A serious accident can change your life in seconds—but you don’t have to face it alone. After a car crash in Texas, one of the first and most stressful worries is how to handle the flood of medical bills. A common question we hear is, "Does my health insurance cover car accident injuries?" The short answer is yes, you absolutely can and should use your health insurance for immediate medical care. But thinking that's the end of the story is a common—and often very expensive—mistake.

When you're hurt and overwhelmed, you need clear answers and a team you can trust. At The Law Office of Bryan Fagan, PLLC, our goal is to provide the support and legal guidance you need to protect your family and begin the road to recovery.

Your Health Insurance Is a Bridge, Not a Destination

A serious crash can turn your world upside down in an instant. Your first priority has to be getting the medical care you need to start healing. Using your health insurance is the quickest way to make sure doctors, hospitals, and specialists get paid on time. This keeps your bills from going to collections and protects your credit score while the details of the accident claim are sorted out.

Think of your health insurance as a crucial first-aid kit. It's there to stop the immediate financial bleeding by covering your initial hospital stay, surgeries, and follow-up doctor visits. But it was never designed to make you whole again after someone else's negligence causes you harm.

What Your Health Plan Misses

Your health insurance policy is a contract between you and your provider. It agrees to cover certain approved medical treatments, but you're still on the hook for deductibles, co-pays, and out-of-network costs. More importantly, it does absolutely nothing to address the full, devastating impact a serious collision has on your life.

A personal injury claim, on the other hand, is designed to recover compensation for all of your losses, including:

- Economic Damages: These are the real, measurable financial hits you've taken. This includes every single medical bill (both past and future), lost wages from being unable to work, and even the loss of future earning capacity if your injuries prevent you from returning to your job.

- Non-Economic Damages: This category covers the immense personal toll the accident has taken on you. It includes your physical pain, emotional distress, mental anguish, and the loss of enjoyment of life.

For example, after a Houston freeway crash, your health plan might pay for the emergency surgery you needed. But it won't pay your mortgage while you're out of work recovering. It won't compensate you for the chronic back pain you now have to live with every single day. Only a personal injury claim can fight for the full compensation that addresses your complete story of loss and recovery.

To put it simply, here’s a breakdown of what your health plan handles versus what a personal injury claim is designed to cover.

Health Insurance vs. Personal Injury Claim: What Each Covers

This table provides a quick, at-a-glance comparison of what your health insurance takes care of versus the comprehensive compensation you can pursue through a car accident claim.

| Type of Damage | Covered by Health Insurance | Covered by a Personal Injury Claim |

|---|---|---|

| Emergency Room Bills | Yes (after deductible/copay) | Yes (full amount) |

| Surgery Costs | Yes (after deductible/copay) | Yes (full amount) |

| Future Medical Care | No (only covers current needs) | Yes (estimated future costs) |

| Lost Wages | No | Yes |

| Diminished Earning Capacity | No | Yes |

| Pain and Suffering | No | Yes |

| Emotional Distress | No | Yes |

| Vehicle Repair/Replacement | No | Yes (property damage claim) |

As you can see, health insurance plays a vital role in getting you immediate care, but it leaves massive gaps in your financial recovery. A personal injury claim is the only way to bridge that gap and hold the at-fault driver accountable for the full scope of the damage they caused.

Relying solely on your health insurance after an accident is like accepting payment for a totaled car but not for the injuries you sustained inside it. It addresses only a fraction of the total harm.

Understanding the difference between what your health insurance pays and what you are legally owed is the first step toward protecting your family’s future. To learn more, our detailed guide explains who pays medical bills after a car accident. A personal injury claim is the legal path to holding the at-fault party accountable and securing the resources you need to truly rebuild. You deserve a legal advocate who will fight for every dollar you need to move forward.

Who Pays First? Understanding the Insurance Pecking Order

After a crash, it's completely normal to feel buried under a mountain of medical bills and confusing letters from insurance companies. One of the biggest headaches is figuring out which insurance policy is supposed to pay for your medical care and when.

Think of it like a relay race. Different insurance policies are responsible for different legs of your recovery journey, and knowing the order is the key to getting through it without financial hiccups.

