A serious accident can change your life in seconds — but you don’t have to face it alone. The "right" amount of uninsured motorist coverage is whatever it takes to protect your family—to cover the medical bills, replace lost income, and provide for future care needs after a wreck.

Our strong recommendation is to get coverage limits that are at least equal to your own liability coverage. Even better, get as much as you can comfortably afford. This is how you truly protect your financial future.

The Hidden Risk on Every Texas Highway

Driving on any major Texas road, whether it's the Katy Freeway in Houston or I-35 cutting through Dallas, carries an invisible risk. A serious accident is devastating enough. Discovering the at-fault driver has little or no insurance just adds a financial crisis to the physical and emotional trauma—a crisis no family should have to face.

Unfortunately, this happens all the time.

This isn't some minor headache; it's a massive threat to your financial stability. The number of uninsured drivers has been creeping up, making the roads more dangerous for responsible drivers like you. In fact, the latest data shows that more than one in seven drivers on the road right now has zero insurance coverage. You can read the full research on uninsured motorists to really grasp the scale of the problem.

Why This Coverage Is Your Strongest Defense

Uninsured/Underinsured Motorist (UM/UIM) coverage isn't just another line item on your policy declaration page. It is your family’s most important financial shield. It was specifically designed to protect you when the person who hurt you can't pay for the damage they caused.

This coverage steps in to pay for the exact same things the at-fault driver’s insurance should have covered, including:

- Medical Expenses: This is everything from the initial ER visit and hospital bills to any future surgeries, physical therapy, and long-term rehabilitation you might need.

- Lost Wages: If you can't work because of your injuries, UM/UIM replaces the income your family depends on to pay the bills and stay afloat.

- Pain and Suffering: This compensates you for the very real physical pain and emotional trauma the crash caused—things that can haunt your quality of life for years.

- Wrongful Death: In the most tragic cases, this coverage provides critical financial support for families who have lost a loved one because of an uninsured driver.

Think of UM/UIM as a safety net that you get to control. You can't make other drivers be responsible, but you can make sure your own policy is strong enough to protect you from their mistakes.

After a Houston freeway crash, your focus should be on healing, not on how you’ll pay for the mountain of medical bills. UM/UIM coverage gives you that peace of mind, ensuring a path to recovery is there when you need it most.

Understanding this coverage is the first step toward building a secure future for you and your family. It’s all about being prepared, informed, and empowered. Whether you've been in a minor fender-bender or a catastrophic truck accident, knowing your policy has your back can make all the difference.

Calculating Your Family's Financial Safety Net

https://www.youtube.com/embed/K8VnPLGHRRc

Trying to figure out how much uninsured motorist coverage you need can feel like guessing in the dark. But it really boils down to one powerful question: What would it take to keep your family financially stable after a life-altering accident?

This isn't just about covering an emergency room visit. It’s about building a genuine financial safety net—one strong enough to handle the long-term fallout from a serious injury caused by someone with little or no insurance. You're essentially planning for a worst-case scenario to make sure your family’s future is secure, no matter what happens on the road.

A good rule of thumb to start with is matching your UM/UIM limits to your own bodily injury liability limits. If you carry a $250,000/$500,000 liability policy, your UM/UIM protection should be at least that high. This creates a balanced policy, but honestly, it’s just the beginning of the conversation.

Looking Beyond the Initial Medical Bills

When a serious crash happens, the immediate medical bills are often just the tip of the iceberg. A catastrophic injury, like a traumatic brain injury or spinal cord damage, can require a lifetime of care. You have to think much bigger than the first few weeks of treatment.

To get a real sense of your needs, you need to look at these critical financial areas:

- Your Family's Monthly Income: How much money does your family actually need each month to cover the mortgage, utilities, groceries, and everything else? If a primary earner is out of work for months—or permanently—your UM/UIM coverage has to be able to replace that lost income.

