A serious accident can change your life in seconds — but you don’t have to face it alone. Figuring out what comes next can feel overwhelming, especially when you’re trying to heal. Before you can even think about a settlement number, you first have to understand every single loss you’ve suffered—and it’s often more than you realize.

A fair settlement isn’t just a random number offered by an insurance company. It's a comprehensive figure that accounts for everything from the initial emergency room visit to the hidden, long-term costs that a serious injury can bring. This guide will help you understand how a settlement is calculated and what you can do to protect your rights.

Understanding What Your Settlement Should Cover

After a crash, your only focus should be on getting better. But the financial pressure mounts quickly. Medical bills start rolling in, you might be out of work, and your car is probably wrecked. This is why knowing how to calculate a fair settlement starts with identifying every single loss you've had to endure.

A proper calculation makes sure that no part of your suffering gets ignored. In Texas, the law allows you to seek compensation for two main categories of losses, known as damages. These two categories are the foundation of your entire claim.

The Two Pillars of a Texas Settlement Claim

Think of your settlement as having two essential components: economic and non-economic damages.

Here's a quick look at the types of compensation you can pursue in a Texas car accident claim.

Types of Compensation in a Texas Car Accident Claim

| Type of Damage | Description | Examples |

|---|---|---|

| Economic | These are the tangible, out-of-pocket financial losses with a clear dollar amount. They can be proven with receipts, bills, and pay stubs. | Medical bills (past and future), Lost wages, Lost earning capacity, Property damage, Physical therapy, Prescriptions |

| Non-Economic | These are the intangible, personal losses that don’t have a price tag. They represent the human cost of the accident. | Pain and suffering, Mental anguish, Disfigurement, Physical impairment, Loss of enjoyment of life, Loss of consortium |

Both of these pillars are critical for building a strong claim that truly reflects everything you've been through.

Diving Deeper into Economic and Non-Economic Damages

Let's break down what these really mean for you and your family.

Economic damages are the most straightforward part of your claim. These are the concrete financial hits you’ve taken. We're talking about things you have receipts for: hospital bills, repair invoices for your car, and pay stubs showing your lost income.

Non-economic damages are just as real, but they represent the human cost of the accident. There's no bill for the chronic back pain that keeps you from picking up your kids or the anxiety you now feel every time you get behind the wheel. These are the personal, intangible losses that deeply affect your quality of life.

Imagine you were involved in a multi-car pileup on a Houston freeway. Your economic damages would be clear: the ambulance bill, your hospital stay, and the cost of repairing your truck. But your non-economic damages would account for the panic attacks you now have in traffic and the constant pain that stops you from enjoying your weekend hobbies. Both are equally important.

A common mistake we see people make is focusing only on the bills they have right now. A fair settlement must also project into the future, covering potential surgeries, lost promotions at work, and the ongoing emotional toll. Overlooking these future costs can leave you financially exposed down the road.

The final settlement amount involves a complex process that considers the severity of your injuries, medical costs, lost income, and the personal impact of your pain and suffering. While some sources say the average settlement for an injury accident is around $30,416, that number can be misleading. A minor whiplash case might settle for $10,000, whereas a catastrophic injury claim could easily exceed $1,000,000.

Understanding these components is the first step. For a complete overview of what to do next, you can learn more about how to file a car accident claim in our detailed guide.