In Texas, the sequence of payment—what we call the "pecking order"—is set up to get your doctors paid quickly while everyone figures out who was at fault for the accident. This system is crucial because it ensures you don't have to wait for a settlement to get the treatment you need.

It might seem backward, but the process almost always starts with your own insurance policies, even if the other driver was clearly at fault.

Your Own Auto Insurance Is the First Responder

The very first place to turn for medical bill payment is often your own car insurance policy. Two specific types of coverage act as your first line of defense:

- Personal Injury Protection (PIP): In Texas, every auto insurance policy is required to include PIP coverage unless you specifically reject it in writing. This is no-fault coverage, which means it pays for your medical bills and a portion of lost wages up to your policy limit, no matter who caused the crash.

- Medical Payments Coverage (MedPay): MedPay is similar to PIP. It’s optional, no-fault coverage that helps with medical expenses. The main difference is that it doesn't cover lost wages.

Using your PIP or MedPay first is a huge advantage. It provides immediate cash to cover those initial ER visits, ambulance rides, and other urgent costs, keeping them from hitting your bank account. We have a detailed guide that explains the benefits of Personal Injury Protection coverage.

Your Health Insurance Steps In Next

Once your PIP or MedPay runs out, your health insurance is next in line to take the baton. It will start covering your ongoing medical care, like surgeries, physical therapy sessions, and appointments with specialists.

You'll still have to cover your usual deductibles and co-pays, just like you would for any other medical issue.