- Future Medical Needs: A severe injury doesn't just disappear when you leave the hospital. Your family could be facing years of expenses for physical therapy, follow-up surgeries, prescriptions, and specialized medical equipment like wheelchairs or home modifications.

- Long-Term and Catastrophic Care: In the most severe cases, an accident victim might need round-the-clock nursing care or even placement in a specialized facility. These costs can easily climb into the hundreds of thousands, if not millions, of dollars over a lifetime.

Your insurance policy is a promise. It’s a promise from the insurance company to be there for you when you need it most. Your job is to make sure the dollar amount attached to that promise is enough to truly protect your family.

A Real-World Houston Scenario

Let's make this tangible. Imagine a 40-year-old construction worker from Houston who supports his family on a $75,000 annual salary. He gets hit in a severe truck crash on the 610 Loop. The other driver is uninsured. The crash leaves our construction worker with a permanent back injury, and he can never return to his physically demanding job.

How do we figure out the coverage his family really needs?

- Lost Earning Capacity: At $75,000 a year, with 25 working years left until retirement, that’s a potential loss of $1,875,000 in future income alone.

- Medical Costs: His initial surgery and hospital stay cost $200,000. He's going to need ongoing physical therapy ($10,000/year) and pain management injections ($15,000/year) for the foreseeable future. Over just ten years, that's another $250,000.

- Non-Economic Damages: We also have to account for the immense physical pain, emotional distress, and the loss of quality of life he and his family will suffer. Texas law allows for compensation for this kind of suffering.

When you add it all up, his family’s total losses could easily top $2 million. If he only carried the state minimum UM coverage of $30,000, his family would be facing financial ruin. This is exactly why a high-limit policy isn't a luxury; it's an absolute necessity.

You can get a deeper understanding of how these figures are calculated by reviewing a guide on how to calculate car accident settlement amounts. It’s also important to remember that insurance is just one of the essential components of a robust financial safety net, such as an emergency fund calculator, that can prepare you for unexpected setbacks.

Sample UM/UIM Coverage Calculation for a Texas Family

To help visualize this, here’s a sample table showing how a family might estimate their coverage needs based on the potential financial impact of a serious accident.

| Potential Financial Loss Category | Example Annual Cost | Estimated Need (5-10 Years) | Recommended Coverage |

|---|---|---|---|

| Lost Income Replacement | $80,000 | $400,000 – $800,000 | At least $500,000 |

| Future Medical & Therapy | $25,000 | $125,000 – $250,000 | At least $250,000 |

| Long-Term Care/Assistance | $50,000+ | $250,000 – $500,000+ | $500,000 to $1M+ |

| Home/Vehicle Modifications | N/A (One-time) | $50,000 – $100,000 | Included in overall need |

| Total Estimated Need | $825,000 – $1,650,000+ | $1M+ (Policy + Umbrella) |

This simple breakdown shows how quickly the costs add up, far exceeding the state minimums and even standard policy limits. An umbrella policy becomes crucial for bridging that gap.

Having the Right Conversation With Your Agent

When you talk to your insurance agent, don't just ask for a quote. Have a real conversation about your life, your family, and what you stand to lose. Be ready to discuss:

- Your Annual Income: Explain exactly how much your family depends on your income.

- Your Health Insurance: Go over your health plan's deductible and out-of-pocket maximums. You’ll have to cover those costs yourself before your health insurance fully kicks in.

- Your Assets: Mention your home, savings, and retirement accounts. These are the very assets you are trying to protect from being wiped out by medical debt.

Armed with this information, you can have a meaningful discussion about getting a policy with limits of $250,000, $500,000, or even a $1 million umbrella policy. The peace of mind that comes from knowing you’ve done everything possible to protect your family is invaluable.

The True Cost of an Accident Without Enough Coverage

A serious crash can flip your world upside down in a heartbeat. The gap between what a catastrophic injury actually costs and what an irresponsible driver can pay is where hardworking families get financially ruined. Once you understand that gap, you’ll know exactly how much uninsured motorist coverage you really need.