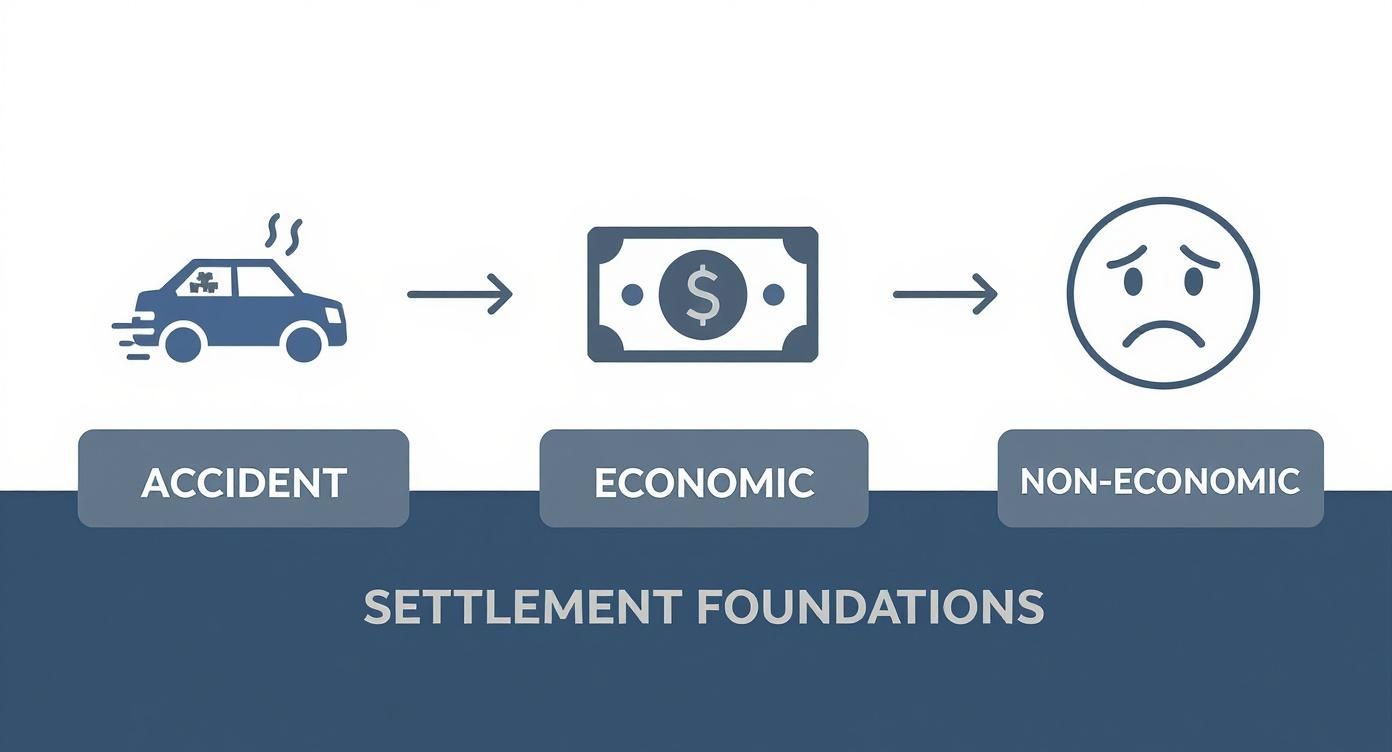

Calculating Your Economic Damages with Precision

After a wreck, the most straightforward losses are the ones with a clear price tag. In legal terms, we call these economic damages, and they serve as the undisputed foundation of your settlement. Think of it as building a detailed invoice for every single dollar the accident has cost you. Getting this part right is absolutely critical for building a strong, evidence-based claim.

This isn't just about adding up a few numbers. It’s about meticulously gathering every bill, receipt, and pay stub to tell the complete financial story of your recovery.

The infographic below shows how a final settlement is constructed, starting with these concrete economic losses.

As you can see, these tangible costs—your economic damages—provide the solid base. From there, the more personal, less tangible losses (non-economic damages) are often calculated.

Documenting Every Medical Expense

Your medical journey is the biggest piece of the economic damages puzzle. Every single cost, no matter how small it might seem, needs to be documented. The insurance adjuster will pick these expenses apart, so having organized, complete records is your best defense.