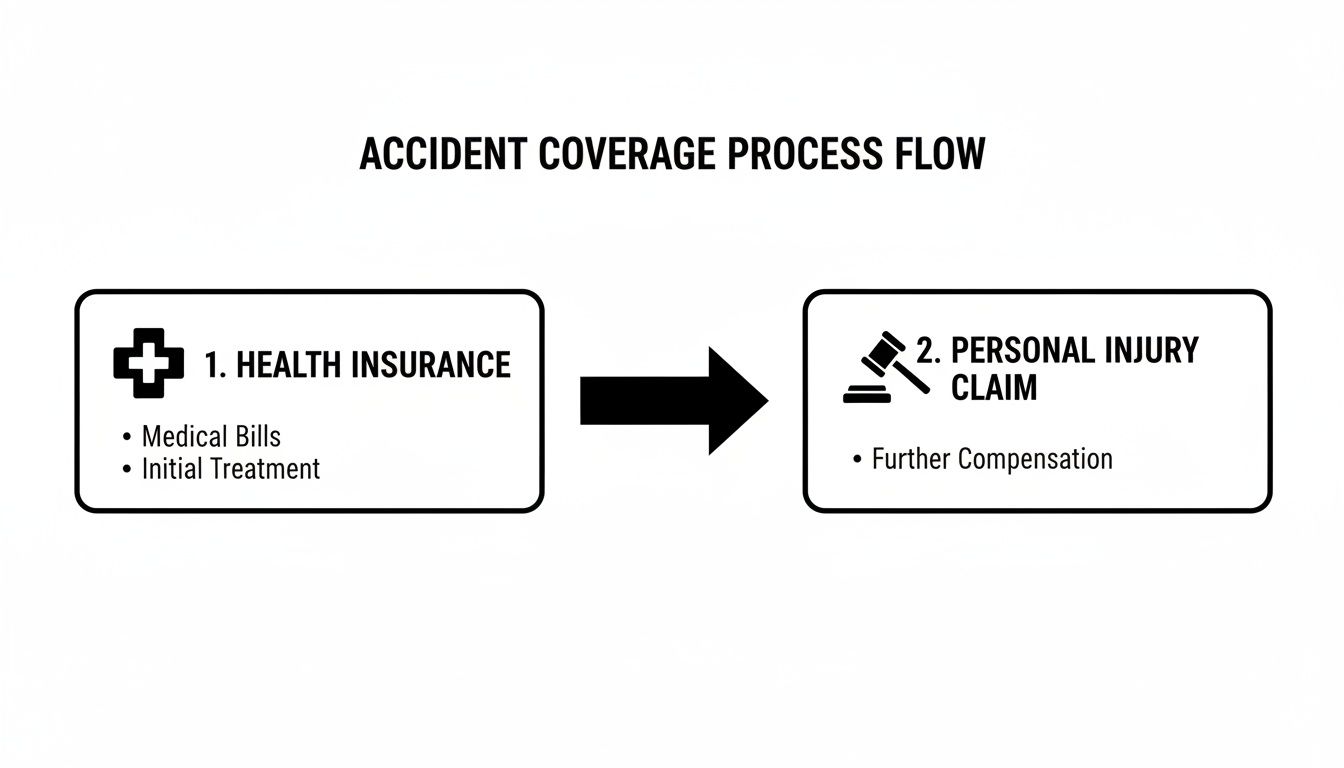

This chart shows the typical flow of how accident coverage works, from the immediate aftermath to your final personal injury claim.

As you can see, your health insurance acts as a critical financial bridge. It allows you to keep getting treatment while your personal injury lawyer builds your case against the at-fault driver. To really get a handle on the "insurance pecking order," it helps to have a good understanding prior authorization in healthcare, since that process can sometimes delay approvals for necessary treatments.

The At-Fault Driver’s Insurance Is Ultimately Responsible

The final runner in this relay race is the at-fault driver's auto liability insurance. This is the policy that is ultimately on the hook for all your damages—not just the medical bills. Under Texas law, the person who caused the accident through their negligence is financially responsible for the harm they caused.

While your PIP and health insurance paid your doctors along the way, the at-fault driver's insurance is responsible for paying them back and covering everything else you've lost.

A personal injury settlement is designed to pay back your insurers and, more importantly, compensate you for the full scope of your losses, including lost income, future medical needs, and the pain and suffering you have endured.

This is exactly why you need an experienced Texas personal injury lawyer. We manage this entire, complicated process, making sure every single bill is accounted for and submitted to the right place. Our job is to build a rock-solid claim that forces the other driver’s insurance to pay for every dollar of harm they caused, so you can put all your energy into getting better.

The Hidden Catch: How Insurance Subrogation Really Works

Using your health insurance to pay for immediate medical care is absolutely the right move after a car accident. It gets your doctors paid quickly and lets you focus on getting better. But it's critical to understand that this coverage isn't a gift—it's more like a loan that your health insurer fully expects to get back.

This repayment process is a legal concept called subrogation. It’s a term insurance companies don’t exactly advertise, but it can have a huge impact on your final settlement.

Put simply, subrogation gives your health insurance company the legal right to claw back every dollar it spent on your accident-related medical care from the settlement you get from the at-fault driver. When they pay your bills, they are essentially "stepping into your shoes" to collect that debt from the person who caused your injuries.

A Real-World Example of Subrogation

To see how this plays out, let’s picture a common scenario in Texas. You’re hurt in a multi-car pileup on a Houston freeway and need major surgery followed by months of physical therapy.

- Your health insurer pays $50,000 to the hospital and your doctors for your care.

- Your Houston car accident attorney builds a powerful case and negotiates a $200,000 settlement with the at-fault driver’s insurance company.

- Before that settlement money ever hits your bank account, your health insurer sends a demand letter for that $50,000 back. This claim is called a lien.

If you don't have an experienced lawyer fighting for you, you could end up handing over that full amount. That would seriously slash the money you're left with to cover everything else, like your lost wages and pain and suffering.

A subrogation lien is the health insurance company’s legal claim on your settlement funds. Their goal is to recover what they paid for your medical treatment, but this claim is often negotiable.

This is where having the right legal advocate becomes a game-changer. An insurance company’s initial demand is just that—a demand. It is not set in stone, and a skilled lawyer knows exactly how to push back.

How a Lawyer Fights to Reduce Liens and Protect Your Settlement

One of the most valuable things a Texas personal injury lawyer does is negotiate these liens down. We don't just roll over and accept the insurance company's first number. We fight to reduce the amount they can take from your settlement, which puts more of that hard-won money directly into your pocket.

