–3 years |

Factors That Influence Each Band

Minor injuries hinge on clear medical notes and follow-up visits. Without solid records, insurers push lower offers.

Moderate injuries demand imaging tests and therapy logs. These documents prove you’re still recovering and deserve fair compensation.

Catastrophic cases rely on expert opinions—life-care plans, vocational assessments, and specialized testimony.

Strong documentation and specialist reports can boost your settlement by 20–40%.

Typical Timelines By Case Complexity

Knowing the clock can ease stress. Here’s what you might face:

- Simple soft-tissue claims often settle in 3–6 months.

- Moderate injury negotiations usually take 6–12 months.

- High-value or wrongful-death cases can stretch 1–3 years.

Planning ahead means you won’t be caught off guard by delays.

These pillars—duty, breach, causation, and damages—form the backbone of any strong claim.

Real World Example Of Settlement Bands

Imagine a Houston freeway collision that left a driver with a herniated disc. Medical bills hit $40,000 and lost wages added $15,000. With a 2× pain-and-suffering multiplier, the demand climbed to about $110,000. Thanks to clear fault and thorough records, the case closed at $100,000 in eight months.

On the flip side, a San Antonio brain-injury lawsuit involved a six-figure life-care plan and expert testimony. Negotiations took two years, but ultimately surpassed $1,200,000.

Best Practices To Strengthen Your Case

- Document Everything: Take clear photos of the scene and your injuries. Keep a daily journal tracking pain levels and treatments.

- Seek Prompt Medical Care: Early treatment links your injuries directly to the accident. Follow every doctor’s order to avoid insurer pushback.

- Consult A Texas Personal Injury Lawyer Early: An experienced attorney handles paperwork, talks to insurers, and builds your evidence so you can focus on healing.

Armed with these settlement ranges and timelines, you’ll be ready to map out your path to recovery and fair compensation.

Claims Timeline And Resolution Options

Once you file your claim, timing and tactics set the pace. Picture it as a relay race: each stage hands off to the next, and your claim only wins if every runner sticks their landing.

You’ll move through:

- Initial Demand: Your attorney drafts a letter detailing injuries, bills, and losses.

- Insurer Investigation: Adjusters dig into medical records, police reports, and fault issues.

- Negotiation Phase: Offers and counteroffers fly until someone blinks.

- Mediation/Arbitration: A neutral third party helps bridge gaps—or hands down a decision.

- Filing Suit: If talks stall, you file before Texas’s 2-year statute of limitations to keep your rights alive.

Understanding Each Stage

The first letter your lawyer sends is more than a demand—it sets expectations. It packages all your evidence: medical bills, pay stubs, and pain journals.

Next comes the insurer’s fact-finding mission. This can take weeks or stretch into months if surgeries or expert opinions are involved. Don’t be surprised if adjusters ask for recorded statements or additional reports.

Many soft-tissue claims wrap up in 3–6 months once fault is clear and injuries are straightforward.

When the insurer’s homework is done, negotiation begins. You’ll see back-and-forth offers until both sides land on a number—or decide to pause talks.

If you hit a stalemate, mediation offers a structured forum. It’s private and usually costs less than court. Arbitration can be faster, but the arbitrator’s decision is typically binding.

Resolution Timeline Overview

| Stage | Typical Duration |

|---|---|

| Initial Demand | 1–2 months |

| Insurer Investigation | 2–6 months |

| Negotiation | 1–3 months |

| Mediation/Arbitration | 1–2 months |

| Trial and Appeal | 1–2 years |

When To File A Lawsuit

Deciding to sue is like calling “all in.” It signals you’re serious and often reboots stalled talks. In Texas, you’ve got two years from the accident date to file suit.

Once you file, formal discovery kicks off: depositions, expert disclosures, and court deadlines. High-stakes or disputed cases often take 1–3 years to reach trial.

Key elements in this phase:

- Structured Settlement Offers: Spread payments over time.

- Arbitration Clauses: Some contracts send you to private hearings.

- Alternative Dispute Resolution: Early neutral evaluation can jump-start settlements.

- Trial Preparation: Expert testimonies, final pleadings, and exhibit binders.

Alternative Resolution Methods

Not every case ends in a jury trial. Here’s a quick rundown:

- Structured Settlements secure long-term payments for future care.

- Arbitration moves faster but limits your appeal options.

- Mediation blends negotiation with neutral facilitation.

Best Practices:

- Review any arbitration clause before signing.

- Weigh structured settlement pros and cons for cash flow.

- Lean on your lawyer for expert witness coordination.

- Watch hidden deadlines, like mediation or arbitration windows.

Next Steps For Your Claim

Stay organized. Track every bill, email, and meeting. Keep a calendar for critical deadlines—especially filing suit or starting arbitration.

Partner closely with your attorney. As your case evolves, so should your strategy.

For a deeper dive into timelines and tactics, check out our guide on How Long It Takes to Settle a Car Accident Claim.

Whether your collision is a minor fender-bender or a major wreck, a clear roadmap keeps you proactive, avoids surprises, and protects your claim’s value. At The Law Office of Bryan Fagan, PLLC, we’ll walk beside you every step of the way—offering both expertise and empathy.