Start a file and keep every bill you receive for:

- Ambulance rides and emergency room treatment

- Hospital stays, surgeries, and appointments with specialists

- X-rays, MRIs, CT scans, and other diagnostic tests

- Prescription drugs and medical gear like crutches or braces

- Physical therapy, chiropractic care, and rehabilitation sessions

A huge mistake people make is only counting the bills they've already paid. A truly fair settlement must also cover the cost of all future medical care your doctors say you'll need, like more surgeries, ongoing therapy, or long-term pain management.

Let's say you were in a serious truck crash on I-10 in Houston. The initial hospital bill might be $50,000. But what if your doctor confirms you'll need two more surgeries and physical therapy for the next year? Those future costs could easily top $100,000, and they absolutely must be professionally estimated and included in your demand. A good truck crash lawyer in Houston will work with medical experts to project these future expenses so you're not left paying out of pocket down the road.

Accounting for Lost Income and Earning Capacity

The financial fallout from a serious injury goes way beyond medical bills. When you can't work, the loss of income can put your entire family in a tough spot. This part of your claim is about more than just the paychecks you missed while you were recovering.

You have to calculate both:

- Lost Wages: This is the direct income you lost. Add up every hour of work you missed, including regular pay, overtime you would have worked, and any sick or vacation days you had to use.

- Lost Earning Capacity: This is a bigger, long-term loss. If your injuries permanently keep you from returning to your old job or limit your ability to earn the same income in the future, you deserve to be compensated for that lifetime of diminished earnings.

Imagine a Dallas-area electrician who suffers a permanent hand injury in a crash. He can no longer do his job. The calculation must include the difference between his old salary and what he's capable of earning now, projected out for the rest of his career. For help getting these numbers exact, tools like specialized economic damage calculators can provide a solid starting point.

Tallying Property Damage and Other Costs

Finally, don't let the other out-of-pocket expenses slip through the cracks. They add up fast. The cost to repair or replace your vehicle is the most obvious one, but property damage also covers any personal items that were ruined in the collision.

Make a list of everything, including:

- Laptops, tablets, or cell phones

- Child car seats (these should always be replaced after a crash)

- Prescription eyeglasses or other personal belongings

Also, be sure to track those little incidental costs, like paying for a rental car or grabbing an Uber to get to your doctor's appointments. Every documented expense makes your claim stronger and gets you one step closer to a settlement that truly covers everything you've lost.

Putting a Value on Your Pain and Suffering

How do you even begin to put a dollar amount on the physical pain or emotional trauma from a wreck? This is, without a doubt, the most challenging—and most fought-over—part of any car accident settlement. We’re talking about your non-economic damages, the very real human cost of your injuries.

Insurance companies are trained to minimize these losses. Why? Because there’s no clean invoice for suffering or a receipt for the joy that’s been stripped from your life. But make no mistake, your pain and suffering are just as real and compensable under Texas law as your medical bills. You have a right to demand fair value for them.

The Multiplier Method Explained

One of the most common starting points for estimating non-economic damages is the Multiplier Method. Think of it as a formula that both attorneys and insurance adjusters use to translate your suffering into a monetary value, based on the severity of your injuries and how they’ve upended your life.

It’s a two-step process:

- First, we tally up all your total economic damages—every last medical bill, lost paycheck, and future medical expense.

- Then, we multiply that total by a number, which typically falls somewhere between 1.5 and 5.

That multiplier isn’t just pulled out of thin air. It’s meant to reflect how drastically the accident has changed your world. A lower multiplier, like a 1.5 or 2, might apply to injuries that heal up pretty quickly with minimal fuss, like a minor case of whiplash. The higher multipliers—4s and 5s—are reserved for catastrophic injuries that lead to permanent disability, scarring, or a lifetime of chronic pain.

How Is the Right Multiplier Chosen?

This is where the art of negotiation really comes into play. A seasoned Texas personal injury lawyer doesn’t just pick a number; they build a compelling case for a higher multiplier by showing exactly how the accident has impacted you.

Factors that push for a higher multiplier include things like:

- The Severity of the Injury: A traumatic brain injury is going to justify a much higher multiplier than a broken arm.