Our legal team knows the laws and the arguments that work. We can challenge the fairness of the lien by:

- Auditing the Bills: We go through every single medical charge with a fine-tooth comb to make sure it was reasonable, necessary, and directly tied to the accident. We often find errors or unrelated charges that can be stripped from the lien.

- Arguing Common Law Doctrines: In Texas, we can argue that the lien should be cut based on legal principles like the "Made Whole Doctrine." This doctrine says an insurer can't get reimbursed until you have been fully compensated for all of your damages, not just your medical bills.

- Negotiating Pro-Rata Reductions: We also argue that the health insurance company should chip in for the cost of getting the settlement in the first place. This means they should reduce their lien to cover a fair share of your attorney's fees and legal expenses.

For instance, on that $50,000 lien, a skilled attorney might successfully negotiate it down to $30,000 or even less. That's an extra $20,000 or more that goes to you and your family to help rebuild your lives—not back into the insurance company's coffers. You can learn more by reading our guide on negotiating medical bills after a settlement.

Managing subrogation is a complex and absolutely critical part of any personal injury case. Without an expert on your side, accident victims can lose a huge chunk of their settlement to these hidden claims. At The Law Office of Bryan Fagan, PLLC, we handle every part of this process so you can focus on what really matters: your recovery.

Why You Still Need a Personal Injury Lawyer

Using your health insurance after a car crash is a smart and necessary first step. Think of it as a crucial safety net—it gets you the immediate medical care you need without having to worry about upfront costs. But that’s where its job ends.

It’s easy to think that once your medical bills are handled, the problem is solved. The reality is that your health plan only addresses one small piece of a much larger, life-altering puzzle. For a true, full recovery, you need an experienced personal injury lawyer. Our role goes far beyond just managing bills; we're here to build a powerful case for all the losses your health insurance policy will never, ever touch.

Fighting for Damages Health Insurance Ignores

Your health insurance contract is written with one purpose: to cover medically necessary treatments. That's it. It has absolutely no way to compensate you for the other devastating financial and personal losses that always follow a serious wreck.

A skilled Texas personal injury lawyer fights for a settlement or verdict that reflects the total impact the accident has had on your life. This includes fighting for compensation for:

- Lost Income: Every single paycheck you missed while you were out of work recovering.

- Future Lost Earning Capacity: If your injuries are catastrophic and you can't go back to your old job, our truck crash lawyers in Houston fight for the income you will now lose over the course of your working life.

- Future Medical Treatment: Your health plan covers today's needs. We work with medical and financial experts to calculate the cost of future surgeries, physical therapy, medications, and in-home care you might need for years to come.

- Pain and Suffering: This is real compensation for the physical pain, emotional distress, and mental anguish you've been forced to endure because of another driver's negligence.

- Loss of Enjoyment of Life: We fight for damages to acknowledge the hobbies, activities, and simple joys you can no longer experience because someone else was careless.

Here’s a good way to look at it: your health insurance helps patch up your physical injuries, but a personal injury claim is designed to help rebuild your entire life.

Your Shield Against Insurance Companies

From the moment an accident happens, the at-fault driver's insurance adjuster gets to work. Their one and only goal is to minimize how much money their company has to pay you. They want to protect their bottom line, not your well-being.

You can expect them to pressure you into giving a recorded statement, offer a quick and insultingly low settlement, or try to convince you your injuries aren't that serious.

Hiring a lawyer puts an immediate stop to these tactics. We become your shield. All communication from their insurance company is routed through our office, protecting you from their aggressive strategies. We handle the complex negotiations, deal with the subrogation claims from your own health insurer, and build a case so strong that they have no choice but to take your claim seriously.

A personal injury attorney levels the playing field, ensuring that you—the victim—are not taken advantage of by powerful insurance corporations. We manage the legal battle so you can focus all your energy on healing.

The importance of having proper insurance coverage simply cannot be overstated, as it directly impacts the quality of care you receive right after a crash. A major 2022 study of over 2.2 million motor vehicle crash patients revealed a stark reality: uninsured patients faced a significantly higher risk of dying. The study found that private insurance dropped the odds of death by 37%. Researchers also noted that uninsured individuals often receive less aggressive care—around 20% less treatment—because providers are worried about unpaid bills. You can find more insights from this study about insurance status and crash outcomes.