Contact our Houston car accident attorney today to schedule a free consultation. Recovery is within reach, and you don’t have to go it alone.

Practical Steps After a Texas Car Accident

A serious accident can upend your life in a blink. But you don’t have to face the chaos alone. The moments after a collision matter for both your health and your claim.

First, call 911 if anyone is hurt or the damage is extensive. Then:

- Get out of harm’s way before doing anything else.

- Move vehicles to the shoulder if it’s safe; note any skid marks or broken glass.

- Swap names, phone numbers, and insurance details with the other driver and witnesses.

- Snap clear photos of the scene, the vehicles, and your injuries.

“Immediate evidence preserves your best odds,” says Bryan Fagan.

Collecting proof on the spot lays a solid foundation for talking about average car accident settlement Texas. Think of your pictures and notes as puzzle pieces showing insurers exactly what happened.

In one Houston intersection crash, a client’s quick medical check and thorough photo record boosted their final offer by 50%.

Choosing The Right Representation

Facing an insurance adjuster alone can feel like walking a tightrope. One careless answer, one recorded statement, and you could lose up to 30% of your settlement.

That’s when you call a seasoned Texas personal injury lawyer. At The Law Office of Bryan Fagan, PLLC, we take calls from insurers so you can focus on healing.

- When injuries demand surgeries or long-term therapy

- If liability is disputed or the facts are complex

- For expert guidance on adjuster tactics

- To explore representation in car, truck, wrongful death, or catastrophic injury cases

Your attorney gathers medical records, police reports, and witness statements—creating a clear paper trail and powerful negotiating position.

Notifying Your Insurer Correctly

Texas law requires you to report most crashes to your insurer within 24 hours. That quick step locks in your coverage and safeguards your benefits.

- Call your insurer with basic facts; never admit fault.

- Provide your policy number and the date of the accident.

- Explain that you’re seeking medical treatment and will forward bills later.

Tuck every claim number and adjuster name into a dedicated accident folder. Journal your symptoms daily—insurers often look for signs you’ve bounced back before cutting checks.

These simple habits can improve your average car accident settlement Texas by highlighting consistent medical care.

Documenting Injuries And Treatment

Take snapshots of every bruise, cut, or swelling you see. Then:

- Keep a daily pain and symptom log with dates

- Record medication dosages and any side effects

- Save physical therapy notes and receipts

This meticulous record-keeping becomes the backbone of your settlement talks.

Next Steps To Strengthen Your Claim

- Continue medical follow-ups until your doctor clears you

- Steer clear of social media posts about your case

When you’re ready, contact our Houston car accident attorney for a free consultation. Recovery is possible, and your rights are our priority.

FAQ On Average Car Accident Settlement Texas

You probably have a lot of questions about how much a typical car accident claim might be worth in Texas—and what really moves the needle on your payout. Below, we unpack the key points in plain English.

How Fault Is Determined In Texas

Texas uses a modified comparative negligence rule. If you’re found 51% (or more) at fault, you can’t recover anything. Otherwise, the court or insurers slice up the responsibility and adjust your recovery based on your share of blame.

What Comparative Negligence Means For Your Settlement

Put simply: if you’re partly to blame, your award shrinks by that percentage. For example, a 20% fault finding on a $20,000 demand drops your final check to $16,000.

Key Insight: Pinpointing fault accurately—through police reports, witness statements, and expert analysis—can boost your settlement.

When To Call A Houston Car Accident Attorney

Don’t wait. Reach out to a seasoned Houston car accident attorney within days of the crash. Early involvement can:

- Shield you from surprise lowball offers

- Preserve critical evidence (think photos, medical records)

- Increase settlement value by 30% or more

An attorney handles the insurance dance, so you can focus on healing.

How Insurers Calculate Your Offer

Insurers typically start by adding up your economic damages—medical bills, repair costs, lost wages—and then tack on a pain & suffering multiplier, usually between 1.5x and 5x. Next, they factor in:

- Policy limits

- Any shared fault under comparative negligence

That final cap often dictates the top end of your payout.

Before Settlement Talks

- Review every medical bill and wage statement.

- Draft a clear, organized demand letter with supporting docs.

- Double-check your underinsured motorist (UIM) coverage if the at-fault driver’s policy is minimal.

| Settlement Metric | Amount |

|---|---|

| Average Award | $22,734 |

| Median Award | $16,000 |

| Low-End Range | <$5,000 |

What If An Insurer Makes A Low Offer?

Never sign on the dotted line with the first number they throw at you. Instead:

- Gather all evidence—doctor notes, pay stubs, repair estimates

- Push back with a counter-offer and a solid demand package

- File a complaint with the Texas Department of Insurance if needed

- Consider filing suit before the two-year statute of limitations expires

Every case is different, so it pays to have an attorney guide you.

If you don’t see your question here, let’s talk. Our teams handling Houston truck crash, wrongful death, and catastrophic injury cases are standing by.

Reach out to The Law Office of Bryan Fagan, PLLC for a free consultation at TexasPersonalInjury.net. Recovery is possible, and legal help is available every step of the way.