- Length of Recovery: A long, grueling recovery that involves multiple surgeries and years of physical therapy demands a higher value.

- Permanent Impairment or Disfigurement: Lasting scars, a limp that will never go away, or the loss of a limb will significantly drive up the multiplier.

- Impact on Daily Life: Can you no longer pick up your kids, enjoy your favorite hobbies, or even get through the day without pain? These are powerful factors.

After a Houston freeway crash, a construction worker suffers a severe back injury. His economic damages for surgery and lost income add up to $150,000. The injury left him with chronic pain so severe he can no longer lift anything heavy. It ended his career and means he can never again pick up his young children. His attorney would argue for a high multiplier, maybe a 4.

Calculation Example: $150,000 (Economic Damages) x 4 (Multiplier) = $600,000 in non-economic damages. His total settlement demand would start at $750,000.

This general approach isn't unique to Texas. Many legal systems around the world use a similar logic for car accident settlements, multiplying medical costs by a factor to account for pain and suffering, with the multiplier often ranging from 1.5 to 5. Of course, lost wages and property damage are then added to that total. If you're curious about how these principles work elsewhere, you can discover more insights about international car accident settlements on louisberklaw.com.

The Per Diem Method

There’s another, less common way to look at it called the Per Diem Method. "Per diem" is just Latin for "per day." This method assigns a specific dollar amount for every single day you lived with pain and suffering, starting from the day of the accident until the day your doctors say you’ve reached "maximum medical improvement."

Often, the daily rate is linked to what you earned per day at your job. The argument is simple: enduring the pain from your injuries was at least as difficult as going to work every day. While it sounds straightforward, this approach is usually a better fit for shorter-term injuries. It can be much harder to justify for injuries that cause long-term or permanent disability.

Calculating the true value of what you’ve been through is deeply personal and far more complex than a simple formula. It takes telling your story in a powerful, evidence-backed way. Whether you were hurt in a Houston car wreck or a loved one was lost, an experienced attorney knows how to show the full picture of your ordeal and fight for the compensation you are owed.

How Texas Fault Laws Impact Your Final Payout

Calculating the full extent of your damages is a monumental first step, but it’s rarely the final number the insurance company will pay. In Texas, a few key legal rules can dramatically change the amount you actually receive.

It's crucial to understand these rules because the insurance company will use them to reduce or deny your claim. This is the point where a simple calculation becomes a legal negotiation—one guided entirely by state law. It's not just about what you've lost; it's about what Texas law says you're entitled to recover based on who was at fault.

Texas's Proportionate Responsibility Rule

The single most critical law affecting your settlement is the Proportionate Responsibility statute, also known as comparative fault. This rule applies when more than one person is to blame for an accident.

Insurance companies will work tirelessly to shift as much blame as possible onto you. Why? Because every single percentage point of fault assigned to you directly reduces their payout.

The rule works in two distinct ways:

- The 51% Bar: This is a harsh, all-or-nothing threshold. If you are found to be 51% or more at fault for the accident, Texas law bars you from recovering any compensation. It doesn't matter how severe your injuries are; being assigned the majority of the blame means you walk away with nothing.

- The Reduction Rule: If you are found to be 50% or less at fault, you can still recover damages. However, your final settlement gets reduced by your exact percentage of fault.

Imagine your total damages after a collision on I-45 in Houston are calculated at $100,000. The other driver's insurance company argues you were partially to blame for changing lanes without signaling. If a jury finds you 20% at fault, your maximum potential recovery is immediately slashed to $80,000.

This is why having a skilled Houston car accident attorney is so vital. We anticipate these arguments from day one. We build a powerful case using police reports, witness statements, and accident reconstruction experts to minimize any fault assigned to you and protect the full value of your claim.

The Impact of Insurance Policy Limits

Another real-world barrier to a full recovery is the at-fault driver's insurance policy limit. No matter how high your calculated damages are, an insurance company is only obligated to pay up to the maximum coverage their client purchased.