Let’s make this real. Imagine a family driving home on I-10 in Houston. A distracted driver runs a red light and T-bones them. The at-fault driver only has the Texas state minimum liability coverage of $30,000. The mother in the passenger seat suffers a severe spinal injury, and her initial hospital bill is $150,000.

Instantly, that family is facing a financial nightmare. They're $120,000 in the hole from the very first medical bill, and the other driver's insurance is completely tapped out. This doesn’t even begin to cover her months of lost income, the staggering cost of physical therapy, or the painful reality that she might never return to her career.

This isn't some far-fetched hypothetical. It's a brutal reality for countless Texas families every year. This is precisely why having enough UM/UIM coverage is so critical. It’s not about fixing a dented bumper; it’s about protecting your home, your savings, and your family's entire future from being destroyed by someone else’s mistake.

Your Policy is a Lifeline, Not Just a Legal Minimum

Texas law requires drivers to carry liability insurance, but the minimums—just $30,000 per person and $60,000 per accident—haven't kept up with the sky-high cost of medical care. A single night in the ICU or one major surgery can blow past those limits, leaving you on the hook for the rest.

When the driver who hit you is uninsured, you have nothing to claim against. When they're underinsured, you're left with a pittance. In both scenarios, your own UM/UIM policy becomes your primary—and often only—source of financial recovery.

This is where the concept of negligence is key. The other driver failed to drive safely and caused you harm. In a fair world, they’d be responsible for every penny of your damages. But when they don’t have the insurance to pay, your UM/UIM coverage steps into their shoes.

UM/UIM coverage is the promise you make to yourself. It’s the guarantee that your recovery won't be capped by the poor choices of another driver. Your own policy limits are the foundation of your ability to rebuild your life.

The Financial Reality of an Uninsured Motorist Claim

Most people are shocked at how quickly accident costs pile up. The numbers show why strong coverage is a must. For uninsured motorist bodily injury claims, the average payout is around $29,825.

That amount can help with immediate medical bills and a few weeks of lost wages. But as our Houston scenario shows, it’s often just a drop in the bucket for serious injuries. This figure typically represents what's available under a policy, not the full, devastating cost of a victim's losses. If you're trying to figure out what fair compensation really looks like, our guide on how much compensation you can expect for a car accident can provide more clarity.

Why You Need an Advocate on Your Side

Here's the frustrating part: even with a great UM/UIM policy, getting the money you're owed isn't automatic. Your own insurance company—the one you've paid faithfully for years—may try to downplay your injuries or challenge your losses to protect their bottom line. This is when a skilled Houston car accident attorney becomes your most important asset.

We deal with these tactics every single day. We know exactly how to:

- Document Every Penny of Your Losses: We meticulously gather proof of all your medical bills, lost earning capacity, and the costs of any future care you'll need.

- Prove the Other Driver's Fault: We establish the other driver's negligence, which is a critical requirement for any personal injury claim in Texas.

- Fight for Your Full Compensation: We negotiate aggressively with your insurer to make them honor the policy you paid for.

A knowledgeable Texas personal injury lawyer understands the nuances of comparative fault and the strict statute of limitations. We make sure every deadline is met and that your claim is positioned for the best possible outcome. Your job is to focus on healing; our job is to fight for the resources you need to do it.

Making Sense of Your Texas Auto Policy

Let's be honest, insurance policies can feel like they're written in another language. They're packed with jargon that leaves most people more confused than confident. But taking a little time to understand a few key concepts on your policy's declaration page is a huge step toward taking control. When you can cut through the confusing language of your Texas UM/UIM coverage, you can make sure you and your family are actually protected.

A good starting point is knowing the state's baseline Texas auto insurance requirements. Just remember, these minimums are only the floor—true financial safety almost always requires more.

Stacking vs. Non-Stacking Policies

One of the most important—and most misunderstood—terms you’ll come across is stacking. In some states, "stacking" is a great feature. It lets you combine the UM/UIM coverage from multiple cars on your policy to create one big pool of money after a crash.