Your health is your most precious asset. You deserve a legal advocate who will fight tooth and nail for the maximum compensation you're entitled to under Texas law. Whether you were injured in a commercial truck wreck or a car crash, our team is ready to protect your rights. For families who have lost a loved one, a dedicated wrongful death lawyer in Texas can provide the compassionate guidance needed to seek justice.

Practical Steps to Protect Your Rights After a Texas Crash

The moments after a car crash are a blur of adrenaline and confusion. It’s tough to think clearly, but what you do in the hours and days that follow can make or break your physical and financial recovery. Taking charge of the chaos might feel impossible, but having a clear game plan is the best way to protect yourself.

Here's a simple, no-nonsense checklist to walk you through it. These steps can dramatically change the outcome of your case and put you in the best position to get the compensation you deserve.

1. Get Medical Help Immediately

Nothing is more important than your health. Even if you think you’re fine, adrenaline is a powerful painkiller that can hide serious problems like internal bleeding or a concussion. Go see a doctor right away, and don't hesitate to use your health insurance for the visit.

Putting off medical care is a huge mistake. Not only does it jeopardize your health, but it also gives the other driver’s insurance company an excuse to claim your injuries aren't from the crash. A documented medical record is your strongest piece of proof.

2. Report the Accident and Document Everything

Always, always call the police to the scene if anyone is hurt. An official police report is an unbiased record of what happened, which is vital for proving negligence—the legal term for showing the other driver failed to be careful. In Texas, this concept of fault is central to your ability to recover compensation.

While you're waiting, and only if you’re able, start gathering evidence with your phone:

- Take photos and videos of everything—the damage to both cars, skid marks, the road conditions, and any visible injuries.

- Swap contact and insurance information with the other driver. Get a picture of their license and insurance card.

- Talk to anyone who saw what happened. Get their names and phone numbers. Witness testimony can be a game-changer.

3. Be Careful What You Say

This is critical: never admit fault or even apologize at the scene. You don't have all the facts yet, and a simple "I'm sorry" can be twisted by an insurance company and used against you.

When you speak to the other driver's insurance adjuster, be polite but firm. You only need to provide the basics. Do not give a recorded statement until you've spoken with a Texas personal injury lawyer. Adjusters are trained to ask tricky, leading questions designed to trip you up and weaken your claim.

4. How Long Do You Have to File a Claim in Texas?

Texas law gives you a limited window to file a personal injury lawsuit. This is called the statute of limitations, and for most car accident claims, you have just two years from the date of the wreck to file.

If you miss this two-year deadline, the courthouse doors will almost certainly be closed to you forever. You lose your right to seek compensation. This is why it’s so important to get legal advice well before time runs out.

This deadline underscores just how urgent the situation is. Crash rates are on the rise, and while the insurance market is huge, victims often get stuck with a massive financial burden. In the U.S., people injured in crashes can end up paying 26% of the costs out of their own pockets. Without a solid personal injury claim, even the initial help from your health insurer can vanish after subrogation, leaving your family deep in debt. You can read more about the growing accident insurance market and how it affects families like yours.

5. Contact an Experienced Car Accident Attorney

The insurance and legal worlds are mazes, and they aren't set up to be fair to people without a lawyer. The sooner you bring a Houston car accident attorney on board, the better. We can immediately take over all communication with the insurance companies, make sure critical evidence is saved, and start building a powerful case for you.

You don't have to face this alone. At The Law Office of Bryan Fagan, PLLC, we offer a free consultation to help you figure out your rights and your next steps. We work on a contingency-fee basis, which means you pay us absolutely nothing unless we win your case.

Answers to Your Questions About Insurance and Car Accidents

After the trauma of a car accident, your mind is probably racing with dozens of questions. The insurance and legal maze can feel impossibly complicated, especially when you're trying to recover. You deserve clear, straightforward answers. Here are some of the most common questions we hear from accident victims across Texas.

What Happens If the At-Fault Driver Is Uninsured in Texas?