In Texas, the minimum liability coverage drivers must carry is shockingly low:

- $30,000 for bodily injury liability per person

- $60,000 for bodily injury liability per accident

- $25,000 for property damage liability per accident

If your damages easily exceed these minimums—which happens in almost any serious injury case—the at-fault driver's policy simply won't be enough. For instance, if your medical bills alone are $75,000 and the other driver only has the minimum $30,000 policy, the insurer will cut a check for $30,000 and consider their obligation met.

When this happens, an experienced attorney will immediately start looking for other avenues for compensation, such as:

- Pursuing a claim against the driver's personal assets (if they have any).

- Filing a claim under your own Uninsured/Underinsured Motorist (UIM) coverage.

- Identifying if a third party, like an employer or vehicle manufacturer, shares responsibility for the crash.

How Long Do You Have to File a Claim in Texas?

You absolutely must be aware of a critical deadline known as the statute of limitations. In Texas, you generally have just two years from the date of the accident to file a personal injury lawsuit.

This isn't a suggestion; it's a hard deadline.

If you fail to file your lawsuit within that two-year window, the court will almost certainly dismiss your case, and you will lose your right to seek compensation forever. Insurance companies know this and often use it to their advantage, delaying and dragging out negotiations in the hope that you'll miss your chance to take legal action.

Acting quickly is crucial. It gives your legal team time to preserve evidence, interview witnesses while their memories are fresh, and ensure every legal deadline is met. If you or a loved one has suffered a catastrophic injury or you need a wrongful death lawyer in Texas, don't wait to understand your rights.

Navigating the Settlement Negotiation Process

Once you’ve done the hard work of calculating all your economic and non-economic damages, you move into a new phase. You’re no longer just adding up bills; you're preparing to fight for the compensation you need to get your life back on track. This is where settlement negotiations begin, a strategic back-and-forth where a skilled Houston car accident attorney can make all the difference.

The whole thing formally kicks off with a document called a demand letter. It's much more than just a simple letter asking for money. It's a detailed legal argument, professionally written by your attorney, that lays out every fact of your case, presents clear evidence of the other driver's negligence, and provides a full breakdown of your damages.

The Initial Offer and Counteroffer Exchange

Get ready for the insurance adjuster's first move. These adjusters are professionals trained with one primary goal: protecting their company's profits by paying out as little as possible. Because of this, their initial offer will almost certainly be a lowball figure. It's designed to see if you’re stressed enough to accept a quick, cheap payout.

It's absolutely critical that you don't get discouraged. This is a standard tactic and an expected part of the negotiation process.

The power of your response is rooted in the evidence you’ve carefully gathered. This is where your organized medical records, the police report, and proof of lost income become your best weapons. Your attorney will use all this documentation to build a counteroffer that systematically tears apart the insurer’s low valuation and re-establishes the true cost of what you’ve been through.

The goal is simple: show the insurance company that you have a solid, well-documented case that would very likely win at trial. That leverage is what forces them to come back with a more serious offer.

The Reality of Reaching a Settlement

Negotiations can feel like a long, drawn-out battle, so it’s important to set realistic expectations. The vast majority of personal injury cases never see the inside of a courtroom. In fact, somewhere around 95-96% of cases in the U.S. are settled out of court through this exact negotiation process.

Depending on the complexity of your injuries, the process can take anywhere from 12 to 36 months. Severe injuries often require a longer timeline to fully document the need for future medical care.

The whole thing is a strategic give-and-take. While you might see parallels in other financial negotiations, like learning about strategies for settling tax debt through an Offer in Compromise, the personal stakes in an injury claim are profoundly higher. Still, seeing how other complex claims are resolved highlights the universal importance of rock-solid preparation and firm, evidence-based arguments.