However, Texas is a non-stacking state. This is a critical detail. It means that if you own three cars, each with $100,000 in UM/UIM coverage, you can't "stack" them to create a $300,000 limit for a single accident. You're stuck with the coverage limit on the specific vehicle involved in the crash. This rule makes it absolutely essential to choose high enough limits on each vehicle you insure.

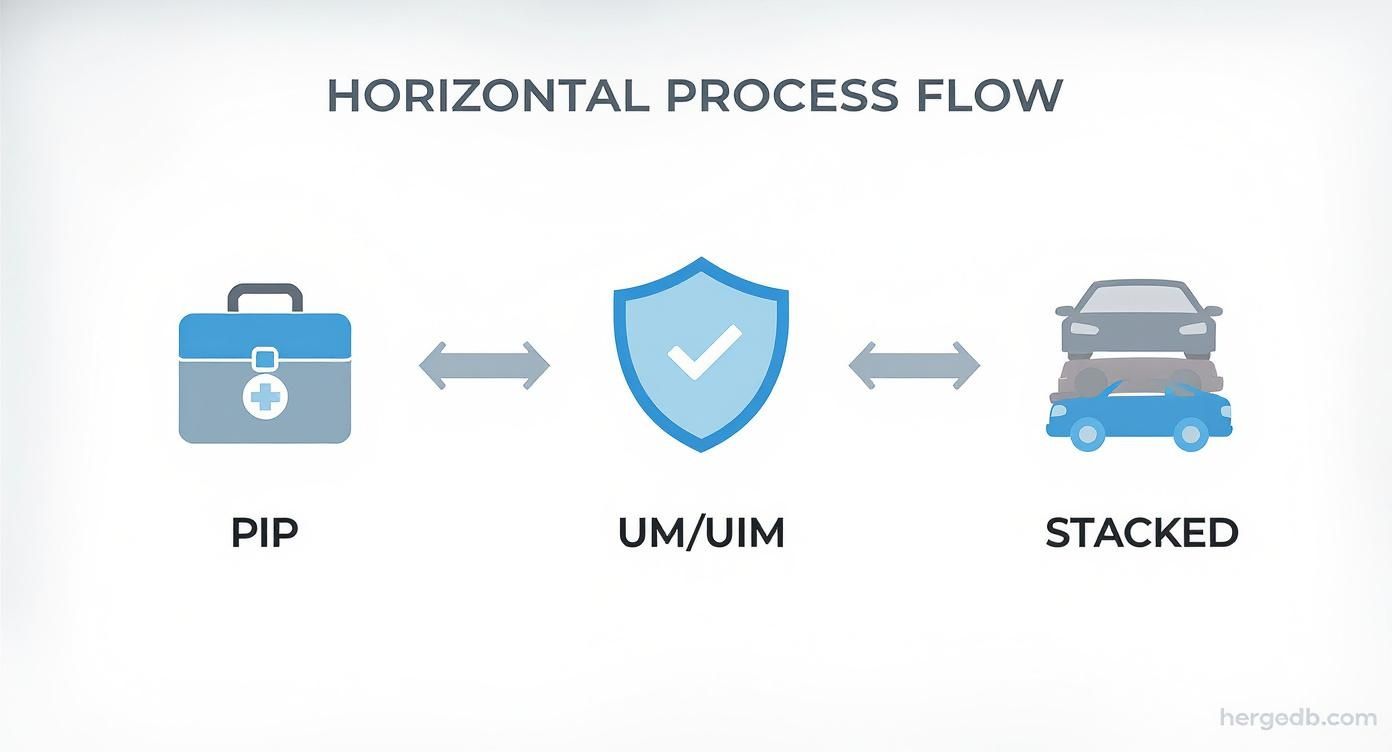

Personal Injury Protection (PIP): Your First Line of Defense

Another vital piece of your policy puzzle is Personal Injury Protection (PIP). In Texas, insurance companies automatically include PIP in your policy unless you go out of your way to reject it in writing. It’s a no-fault coverage, meaning it pays out quickly for your initial medical bills and a chunk of your lost wages, no matter who caused the accident.