It’s a nightmare scenario: the driver who hit you has no insurance, or their policy is too small to cover your medical bills and damages. This is exactly why you have Uninsured/Underinsured Motorist (UM/UIM) coverage. If you opted for this coverage on your own policy, it essentially steps into the shoes of the at-fault driver's missing insurance.

Your health insurance will still kick in to cover your initial medical treatments. Behind the scenes, they will then seek reimbursement—a process called subrogation—from your UM/UIM settlement. Navigating this claim is complex, which is why a Houston car accident lawyer is so critical to making sure you get the maximum recovery from every available policy.

Can My Health Insurance Company Refuse to Pay for My Injuries?

Generally, no. Your contract with your health insurance company obligates them to pay for medically necessary care, no matter what caused the injury. That said, their first move will be to look for someone else to foot the bill—namely, the at-fault driver's insurer.

While some policies might have obscure exclusions for injuries that happen during illegal acts, it's extremely rare for a standard health plan to deny care after a car wreck. If your insurer is delaying or outright denying payment, that's a huge red flag. It’s a sign that you need to contact a personal injury attorney immediately to advocate on your behalf with all the insurance companies involved.

The entire point of health insurance is to get you medical care when you need it. Any hesitation from your provider after an accident is a signal that you need legal help to protect both your health and your rights.

If you want a better grasp on your medical bills and how your insurer processes them, it helps to understand how a simple doctor's visit gets translated into charges using specific E&M codes.

Do I Have to Repay My Health Insurance If I Lose My Case?

No. Your health insurer’s right to get their money back (subrogation) only kicks in if you actually recover money from the at-fault party. If you don't win a settlement or a lawsuit verdict, there's simply no fund for them to be repaid from.

This is exactly why having a skilled lawyer to build a rock-solid case is so important. At The Law Office of Bryan Fagan, PLLC, we work on a contingency fee basis. That means you owe us nothing unless we win your case.

Will Using My Health Insurance Make My Premiums Go Up?

Using your health plan for a car accident shouldn't cause your premiums to spike. The ultimate financial responsibility falls on the at-fault driver's auto insurance, and your health insurer fully expects to get its money back through subrogation.

You should never, ever delay getting medical care because you're worried about a premium increase. Your health and recovery are the number one priority. Let the lawyers sort out who pays for what later.

You Are Not Alone—We Can Help You Move Forward

A serious car accident can turn your world upside down in a heartbeat. Suddenly, you're dealing with injuries, medical bills, and an insurance system that feels intentionally complicated and stacked against you. But you don't have to face this overwhelming aftermath by yourself. With the right legal team in your corner, you can fight for the resources you and your family need to truly recover.

It's important to remember that your health insurance is a crucial tool for getting immediate medical care, but it was never designed to make you whole again. It can't cover your lost wages, and it certainly can't compensate you for the pain and suffering caused by a negligent driver. A personal injury claim is the only way to hold the at-fault party fully accountable for the damage they've done to your life.

Our Commitment to Texas Families

At The Law Office of Bryan Fagan, PLLC, we are deeply committed to fighting for Texas families who have been hurt by someone else's carelessness. We know the physical, emotional, and financial weight you're carrying, and our entire team of experienced personal injury attorneys is here to lift that burden off your shoulders.

We take care of everything—from investigating the crash and handling aggressive insurance adjusters to fighting to reduce medical liens so that more of the settlement money stays in your pocket. We are proud to represent our clients on a contingency-fee basis.

What does this mean for you? It means you pay absolutely nothing unless we win your case. There are no upfront costs and no hidden fees. Our payment is simply a percentage of the compensation we recover for you, which allows you to get top-tier legal help without any financial risk.

Recovery is possible, and legal help is available. We invite you to schedule a free, no-obligation consultation with a compassionate Texas personal injury lawyer. Let us hear your story, explain your rights in plain English, and show you how we can help you start the journey toward healing and justice.

Don't wait to get the answers and support you deserve. Contact The Law Office of Bryan Fagan, PLLC today to schedule your free consultation and learn how we can help you move forward. Visit us at https://texaspersonalinjury.net.