This complicated back-and-forth is precisely why having a dedicated legal advocate is so important. A Texas personal injury lawyer handles every bit of communication with the insurance company, shielding you from their pressure tactics so you can focus on healing. They know the game and will fight to make sure the final number truly reflects everything you have endured. To get a better handle on what to expect, you can learn more about how to negotiate a personal injury settlement in our detailed guide.

Common Questions About Texas Car Accident Settlements

When you're trying to heal after a car crash, the last thing you want is a mountain of legal questions. You’re likely overwhelmed, in pain, and just want clear answers. We hear these same concerns from clients every day, so here are some straightforward answers to the questions we get asked the most.

Should I Accept the Insurance Company's First Settlement Offer?

It’s almost never a good idea to accept the first offer. Think of it as the insurance company's opening bid—and it's intentionally low. They're in business to pay out as little as possible, and they're hoping your financial stress will push you to take a quick, cheap payout.

That first offer rarely accounts for the full picture. It doesn't consider future physical therapy, potential lost earning capacity, or the real-world impact of your pain and suffering. Before you even think about accepting, you should talk to a Texas personal injury lawyer. We can help you understand what your claim is actually worth and make sure you don't leave money on the table that you'll need down the road.

How Long Do I Have to File a Car Accident Claim in Texas?

In Texas, you generally have two years from the date of the accident to file a personal injury lawsuit. This is called the statute of limitations, and it’s a hard deadline.

If you miss it, you will almost certainly lose your right to seek compensation forever. Two years might sound like a long time, but evidence can disappear quickly. Security camera footage gets erased, and witnesses' memories fade. The sooner you get an attorney involved, the better your chances are of preserving the evidence needed to build a strong case and protect those critical legal deadlines.

How Is Fault Determined in a Texas Car Accident?

In Texas, fault boils down to proving negligence. This means showing that another driver wasn't reasonably careful, and their carelessness is the direct reason you got hurt. This isn't just about pointing fingers; it requires solid evidence.

To establish fault, we often rely on:

- The official police report filed at the scene.

- Photos showing vehicle damage, road conditions, and your injuries.

- Statements from eyewitnesses who saw what happened.

- Video from traffic lights or nearby business security cameras.

Texas also uses a system called "proportionate responsibility." This means fault can be split and assigned as a percentage to everyone involved. That percentage is a big deal because it directly reduces your settlement. If you're found 10% at fault, for example, your final compensation is cut by 10%.

You can be sure the insurance company will try to shift as much blame as possible onto you—even a tiny amount—just to lower their payout. A good lawyer knows how to fight back against these tactics and protect the true value of your claim.

Do I Need a Lawyer to Calculate My Settlement?

Legally, no, you don't have to hire an attorney. But trying to calculate and negotiate a fair settlement on your own is a huge risk, especially if your injuries are serious. So much of a settlement's value comes from non-economic damages like pain and suffering, and there's no simple calculator for that. It takes experience.

An experienced personal injury lawyer knows how to gather the right medical evidence to prove your need for future care and understands how to navigate Texas's complicated fault rules. More importantly, we're trained negotiators who won't be pushed around by insurance adjusters and their lowball tactics.

Data shows that accident victims who have a lawyer on their side consistently recover significantly higher settlements than those who handle it alone. A lawyer ensures your calculation is right from the start and gives you a powerful advocate fighting for every dollar you deserve. For more on what to do right away, check out our post on what to do after a car accident.

A serious accident can flip your world upside down in an instant, but you don’t have to pick up the pieces by yourself. We know that recovery is possible, and we are here to provide the legal help you need. The experienced attorneys at The Law Office of Bryan Fagan, PLLC are here to answer your questions, stand up for your rights, and fight for the full and fair settlement you need to move forward.

Let us handle the legal headaches so you can focus on what’s most important: your health and your family. We invite you to schedule a free, no-obligation consultation to talk about your case and get clear answers about your next steps.

Schedule Your Free Consultation with The Law Office of Bryan Fagan, PLLC