Think of PIP and UM/UIM as a powerful team working together for you:

- PIP is for immediate needs. It pays out fast for things like the ambulance ride, the emergency room visit, and your first few doctor's appointments, up to your policy limit (which usually starts at $2,500).

- UM/UIM is for the big picture. It's there to cover the much larger, long-term costs that come with serious injuries. This includes ongoing medical care, major income loss, and compensation for pain and suffering once your PIP runs out.

Having both creates a two-layer safety net. It ensures you have immediate funds to get the care you need while your attorney builds the case for the full compensation you deserve from your UM/UIM policy. This is especially crucial for anyone who has suffered a catastrophic injury.

You should never have to choose between getting medical care and paying your mortgage. PIP provides that immediate relief, while a strong UM/UIM policy ensures you have the resources for a full recovery down the road.

Never, Ever Sign the UM/UIM Rejection Form

If you take only one piece of advice from this, let it be this: Under no circumstances should you ever sign the UM/UIM Rejection Form. Texas law is on your side here—it requires insurance companies to automatically include this coverage in every policy. The only way they can remove it is if you actively sign your rights away.

Some agents might push this form on you, framing it as a simple way to save a few bucks on your premium. But the financial risk you take on is catastrophic. Waiving this coverage leaves you and your family completely exposed to the financial devastation an uninsured driver can cause. And that risk is very real. In some parts of the country, the rate of uninsured drivers is alarmingly high, exceeding 20 percent.

Signing that form is like throwing the lifeboats off a ship just to save a little weight—it's a reckless gamble that can cost you everything. Always double-check your policy declarations page to confirm your UM/UIM coverage is active and that your limits are high enough. If you have any doubt, call your agent and demand written confirmation that you have not rejected this vital protection.

What to Do After a Crash with an Uninsured Driver

The moments after a wreck are a blur of chaos and confusion. Then you find out the other driver has no insurance, and a fresh wave of panic sets in. It’s a terrible situation, but taking the right steps right away is absolutely critical for protecting your health and your ability to recover financially.

Your first priority is always your own safety. The adrenaline pumping through your system after a crash can easily hide serious injuries. Get medical attention immediately, even if you think you’re okay. Call 911 so police and paramedics are on their way.

Secure the Scene and Document Everything

While you wait for help, and only if you’re able to do so safely, start documenting everything. The police report is the official record of the accident, and it's vital the officer notes the other driver’s lack of insurance. Don’t ever let the other driver convince you not to call the police—that’s a huge red flag.

Once the scene is safe, start gathering your own evidence. It can make all the difference.

- Take Photos and Videos: Use your phone. Get pictures of the vehicle damage, any skid marks on the pavement, traffic lights, and the general area from different perspectives.

- Get Witness Information: If anyone saw what happened, get their name and phone number. An independent witness can be incredibly powerful for your claim.

- Keep Meticulous Records: Save every single piece of paper related to the crash. This includes medical bills, pharmacy receipts, and even simple notes about your symptoms and how you’re feeling day-to-day.

Notify Your Insurer and Contact an Attorney

As soon as you can, you have to report the crash to your own insurance company to open a UM/UIM claim. This gets the ball rolling, but it's also where things can get surprisingly difficult. Many people are shocked when their own insurance company, who they’ve paid faithfully for years, starts pushing back.

Your insurer’s main goal is to protect its bottom line. This often means trying to pay out as little as possible—even to their own customers. They might question how badly you were hurt or argue about the value of what you’ve lost.

This is the exact moment you need to call an experienced Houston car accident attorney. An attorney levels the playing field. We’ll take over all communication with the insurance company right away, stopping them from twisting your words or pressuring you into a fast, lowball settlement.

The graphic below shows how the different parts of your policy are designed to work together for your protection.

Think of it as layers of coverage. Your policy is built to provide immediate help through no-fault benefits before moving on to more comprehensive coverage for significant losses.

Building Your Case for Full Compensation

Successfully handling a UM/UIM claim takes a deep knowledge of Texas personal injury law, from proving the other driver’s negligence to meeting the strict two-year statute of limitations for filing a lawsuit. As your legal advocates, our job is to build a rock-solid case that proves fault and documents the full, true extent of your damages.

We handle every detail so you can focus on getting better. Our team investigates the crash, gathers all the evidence, and calculates your total losses, including:

- Current and future medical treatments

- Lost income and diminished future earning capacity

- Physical pain and emotional suffering

- Permanent disfigurement or disability

When an uninsured driver hit your car, you need a team that will fight for every penny you’re owed under your policy. We have a more detailed guide that walks you through the specifics.

You paid your premiums for this protection. Our job is to make absolutely sure your insurance company keeps its promise to you when you need them the most.

Common Questions About Texas UM/UIM Coverage

Figuring out the ins and outs of an auto insurance policy can feel like a chore, especially when you’re trying to make the right call for your family's protection. To cut through the confusion, we’ve put together some straightforward answers to the questions we hear most often about uninsured and underinsured motorist coverage here in Texas.

Does UM/UIM Cover Me as a Pedestrian or Cyclist?

Yes, it absolutely does. This is a critical feature of UM/UIM that many people don't even realize they have.

In Texas, your policy is designed to protect you and your resident family members—not just a particular car. So, if an uninsured or underinsured driver hits you while you're out for a walk, a jog, or a bike ride, you can file a claim under your own auto policy. This coverage can be a true financial lifeline, stepping in to pay for medical bills and lost wages when the at-fault driver has no way to pay.

What Happens if My Medical Bills Exceed My UM/UIM Limits?

This is a nightmare scenario, and it's exactly why choosing a high enough coverage limit from the get-go is so important. If your total damages from the crash are higher than your policy limit, the insurance company's payment stops at that maximum amount, no matter what you're owed.

Sure, you have the legal right to sue the at-fault driver personally for the rest. But the hard truth is that trying to collect a judgment from someone who couldn't afford proper insurance in the first place is almost always a dead end. A skilled Texas personal injury lawyer can hunt down every possible source of recovery, but at the end of the day, your own policy is your strongest financial shield.

Will Filing a UM/UIM Claim Increase My Insurance Rates?

No. In fact, it's illegal for them to do so. Under Texas law, your insurer is prohibited from raising your premiums for filing a UM/UIM claim if you weren't at fault for the accident.

You pay for this protection with every premium payment. It’s a benefit you've earned the right to use without being punished for it.

Be wary if an adjuster ever hints that using your UM/UIM coverage will make your rates go up. That's a classic bad faith tactic. If you hear that, it’s time to call an experienced car accident attorney immediately to make sure your rights are protected.

Should I Just Get the Minimum UM/UIM Coverage?

We strongly advise against it. The state minimums in Texas—just $30,000 per person and $60,000 per accident—are dangerously low for the modern world.

A single trip to the emergency room or one surgery after a bad wreck can burn through those limits in a heartbeat. That could leave you on the hook for tens or even hundreds of thousands of dollars in medical debt.

To truly safeguard your family's financial future, you should buy as much UM/UIM coverage as you can comfortably afford. A good rule of thumb is to match it to your liability limits, but honestly, more is always better. Don't think of it as just another bill—it's a crucial investment in your peace of mind.

The aftermath of a serious accident is difficult, but you don't have to face it alone. At The Law Office of Bryan Fagan, PLLC, our compassionate attorneys are here to answer your questions, handle the insurance companies, and fight for the full compensation you deserve. We invite you to schedule a free, no-obligation consultation to discuss your case and learn how we can help. Your recovery is possible, and expert legal help is just a phone call away.

Schedule your free consultation with our team today by visiting https://texaspersonalinjury.net.